Main Points :

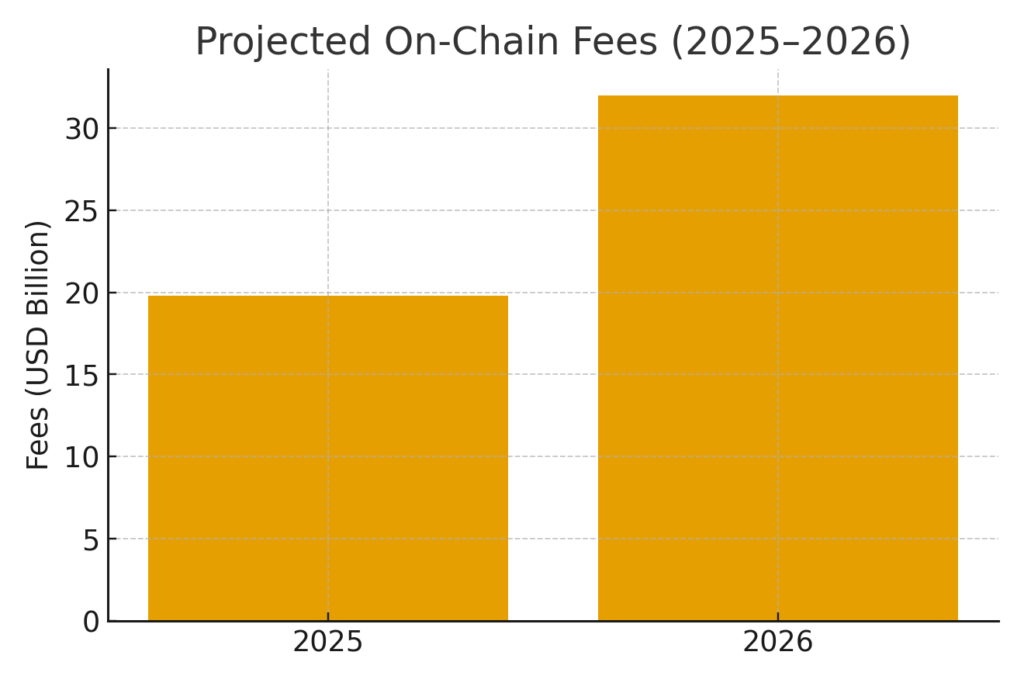

- On-chain fees paid by users are projected to reach approximately $19.8 billion (≒ ¥3 trillion) in 2025.

- In the first half of 2025 alone, users paid about $9.7 billion in on-chain fees.

- These fees serve as one of the clearest indicators of real-world usage and utility of blockchain networks, beyond purely speculative activity.

- Emerging sectors such as Real World Asset (RWA) tokenization, decentralised physical infrastructure networks (DePIN), wallet-monetised consumer apps are expanding rapidly.

- The growth of fees highlights a shift: crypto networks are evolving from speculative instruments to revenue-generating, utility-driven infrastructure.

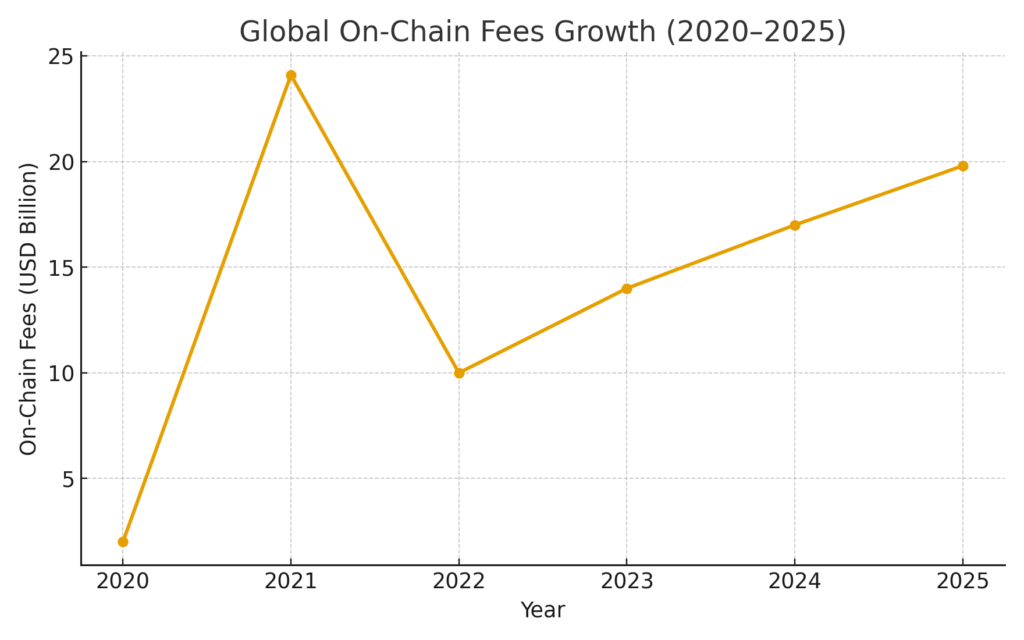

- While the total remains below the previous peak (≈ $24.1 billion in 2021), the compound annual growth rate (CAGR) since 2020 is around 60 %.

