Key Takeaways:

- OCC Interpretive Letter 1188 has formally confirmed that U.S. national banks can execute “riskless principal” crypto trades, acting as intermediaries between customers without holding volatile crypto inventory on their own balance sheets.

- This puts crypto on the same structural footing as traditional securities brokerage, giving large banks a clear legal path to offer execution and intermediation in Bitcoin, Ethereum, and other non-securities tokens.

- Bank of America, among others, is now allowing wealth advisers to recommend crypto ETPs and suggesting 1–4% portfolio allocation to digital assets for clients who can handle volatility.

- PNC Bank has launched direct spot Bitcoin trading for eligible private-bank clients via a deep integration with Coinbase’s Crypto-as-a-Service infrastructure, making it the first major U.S. bank to do so.

- Anchorage Digital Bank, the first and still only federally chartered crypto bank, has had its OCC consent order lifted and is positioning itself as a regulated engine for white-label stablecoins and institutional crypto infrastructure, especially under the new GENIUS Act stablecoin regime.

- The stablecoin market has surpassed roughly $300 billion in capitalization, with issuers holding over $150 billion in U.S. Treasury bills, turning bank-friendly stablecoins and RWA tokens into core infrastructure for yield strategies.

- In Europe, a consortium of 10 major banks is building qivalis, a euro-backed stablecoin platform, confirming that bank-issued stablecoins are becoming a global theme rather than a U.S.-only phenomenon.

These shifts open new opportunities not just for Bitcoin and Ethereum, but for bank-compatible tokens, on-chain Treasury strategies, and infrastructure projects that connect DeFi rails with regulated bank balance sheets.

1. What Did the OCC Actually Approve?

The original Japanese article explains that the U.S. Office of the Comptroller of the Currency (OCC) has published Interpretive Letter 1188, making it explicit that national banks can engage in “riskless principal” transactions in crypto-assets.

In plain language, this means:

- A bank can buy a crypto-asset from one customer and, at essentially the same moment, sell it to another customer.

- The bank does not keep the asset as inventory, except for a minimal instant needed to match the trade.

- As a result, the bank is exposed only to very short-term settlement risk, not to ongoing market price swings.

This is not a brand-new invention. In the securities world, riskless principal trading has been recognized for years as a standard brokerage function. The OCC is now saying: if banks are allowed to do this for stocks and bonds, they can do the same structure for crypto, as long as the underlying assets are non-securities tokens and the bank meets all safety and soundness requirements.

For years, the OCC, Fed, and other regulators warned banks about the liquidity, volatility, and operational risks of crypto between roughly 2021 and 2024. The new letter does not ignore these risks. Instead, it channels crypto activity into a form that supervisors know how to oversee: brokerage-like intermediation, not speculative trading on the bank’s own book.

2. How “Riskless Principal” Crypto Trading Works

At a technical level, a riskless principal crypto transaction looks like this:

- Customer A wants to sell, say, $100,000 of BTC.

- Customer B wants to buy $100,000 of BTC.

- The bank steps in as an intermediary:

- Buys BTC from A for $100,000 (very briefly as principal).

- Immediately sells the same BTC to B for $100,000 (or $100,000 plus a fee).

- The bank earns a spread or explicit fee, but does not hold BTC or USDC for price speculation.

Economically, this is almost identical to the bank acting as an agency broker, except that technically it is a principal in both legs. The OCC’s key point is that:

- This activity is functionally similar to existing bank brokerage business.

- Therefore, it can be treated as part of the bank’s “incidental powers”—the set of activities a national bank may conduct in connection with traditional banking business.

For crypto builders and traders, the important consequence is that execution can move from loosely regulated offshore exchanges into fully supervised U.S. banks, without requiring banks to become speculative trading houses.

3. Why This Matters for Investors Looking for the “Next Trade”

For your audience—people hunting for new assets, next revenue streams, and practical blockchain use cases—this change is less about legal wording and more about who you trade with and what products become possible.

Some immediate implications:

- Onboarding capital: Large private banks and wealth platforms already manage trillions of dollars in client assets. Once crypto execution is clearly permitted, even modest 1–4% allocations recommended by big banks can mean tens or hundreds of billions of new demand flowing into Bitcoin, Ether, and possibly bank-vetted altcoins and ETPs.

