Main Points :

- The Federal Reserve (Fed) is exploring a new “payment account” (or “skinny master account”) to give crypto-firms and fintechs direct access to its core payment infrastructure.

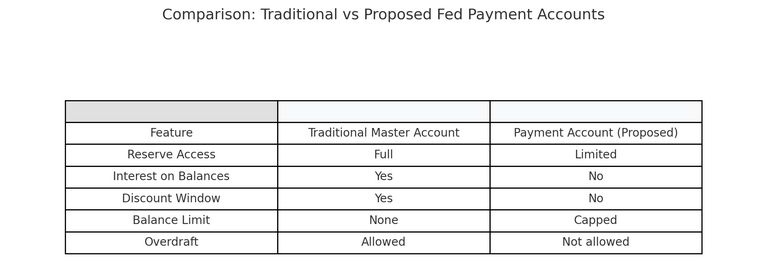

- These accounts would be heavily restricted compared to full master accounts: no interest on balances, no access to the Fed’s discount window, caps on balances, no daylight overdrafts.

- The move signals a shift in the Fed’s posture: from viewing crypto/DeFi as fringe to welcoming them into the payment discussion.

- The proposal is still at prototype stage; many details remain to be defined (eligibility, review timeline, risk-control mechanisms).

- The broader regulatory context: the Fed has already moved to integrate crypto/fintech oversight into its regular supervision framework (scrapping its “novel activities” program).

- For firms in crypto, blockchain infrastructure and payments, this development could materially shift operational models: less reliance on banks, more direct settlement access, potentially lower costs and new business opportunities.

1. Background: why this matters

When we think of how firms access the U.S. central-bank payment infrastructure, typically only federally chartered banks have “master accounts” at the Fed — the kind of account that allows them to send/receive payment-settlements directly via Fed wires and access key liquidity facilities. Traditional banks hold these; emerging crypto firms and fintechs have historically been shut out or forced to funnel through partner banks. This has created structural friction in how crypto/payment innovation integrates with the legacy financial system.

At the recent Payments Innovation Conference, Fed Governor Christopher J. Waller laid out how payments are being transformed: “Stablecoins and tokenised assets making use of distributed-ledger technology… the convergence between these innovations and the traditional financial ecosystem.”

He emphasized that the payments landscape and types of providers have “evolved dramatically in recent years” and that the Fed must “keep up”.

Hence, the proposal of the “payment account” is the Fed’s response to this evolution: offering a tailored, lighter-version of a master account to firms focused on payment innovation.

2. What the “payment account” / “skinny master account” actually means

The proposal is that eligible institutions—which may include fintech companies, stable-coin issuers, crypto asset firms—could gain direct access to the Fed’s payment rails via this new account type. Key features as outlined:

- Access to the Fed’s payment infrastructure: The account would allow firms to send/receive payments (via Fed settlement systems) without going through a partner bank.

- Restrictions compared to full master account:

- No interest on balances held in the account.

- No daylight overdraft privileges; if the balance hits zero, payments would simply be rejected.

- No access to the Fed’s discount-window or emergency lending facilities.

- Balance caps would likely be imposed to control risk exposure.

- Streamlined review process: Because these accounts are risk-limited, the Fed staff would target a simpler/shorter request timeline compared to full bank master accounts.

- Prototype stage: It is still only a concept under study; many implementation details remain unspecified (exact eligibility criteria, supervision model, risk-management framework).