- Projections for 2026 suggest on-chain fees could reach about $32 billion, driven by the application layer of the ecosystem.

1. On-Chain Fees as a Barometer of Blockchain Maturity

In the early days of cryptocurrency, the narrative was dominated by price speculation, token trading and macro-stories such as the halving of Bitcoin or major exchange listings. However, the new research by VC firm 1kx (their “On-Chain Revenue Report H1 2025”) shifts attention toward one of the most telling metrics of real-world utility: on-chain fees paid by users and companies for direct blockchain-based activity.

These fees include user payments for transactions, swaps, registrations, gaming incomes, subscriptions and other behaviours directly on blockchain infrastructure. The logic is simple but profound: when people pay for using a protocol, it suggests sustainable value and recurring utility, beyond mere speculation. As the report states: “We view fees paid as the best indicator, reflecting repeatable utility that users and firms are willing to pay for.”

For crypto investors, developers (like you, developing a wallet or swap UX) and protocol designers, this shift matters: it signals that blockchain networks are being valued increasingly as revenue-generating infrastructure rather than purely as volatile assets.

2. The Snapshot: 2025’s On-Chain Fee Landscape

The 1kx report aggregates data across more than 1,200 protocols spanning multiple sectors (blockchains, DeFi/finance, wallets, consumer apps, DePINs, middleware).

Key figures include:

- Users paid approximately $9.7 billion in on-chain fees during the first half of 2025.

- For the full year 2025, the projection ranges between $19.8 billion to $20 billion.

- While this doesn’t surpass the ~$24.1 billion achieved in 2021, it still represents a greater than ten-fold increase since 2020 and a CAGR of ~60 %.

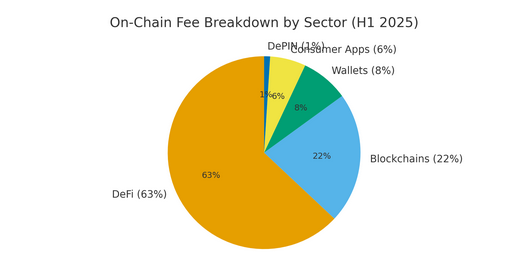

- Breakdown by sector (H1 2025): DeFi protocols accounted for approximately 63 % of total fees (~$6.1 billion). Blockchains ~22 %, wallets ~8 %, consumer applications ~6 %, while DePIN and middleware made up ~1 % each.

- Fee growth in emerging segments: Wallet-monetised apps reportedly grew by ~260 % year-on-year; consumer apps ~200 %; DePIN ~400 %.

For your interest as someone building a wallet, this is particularly relevant: wallet ecosystems are now not just tools for holding assets, but increasingly centres for monetised user interaction.

3. What Is Driving the Growth?

3.1 Scalable Infrastructure and Falling Fees

One driver is the declining cost of transactions: average blockchain transaction fees have fallen significantly (e.g., up to ~86 % drop since 2021 for major chains) as layer-2 solutions, scaling efforts and more efficient networks proliferate.

Lower fees broaden access, increase usage, and facilitate new verticals (gaming, subscription, DePIN). More usage means more fees in aggregate even if per-transaction fee is lower.

3.2 Emerging Application Layers

Beyond simple transfers, protocols are increasingly applied to:

- Tokenization of real-world assets (RWA) – buildings, loans, real estate, private equity being represented on-chain. According to RWA.xyz and 1kx, the on-chain value of tokenized RWAs (excluding stablecoins) in Q3 2025 exceeded $28 billion, and has since passed ~$35 billion.

- DePIN (decentralised physical infrastructure networks) – e.g., networks that use tokens to incentivise physical hardware deployment and usage.

- Wallet-centric consumer cryptographic apps – bundling payments, subscriptions, social interactions, etc.

These application layers are showing high growth in fees, signalling greater adoption of blockchain infrastructure for “real” use cases rather than speculative trades.

