Main Points :

- U.S. teacher unions AFT and AFL-CIO strongly oppose the Senate’s crypto market structure bill, warning it may introduce instability into pension systems.

- The unions argue the proposed legislation treats volatile crypto assets as if they were traditional, stable investment instruments.

- Despite union opposition, political momentum—driven partly by President Trump’s directive to expand crypto options in 401(k) plans—continues to push digital assets toward retirement portfolios.

- Major asset managers and state pension systems have already begun limited crypto exposure through ETFs and specialized funds.

- The risk debate reflects a broader macro trend: crypto’s rapid institutional adoption clashing with regulatory uncertainty in the U.S.

- Investors seeking new digital assets or income streams must interpret this conflict as a sign of the market’s transition toward mainstream financial integration.

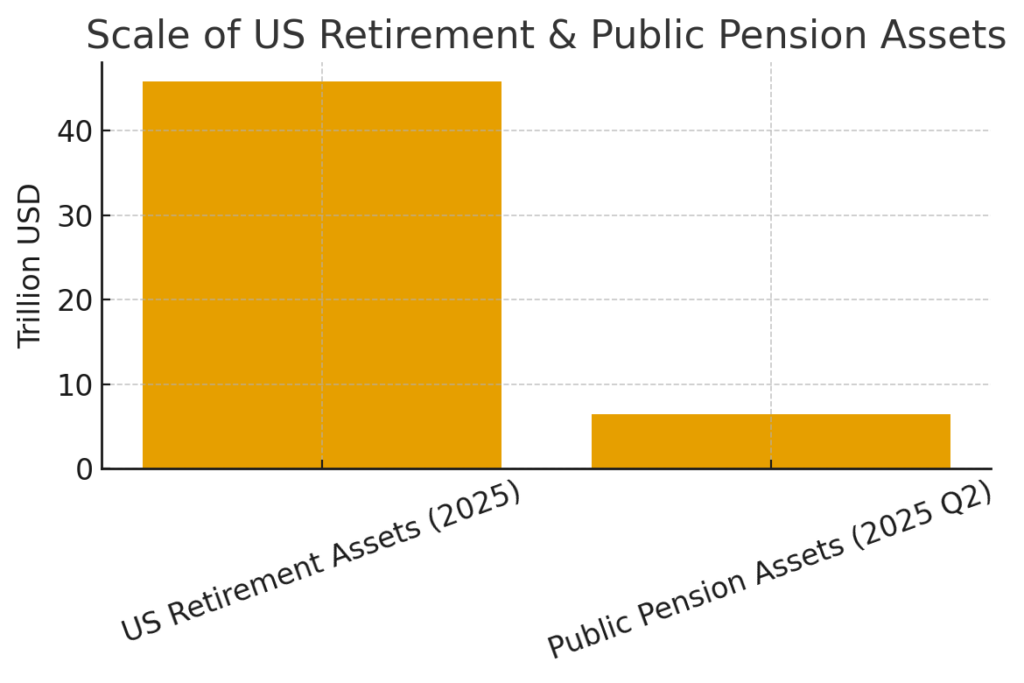

Chart – Scale of U.S. Retirement Assets

(This chart visualizes the relative scale of U.S. retirement assets—USD 45.8 trillion—versus public pension assets—USD 6.5 trillion—which unions fear may be exposed to crypto volatility.)

Section 1 — Introduction: A Nationwide Debate Over Pension Safety

The United States is witnessing a pivotal clash between innovation and financial conservatism. As digital assets gain traction among institutional investors, regulators and worker unions are increasingly concerned about the potential impact of cryptocurrency exposure on the country’s enormous retirement pool, valued at approximately $45.8 trillion. This conflict has come to the forefront as the U.S. Senate considers a new crypto market structure bill—derived from the House-approved CLARITY Act—which aims to modernize the nation’s digital asset regulatory framework.

Yet not everyone sees this modernization as a positive development. The American Federation of Teachers (AFT), representing millions of educators, and the AFL-CIO, the country’s largest labor federation, have both issued formal objections. Their central concern: retirement stability.

The unions argue that crypto assets—volatile, technologically complex, and still lacking broad regulatory clarity—pose an unacceptable risk to pensioners. This tension captures a defining moment for the digital asset industry: as adoption accelerates, so do concerns about systemic risk, investor protection, and economic stability.

Section 2 — What the Senate Crypto Market Structure Bill Seeks to Change

The Senate’s proposed legislation—informally referred to as a complement to the CLARITY framework—aims to establish clearer rules for the classification and oversight of digital assets. It attempts to define jurisdictional boundaries between the SEC and CFTC, create standards for stablecoins, and codify reporting requirements for digital asset intermediaries.

Crucially, the bill does not explicitly authorize the inclusion of cryptocurrencies within pension or retirement plans. However, unions emphasize that the absence of explicit prohibitions leaves the door open for risk amplification. Their fear is that by regulating crypto in a framework similar to traditional assets, lawmakers foster a sense of legitimacy that pension managers may interpret as a green light for broader adoption.