3. Implications for the crypto/blockchain ecosystem

For readers who are exploring new crypto assets, payments use-cases, blockchain infrastructure or are seeking new sources of revenue, this development is significant in several ways:

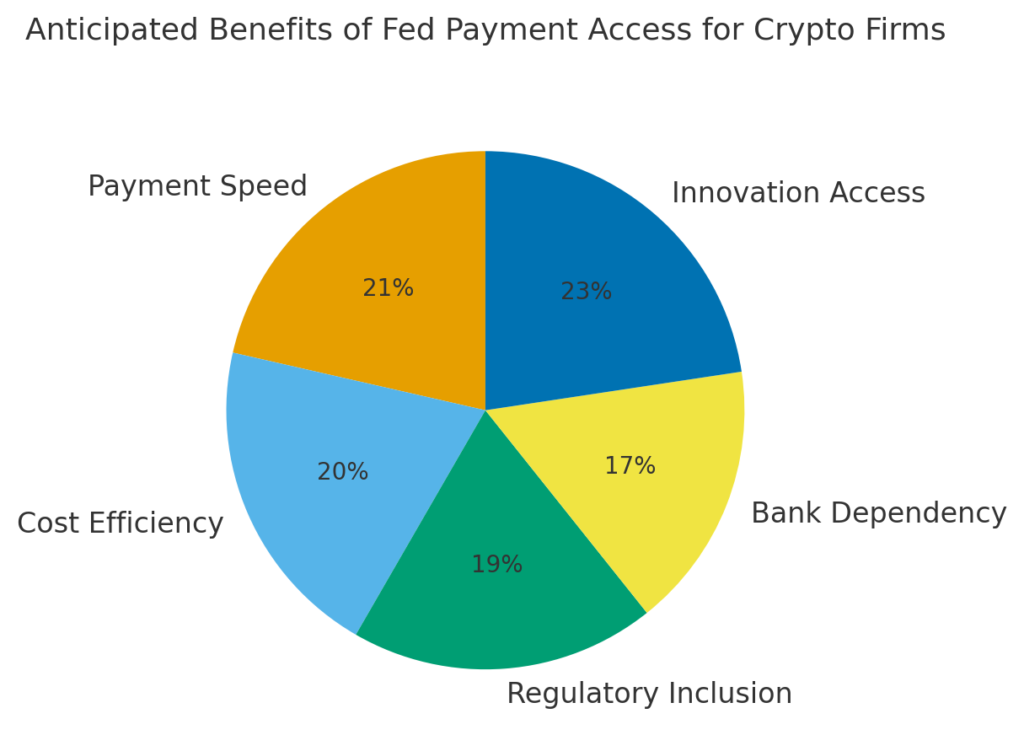

- Reduced dependence on banks: Until now, many crypto firms needed a partner bank with a Fed master account to gain access to settlement infrastructure. The new account could remove or reduce that intermediary layer, lowering cost and operational friction.

- Faster settlement, lower cost opportunities: Direct access to Fed rails means faster payment flows, potentially enabling products such as token-settled transfers, stable-coin based cross-border payments, or blockchain-native rails to interface with real-world settlement layers.

- Greater legitimacy of crypto payment firms: Fed acknowledgement signals that crypto / DeFi is no longer niche. That can bolster confidence, unlock partnerships, and invite institutional capital.

- Emergence of new business models: Firms may design services around being “Fed-connected” fintechs: e.g., payment processors leveraging blockchain rails, stable-coin issuers offering Fed-settled on-ramp/off-ramp, tokenised asset platforms integrated with core infrastructure.

- Risk and regulatory guard-rails remain important: Because these accounts have built-in limitations, firms must still operate within frameworks that control for systemic risks (e.g., large unbacked stable-coin flows, settlement risk, operational risk). The Fed emphasises that it still requires “safety and stability” even as it supports innovation.

- Market-timing and competitive advantage: For firms already positioned in payments-blockchain niches, this could provide an early mover advantage. Conversely, firms slow to adapt may face increased competition from those with direct rails access.

4. Regulatory context and recent trends

This proposal doesn’t happen in a vacuum; it fits into broader shifts in U.S. crypto/fintech regulation:

- Earlier in August 2025 the Fed announced it would scrap its “novel activities” supervisory program (which specifically monitored banks’ crypto/fintech activities) and instead incorporate such oversight into its standard framework.