3.3 Institutional Participation and Tokenisation

Major financial institutions are increasingly engaging in tokenisation initiatives: for example, JPMorgan tokenised a private-equity fund on its private Kinexys blockchain; BNY Mellon partnered with RWA tokenisation platforms like Securitize to bring asset-backed loans on-chain.

These initiatives hint at the evolving role of blockchain within capital markets and the broader financial ecosystem. For blockchain practitioners and investors, this means infrastructure built today may connect to trillion-dollar traditional markets.

4. Implications for New Crypto Assets, Income Streams and Practical Blockchain Use

For your audience—those seeking new crypto assets, income opportunities and practical blockchain applications—here are key takeaways:

4.1 Protocols with recurring fee revenue may gain valuation recognition

Protocols that generate stable, recurring on-chain revenues (e.g., via user fees) may start to be valued more like businesses rather than purely speculative assets. The 1kx report notes a divergence: blockchains may trade at 3,900× price-to-fees, whereas DeFi apps trade closer to ~17×, suggesting application-layer protocols may present opportunity.

4.2 Emerging sectors = higher growth potential but also higher risk

Segments such as RWA tokenisation, DePIN and consumer apps are experiencing rapid growth in fee revenue (200-400% YoY). These could be fertile ground for early-stage opportunities—both token issuances with applied use-cases and decentralised services monetising wallets as UX front-ends.

4.3 Infrastructure builders and wallet platforms are strategic

Given your interest in developing a wallet with BTC↔ETH swaps and strong UX, note that wallet-based monetisation is one of the fastest growing segments (~260% YoY growth). If you embed fee-based services (subscriptions, swaps, infrastructure access) that users pay for, you align with this trend.

4.4 Tokenisation opens up new asset-classes and revenue models

Tokenised RWAs are growing rapidly—on-chain value doubling over one year—offering new yield opportunities, token economics, and use-cases beyond “store-of-value”. For example, tokenised debt, real estate, and private equity on-chain may represent future income streams.

4.5 Maturation implies more scrutiny and disclosure

With increasing institutional participation and focus on revenue metrics, protocols may be expected to disclose on-chain fee data, usage statistics and recurring revenue models to attract investment. In your token issuance plans (e.g., for wallet or platform utilities) aligning your metrics with this mindset may help investor confidence.

5. Structural Shift: From Speculation to Utility-Driven Networks

The overarching theme is that the crypto ecosystem appears to be entering a more “mature” phase—where the interplay of usage → fees → value distribution becomes dominant. The report suggests that networks that can generate and distribute stable fee-based revenue will separate long-term, durable networks from early-stage experimental projects.

For example, while the speculative bull-runs of 2020-21 generated large fee totals, much of the fee revenue then was driven by high gas costs and speculative trading. Now, lower per-transaction fees but higher volume and diversified application types reflect deeper adoption.

The report forecasts that by 2026, on-chain fees could approach $32 billion (≈ ¥5.8 trillion) in a single year. This suggests we are at an inflection point: the crypto economy is becoming a meaningful complement to Web 2 infrastructure, not just a niche playground.

6. Considerations and Risks

While the trend is positive, several caveats should guide strategic thinking:

- Even though the fee totals are rising, they still remain below the 2021 all-time high. There is no guarantee of a straight path upward.

- The majority of fees still stem from established segments (DeFi) and top protocols: the top 20 protocols capture ~70% of fees. This concentration means discovering “the next protocol” remains challenging.

- Fee data is just one metric: other dimensions such as token economics, governance, sustainable user growth, regulatory risk, security matter deeply.

- Regulatory or macro-economic headwinds (e.g., policy changes, crypto bans, macro downturns) could slow adoption and fee growth.

- The transition from speculation to utility may compress returns for purely speculative tokens; investors and builders may need to adapt to revenue-based valuation models.

Conclusion

The crypto industry in 2025 is showing clear signs of transition from an era focused on token price speculation toward one grounded in real utility, usage and monetised infrastructure. With projected on-chain fees approaching $20 billion this year—driven by DeFi, wallet apps, tokenised real-world assets and DePIN—stakeholders should take note. For those seeking new crypto assets or income streams, focusing on protocols and applications that generate repeatable, user-paid revenue may be wise. For builders such as wallet developers or token issuers, aligning product strategy with monetised fee models, tokenised assets and consumer-facing flows places you at the heart of the emerging phase. The maturation of crypto is not just about price surges—it’s about building revenue-generating networks. As we look ahead to 2026 and the potential $32 billion fee milestone, the narrative is shifting: crypto as infrastructure, crypto as services, crypto as business.