AFT argues that this perception gap is dangerous. While equities, bonds, and other conventional financial instruments have decades of legal precedent and risk-mitigation structures, crypto remains an evolving landscape marked by exchange failures, protocol exploits, regulatory enforcement actions, and liquidity shocks.

Section 3 — Why Unions See Crypto as a Threat to Retirement Security

AFT’s opposition letter—sent to bipartisan leadership of the Senate Banking Committee—warns that the bill “fails to provide the level of regulatory oversight that pension assets require.” Their argument includes several key points:

1. Crypto Assets Are Treated Like Mainstream Investments

AFT states that the bill implicitly frames digital assets as “stable and mainstream,” despite evidence of extreme volatility and market manipulation.

2. Most Pension Funds Avoid Crypto for a Reason

Public pension funds generally hold diversified mixes of equities, fixed income, infrastructure, and real estate. Crypto’s risk profile differs substantially.

3. Retirement Portfolios Should Not Rely on Highly Speculative Assets

AFT and AFL-CIO fear that even small allocations to speculative instruments could endanger long-term solvency for millions of retirees, especially during economic downturns.

4. Regulatory Ambiguity Amplifies Systemic Risk

Without clear, investor-first regulatory structures, digital assets introduce operational, custodial, and market uncertainties not present in traditional portfolios.

Given that teacher pensions and other public retirement systems collectively hold over $6.5 trillion, unions argue that exposing even a small percentage to crypto could create cascading economic effects if markets sharply decline.

Section 4 — The Countermovement: Political and Corporate Push Toward Crypto in Retirement Plans

While unions resist crypto integration, momentum is building in the opposite direction. Political leadership, major financial institutions, and state-level pension programs are actively exploring digital asset frameworks.

1. President Trump’s Executive Order

In August, President Trump signed a directive requiring the Department of Labor (DOL) to reconsider restrictions on alternative assets—including digital assets—in 401(k) plans. His stated goal: to expand diversification options for American workers.

2. Morgan Stanley Opens the Door for Advisors

In October, Morgan Stanley reportedly allowed financial advisors to recommend crypto funds as part of retirement portfolios, reflecting rising institutional comfort.

3. State Pension Funds Begin Limited Exposure

States like Michigan and Wisconsin have begun experimenting with crypto ETF allocations. These moves are small in percentage terms but symbolically significant.

4. Growing IRA and Retirement Crypto Platforms

Several asset managers now offer IRAs tailored to digital assets, targeting younger investors who believe in crypto’s long-term appreciation potential.

Thus, while unions push for caution, the private sector is rapidly embracing crypto as a new frontier in retirement planning.

Section 5 — Market Trends: Institutional Adoption vs. Regulatory Headwinds

Looking beyond the legislative debate, broader market trends highlight crypto’s accelerating institutionalization:

• Rising Demand for Regulated Crypto ETFs

Bitcoin and Ethereum ETFs continue to see strong inflows, particularly among wealth managers.

• Stablecoins as Settlement Infrastructure

U.S. corporates increasingly experiment with USDC and similar stablecoins for cross-border payments, though regulatory oversight remains uncertain.

• Traditional Finance (TradFi) Integrating Blockchain Rails

Firms like BlackRock, JPMorgan, and Fidelity are launching tokenization initiatives for money market funds, U.S. Treasuries, and private credit.

• Growing Pressure for Regulatory Clarity

Investors want consistent rules across exchanges, brokers, stablecoin issuers, and custodians—a goal the Senate bill attempts to address.

Yet contradictions persist: markets seek innovation; unions seek safety; regulators seek balance.

Section 6 — What This Debate Means for Crypto Investors

For readers searching for new crypto assets, next revenue streams, or practical blockchain applications, the union opposition should not be read as a rejection of crypto’s future. Rather, it signals that:

1. Institutional Adoption Will Increase

Despite political disagreements, major asset managers are positioning crypto as a long-term asset class.

2. Regulation Will Become Stricter

The Senate bill—if passed—would create a more structured environment, which often precedes broader institutional investment.

3. Retirement Funds Are a Massive Future Market

The U.S. retirement sector represents nearly $50 trillion, dwarfing the entire crypto market. Even 1% adoption would equal hundreds of billions of dollars in inflows.

4. Short-Term Volatility Remains Inevitable

Investors should expect political debates, regulatory friction, and market cycles to continue shaping sentiment.

Conclusion

The clash between U.S. teacher unions and federal lawmakers underscores a central tension in modern finance: innovation often advances faster than policy. Digital assets are maturing rapidly, but questions remain regarding their role in long-term wealth preservation.

Whether pensions ultimately adopt crypto or avoid it entirely will depend on regulatory clarity, market stability, and the evolution of institutional tools for risk management. For investors, the key takeaway is clear: crypto is steadily moving toward the mainstream, but not without resistance from stakeholders tasked with safeguarding retirements.

The coming years will likely define how digital assets integrate into global financial systems—and whether they enhance or undermine economic security for millions of workers.