- That move has been interpreted as the Fed believing that crypto/fintech risks are now better understood and that they should be supervised in the same way as other bank-activities. This may therefore lower the regulatory “fear-factor” for crypto firms.

- In earlier speeches, Waller stated that DeFi is “no longer on the fringes” and that the Fed intends to be an active part of the payments revolution.

- At the same time, the Fed still emphasises that firms must have “appropriate backing assets” and sound governance in stable-coins and other digital-asset services to avoid financial-stability risk.

- The proposed payment-account model seems to embody a hybrid approach: open infrastructure more broadly, but with built-in restrictions to maintain safety-net features.

5. What this means for blockchain practitioners and crypto-asset seekers

From your vantage (interested in new crypto assets, revenue streams, blockchain practical uses), here are some actionable take-aways:

- Watch firms that may gain payment-account access: If a crypto or tokenised-asset platform secures such access, it may gain a competitive edge. Partnerships, enterprise clients and settlement rails may evolve accordingly.

- Consider infrastructure plays: Blockchain platforms, layer-2 networks or protocols that integrate with Fed-settled rails could find demand. If you build or invest in middleware, tokenised-asset settlement, stable-coin rails or cross-border payments tied to Fed access, the addressable market may expand.

- Re-evaluate stable-coin business models: A stable-coin issuer that can tap Fed rails directly might lower costs and enhance credibility. This could impact valuations of stable-coins and token projects built around them.

- Risk-management is paramount: While the opportunity is strong, firms still need to meet eligibility, compliance, oversight and operational-risk standards. Blockchain innovator-firms should pre-emptively align with governance / transparency frameworks.

- Timing matters: Since the proposal is still under study, now is a good time to build use-cases and show readiness (e.g., regulated entity status, auditability, real-world payment flows). Early preparedness positions you to leverage the rails when available.

- Tokens and assets tied to payment rails may trend: If settlement rails become cheaper and more direct, tokenised payment networks, on-chain remittance services or hybrid rails (blockchain + Fed) may become more attractive. This may shift investor sentiment in related crypto-assets.

6. Challenges and unanswered questions

While the direction is promising, some caveats remain:

- Eligibility still unclear: “Legally eligible institutions” is vague. Some crypto-firms may still not qualify depending on charter, regulation, custody model.

- Risk oversight remains stringent: The Fed emphasises the need for safety and stability — so firms may face heavy compliance burdens.

- Scale limitations: Balance caps and no discount-window access mean the account may be good for payment-settlement flows but not for large-scale banking operations or speculative leveraging.

- Implementation timeline unknown: While the speech was made, actual rollout and rule-making may take time; advantages may accrue to those ready ahead.

- Ecosystem coordination required: Beyond the account itself, the broader payments/crypto ecosystem (banks, token-issuers, infrastructure providers, regulators) will need to bridge legacy systems with on-chain flows.

7. Summary and outlook

In summary: The Fed’s proposal to open a new type of “payment account” aimed at crypto/fintech firms is a major inflection point. It signals that blockchain-native firms may soon gain direct access to core central-bank payment rails — a capability that was historically reserved for banks. For those in crypto assets, payments rails, tokenisation and blockchain infrastructure, this offers a window of strategic opportunity: design business models that leverage this access, partner early with regulated entities, align governance/compliance, and think about how on-chain flows can integrate with real-world settlement.

Looking ahead: If implemented, the model could accelerate the convergence of blockchain-first systems with legacy financial infrastructure. Stable-coins and tokenised assets may become more deeply embedded in the U.S. settlement ecosystem. Firms that are prepared now—operationally, legally and technically—may enjoy first-mover advantages. The key will be balancing innovation and risk-management: the Fed has made clear it will support transformation, but not at the cost of financial stability.

For anyone seeking new crypto-asset opportunities or revenue models in blockchain, this is a moment to pay attention, strategise and act. The rails are evolving — and those ready to ride them stand to gain.