- Counterparty risk shifts: Wealthy clients who avoided offshore exchanges (“I don’t want my money on some Cayman exchange I’ve never heard of”) now have a path to trade through their existing bank relationship, where KYC, AML, and capital rules already exist.

- Product innovation: Once trade execution is in-house, banks can more easily package structured products, lending lines, and yield strategies around underlying crypto exposure while still staying within familiar regulatory frameworks.

From a trader’s perspective, the OCC’s letter is a liquidity and trust upgrade layer for the crypto market.

4. Big Banks Are Already Moving: BofA, PNC, and Others

This OCC signal doesn’t land in a vacuum. It drops into a landscape where several large institutions were already edging into crypto.

Bank of America: From “No” to Portfolio Recommendation

Bank of America now allows its wealth advisers across Bank of America Private Bank, Merrill, and Merrill Edge to recommend crypto ETPs (exchange-traded products) directly to clients, starting in early 2026. The bank’s research arm has publicly discussed 1–4% crypto exposure for suitable portfolios, framing it as a high-volatility satellite allocation around a core traditional portfolio.

This is a big mindset shift: from “we can’t touch crypto” to “we can recommend regulated vehicles that track Bitcoin and other assets.”

PNC: Direct Spot Bitcoin Trading via Coinbase

In parallel, PNC Bank is rolling out direct spot Bitcoin trading for eligible private-bank clients, powered by Coinbase’s Crypto-as-a-Service infrastructure. Clients trade inside PNC’s own digital banking interface; Coinbase handles the underlying execution and custody plumbing. PNC is being described as the first major U.S. bank to offer direct spot BTC trading to its clients in this way.

This is exactly the type of business model that becomes more robust when the OCC says: “Yes, this kind of intermediation is part of the business of banking.”

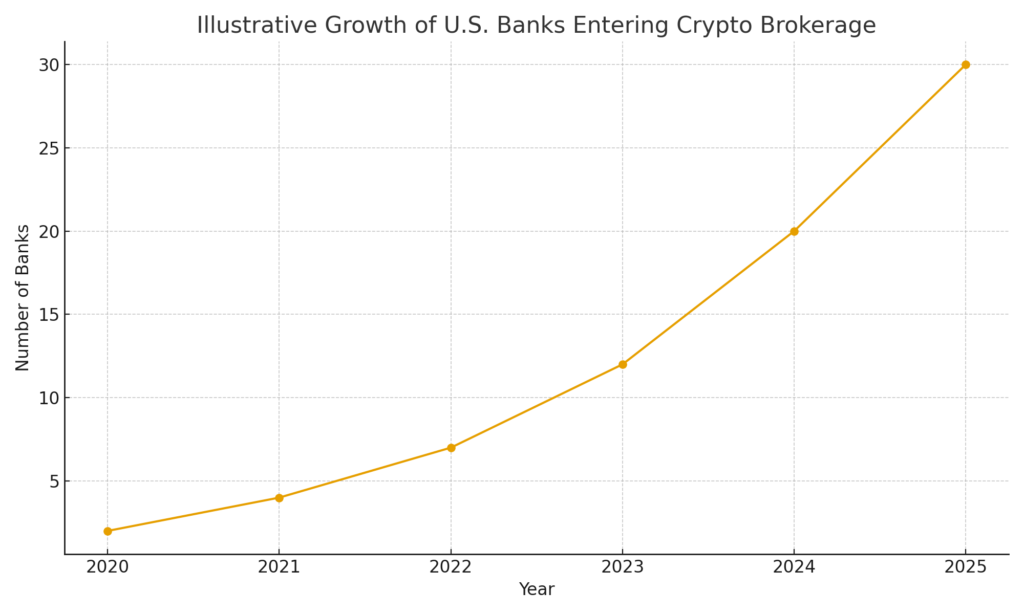

Use this chart in the section above to visually show a hypothetical upward trend in the number of U.S. banks entering crypto brokerage between 2020 and 2025.

(Note: The chart is illustrative, not actual regulatory data.)

5. The Rise of Regulated Crypto Banks and Stablecoins

Beyond traditional banks, crypto-native institutions are also adapting to the new environment.

Anchorage Digital Bank: From Consent Order to Stablecoin Engine

Anchorage Digital Bank—the first federally chartered digital asset bank in the U.S.—was previously under an OCC consent order over AML program weaknesses. That order was lifted in August 2025, signaling that the bank has upgraded its compliance to satisfy federal regulators.

