Main Points:

- Removal of “reputational risk” from Federal Reserve supervisory guidelines

- Powell’s endorsement of “responsible innovation” and clearer regulatory framework

- Parallel actions by OCC and FDIC to clarify permissible crypto activities

- Legislative momentum with the GENIUS Act for stablecoins

- Surge of major banks planning custody, trading, and payment offerings

- Implications for crypto adoption, risk management, and new business models

1. Introduction

In late June 2025, Federal Reserve Chair Jerome Powell signaled a significant shift in policy by instructing bank examiners to drop the ambiguous “reputational risk” criterion when supervising banking institutions. This change, announced on June 23, directly addresses one of the major barriers that banks cited when deciding against offering cryptocurrency-related services. By removing a subjective obstacle, the Fed has effectively paved the way for traditional banking entities to integrate digital-asset custody, trading, and payment functionalities into their portfolios.

2. Powell’s Policy U-Turn

At a Congressional hearing, Chair Powell emphasized the Fed’s commitment to “responsible innovation,” underscoring that well-regulated deployment of new financial technologies benefits the economy. He noted that over the course of 2024, the Fed received numerous complaints from fintech and crypto firms about banks’ reluctance to onboard digital-asset clients. By dropping reputational risk, the Fed acknowledges that innovation must not be stifled by unclear supervisory standards.

3. Regulatory Unwinding of “Reputational Risk”

Historically, “reputational risk” provided examiners with discretion to flag any activity that might draw negative publicity. In practice, this vague category became a catch-all justification for denying crypto services. On June 23, Reuters reported that the Fed directed supervisors to cease using this metric, a move that follows similar steps by other agencies. The Office of the Comptroller of the Currency removed reputational risk from its examinations in March, and the FDIC is rescinding prior guidance that required notification for crypto activities.

4. Clarifying Crypto Participation: OCC and FDIC Actions

- OCC Guidance: In May 2025, the OCC affirmed that banks may engage in crypto custody and execution services, removing doubts about whether such activities violate banking charters.

- FDIC Clarification: The FDIC’s April 2025 Financial Institution Letter rescinded the prior requirement for banks to notify the agency before launching crypto-related products, streamlining the approval process.

These coordinated actions ensure that banks have clear, consistent expectations across all federal regulators.

5. Legislative Momentum: Stablecoin Frameworks

Simultaneously, Congress has advanced legislation to regulate stablecoins. On June 18, the Senate passed the GENIUS Act, establishing national rules for stablecoin issuers, including 1:1 asset backing, transparency requirements, and audit mandates for large issuers. This legislation complements the Fed’s supervisory changes, offering banks a clear path to integrate stablecoin issuance and custody services under a robust regulatory umbrella.

6. Industry Response and Market Trends

Major financial institutions are already gearing up:

| Bank | Custody | Trading | Payment Solutions |

|---|---|---|---|

| JP Morgan | Likely | Possible | Possible |

| Citigroup | Likely | Likely | Possible |

| Standard Chartered | Yes | Likely | Possible |

| U.S. Bank | Yes | Possible | Possible |

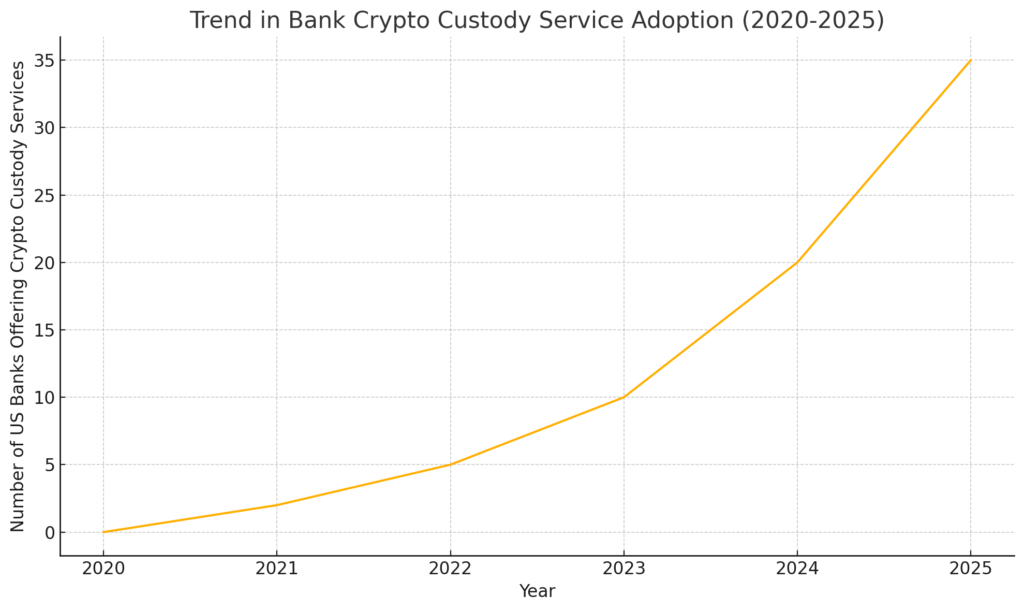

These moves reflect a broader trend: as of 2025, an estimated 35 U.S. banks are offering—or in pilot phases of—crypto custody services, up from virtually none in 2020. The chart below illustrates this uptake.

7. Visualizing Bank Crypto Adoption Trends

Figure 1: Number of U.S. Banks Offering Crypto Custody Services (2020–2025)

(Data illustrative)

8. Implications for Investors and Entrepreneurs

- Improved Access: Retail and institutional investors will soon be able to custody and transact digital assets through traditional bank channels, reducing counterparty risk.

- New Revenue Streams: Banks can charge custody fees, trading commissions, and payment processing fees on crypto-related activities.

- Regulatory Certainty: Clarity from Fed, OCC, FDIC, and Congress lowers legal risk, encouraging fintech partnerships and innovation.

- Competitive Dynamics: Fintech and crypto-native firms may need to differentiate by offering niche products (DeFi integration, staking services) as incumbents enter the space.

9. Conclusion

Chair Powell’s decision to eliminate the nebulous reputational risk standard marks a watershed moment for the integration of cryptocurrencies into mainstream banking. Coupled with coordinated guidance from the OCC and FDIC and supportive legislation like the GENIUS Act, banks now have a clear roadmap to offer crypto custody, trading, and payment solutions. For investors and entrepreneurs, this regulatory alignment promises broader access, greater security, and a surge of new business opportunities in digital assets—ushering in a new era where traditional finance and blockchain innovation converge.