Anchorage is now positioning itself as:

- A regulated custody and trading hub for institutions

- A platform capable of launching white-label, federally regulated stablecoins, especially in the wake of the GENIUS Act, which sets out a clear framework for U.S. payment stablecoins.

For builders, that means:

- If you are designing RWA tokens, tokenized T-bills, or bank-compatible stablecoin utilities, there will be federally supervised infrastructure that can host or integrate with your project.

The $300+ Billion Stablecoin Base Layer

The stablecoin market has quietly become a $300+ billion sector, with dollar-pegged coins dominating. Recent data point to total stablecoin market capitalization above $300 billion, and analysts estimate that stablecoin issuers hold about $155 billion in U.S. Treasury bills, roughly 2.5% of the entire T-bill market.

For your audience, the takeaway is:

- Stablecoins are no longer “just” trading chips; they are on-chain wrappers around real, dollar-denominated cash and short-term government debt.

- Regulatory clarity (GENIUS Act in the U.S., MiCA in the EU) makes bank-grade stablecoins much more likely, creating new yield strategies and liquidity pools that are acceptable to institutional capital.

6. Global Banking: Euro Stablecoins and Cross-Border Opportunities

The OCC’s move is part of a global race among banks to control the interface between fiat and digital assets.

In Europe, a group of 10 major banks—including ING, UniCredit, and BNP Paribas—has formed qivalis, a company dedicated to issuing a euro-backed stablecoin. The consortium is applying for an EMI license from the Dutch central bank and aims to launch the stablecoin in 2026.

Key implications:

- Banks are not content to let US dollar stablecoins dominate global crypto flows.

- For developers and liquidity providers, cross-chain and cross-currency routing between USD stablecoins and future EUR bank-stablecoins will likely become a major theme.

- DeFi protocols that can plug into** bank-issued stablecoins**—with clear KYC and sanctions controls—will have an easier time partnering with regulated institutions.

This is an opportunity for builders to create compliance-aware, cross-currency liquidity layers that speak the language of both DeFi and core banking.

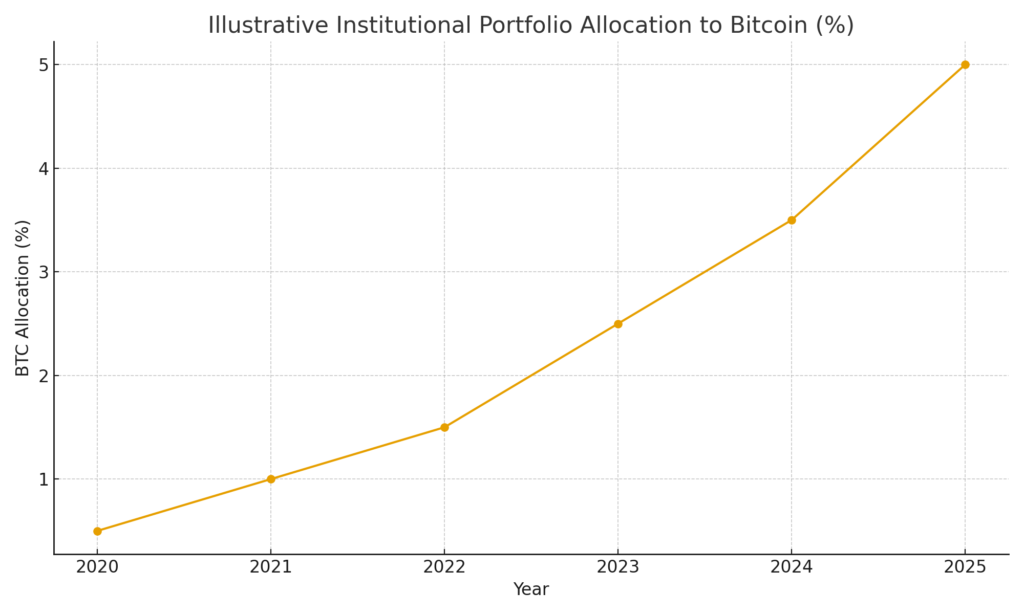

Place this chart in this or the next section to show a hypothetical increase in institutional portfolio allocation to Bitcoin from 2020 to 2025, rising from below 1% to around 5%.

(Again, this is illustrative, not a precise market statistic.)

7. Where Are the Opportunities? Tokens, Yield, and Infrastructure

Given this regulatory context, where are the practical opportunities for investors and builders?

7.1 Bank-Compatible Tokens and Infrastructure

Projects that are easy to integrate into bank workflows will have an advantage:

- Stablecoins backed by cash and T-bills with transparent reporting and strong compliance.

- RWA tokens representing U.S. Treasuries, money market funds, or short-duration credit, structured so banks can either hold the assets themselves or rely on a regulated partner.

- KYC-enabled DeFi protocols that let banks offer yield opportunities within a permissioned environment.

Anchorage’s stablecoin and custody stack, Coinbase’s Crypto-as-a-Service, and other institutional platforms act as bridges between traditional banks and the public chains where these tokens live.

7.2 Yield From the New “On-Chain Money Market”

With stablecoin issuers holding over $150 billion in Treasuries and the total stablecoin market above $300 billion, on-chain finance is effectively building a parallel money-market layer, denominated in U.S. dollars.

Opportunities include:

- Providing liquidity to bank-affiliated stablecoin pools, where yields come from transaction fees, lending spreads, or reward programs.

- Building treasury-management tools for corporates and family offices that want on-chain exposure to dollar yields without giving up regulatory comfort.

- Designing hedging and derivatives products (e.g., interest-rate swaps on stablecoin yield, BTC options, etc.) that banks can route to regulated counterparties.

7.3 Trading and Market-Making Around Bank Flows

As more banks turn on crypto brokerage for wealthy clients, we should expect:

- Time-clustered order flow around bank business hours.

- Flow “herding” into the assets banks are most comfortable with: Bitcoin, Ether, large-cap tokens, regulated ETPs, and bank-endorsed stablecoins.

- Demand for smart routing, liquidity aggregation, and cross-venue arbitrage between bank channels, centralized exchanges, and DeFi venues.

This creates opportunities for both professional market-makers and infrastructure providers offering order-routing, analytics, and execution algorithms tuned to bank-driven flows.

8. Risks and Constraints: It’s Not “Number Go Up” Only

The OCC’s stance is positive, but it doesn’t remove risk. If anything, it formalizes how risk is managed and where it sits.

Key constraints:

- Compliance overhead: Banks will require full KYC, sanctions screening, and transaction monitoring for all crypto clients. The days of easy anonymous trading are not coming back in the regulated channel.

- Limited token universe: Because the OCC’s letter covers non-securities crypto-assets, banks will be cautious about which tokens they touch, given ongoing debates over which assets are securities under U.S. law.

- Concentration in a few rails: A large portion of flows may end up in a handful of dominant networks (e.g., Bitcoin, Ethereum, and bank-endorsed stablecoins), leaving smaller ecosystems to compete for attention and liquidity.

From a portfolio perspective, the volatility of Bitcoin and other majors remains real—recent data show that even in 2025, Bitcoin can lose over $10,000–$20,000 in a single month in dollar terms.

For serious investors, the message is: the rails are becoming more regulated and more institutional, but asset risk hasn’t magically disappeared.

9. Conclusion: Banks as the New Crypto Gatekeepers

The OCC’s Interpretive Letter 1188 completes a quiet but powerful transition:

- Crypto trading is no longer only a domain of offshore exchanges and specialized brokers.

- U.S. national banks now have a clear regulatory path to intermediate crypto trades as riskless principals.

- Large institutions like Bank of America and PNC are already moving, while Anchorage and other crypto-native banks provide specialized infrastructure, particularly around stablecoins.

For your readers, the core opportunity is to position themselves where the regulated capital will flow next:

- Bank-friendly tokens (especially dollar-backed stablecoins and RWA tokens).

- Infrastructure that helps banks, wealth managers, and corporates use blockchain for real business—payments, custody, collateral, and on-chain money markets.

- Trading and yield strategies that align with tighter compliance but still capture the growth of digital assets as a new asset class.

In short, the OCC has turned riskless principal crypto trades into a legitimate, regulated banking business. As banks update their technology stack—from telegraph to SWIFT to blockchain—the next wave of adoption will likely be less about speculative hype and more about integrating crypto into the daily workflows of global finance. For builders and investors who understand both sides—code and compliance—this is a rare window where regulation is actively expanding, not shrinking, the frontier of opportunity.