Main Points :

- Norway’s central bank concludes that a retail or wholesale CBDC is not currently justified, citing a highly efficient existing payment system.

- Despite pausing implementation, Norway maintains readiness for future CBDC deployment if circumstances change.

- Norway’s years-long CBDC experiments—including cross-border trials—highlight the complexity and slow global progress toward CBDC standardization.

- The European Central Bank’s digital euro project is moving ahead and is expected to begin issuance around 2029, depending on legislation.

- The global landscape shows uneven CBDC readiness, leaving opportunities for private digital assets, stablecoins, and blockchain-based payment infrastructure.

Introduction: A Rare Moment of Restraint in the CBDC Race

While dozens of central banks across the world are accelerating their central bank digital currency (CBDC) projects, Norway has taken an unusually cautious stance. The Norges Bank (Norway’s central bank) announced that, despite several years of research and pilot testing, CBDC implementation is not currently justified.

This decision matters beyond Norway. It represents a sober reminder that CBDCs—often portrayed as inevitable—must still prove their necessity, especially in markets where electronic payments are already mature, efficient, and low-cost.

Norway’s move contrasts with active CBDC development in the Eurozone, China, and other regions. For crypto investors and blockchain builders, this raises critical questions:

If advanced economies slow down CBDC adoption, does this strengthen the value proposition of decentralized digital assets? Does it open more room for stablecoins and tokenized settlement networks?

In this article, we examine Norway’s decision, compare it with global trends, analyze the implications for blockchain adoption, and explore emerging crypto opportunities in a world where CBDCs are progressing unevenly.

Norway’s Position: “No Justification for CBDCs at Present”

A Highly Efficient Payment System Reduces Urgency

Norges Bank Governor Ida Wolden Bache stated clearly:

“Norway’s existing payment system is already safe, efficient, and offers low-cost transactions. Introducing a CBDC is not justified at this time.”

Norway is already one of the most cashless societies in the world. Over 95% of retail payments are digital, and private bank-issued electronic money works with high reliability. From the central bank’s perspective, the marginal benefit of adding a CBDC—at least now—is limited.

However, Norway emphasized that this is not a cancellation, merely a pause. Should the need arise—such as operational risks in private payment infrastructures or geopolitical pressures—the bank is ready to move forward.

Years of Testing: Norway’s Extensive CBDC Experimentation

Norway did not reach its conclusion lightly. The country conducted several pilot programs and participated in global CBDC collaborations.

1. Token-Based CBDC Experiments

Over the past few years, Norway tested blockchain-based settlement models, exploring:

- tokenized retail CBDCs

- wholesale CBDCs

- programmable settlement features

- cross-platform interoperability

These tests revealed promising potential—but also highlighted unresolved challenges, especially around security, scalability, and standardization.

2. Participation in Project Icebreaker (2023)

Norway joined Israel and Sweden in Project Icebreaker, which examined new architectures for cross-border retail CBDC payments. The project demonstrated that CBDCs could improve international remittances—but also underscored the need for shared standards and robust international coordination.

3. Coexistence with Cash and Private Digital Money

In 2024, the project’s director Ketil Watne stated:

“If a CBDC is issued, it will coexist with cash and private digital currencies.”

This vision emphasizes complementarity, not replacement—but Norway still believes such coexistence is unnecessary for now.

Wholesale CBDCs: Future Potential, Limited Present Value

Norway acknowledged that wholesale CBDCs may modernize interbank settlement, increase transparency, or automate financial processes. However:

- No standardized infrastructure currently exists.

- Benefits remain unproven.

- Global interoperability frameworks are still missing.

This lack of maturity is one reason Norway is choosing prudence over haste.

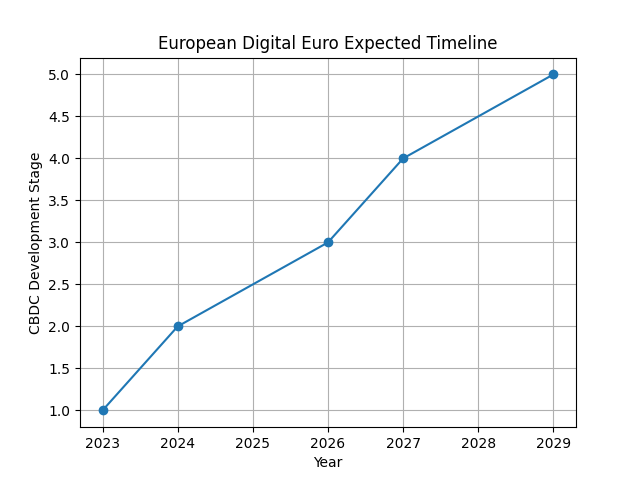

Europe Moves Ahead: The Digital Euro Targeted for 2029

In contrast to Norway’s caution, the European Central Bank (ECB) is advancing toward a digital euro.

ECB’s Projected Timeline

The ECB announced:

- 2026 – Legislative approval expected

- 2027 – Pilot operations could begin

- 2029 – Earliest potential initial issuance

The digital euro is positioned as a complement to cash and bank deposits, with goals such as:

- strengthening Europe’s monetary sovereignty

- providing a public digital payment option

- ensuring payment competition and resilience

Norway is watching closely and may adopt solutions compatible with European CBDC infrastructure—an important point for any business or platform seeking multi-jurisdictional compliance.

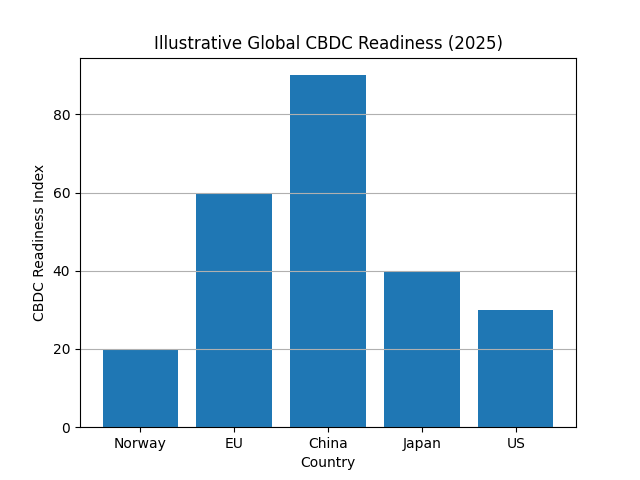

Global CBDC Trends: Fragmented and Uneven

Despite media narratives, global CBDC development is highly uneven.

To illustrate this, Chart 2 provides an illustrative global CBDC readiness index (simplified).

China is far ahead, already distributing digital yuan in commercial scenarios. The European Union is progressing steadily. The U.S. remains cautious, emphasizing privacy and political concerns.

Norway sits in the low-readiness tier—not due to lack of capability, but because of its assessment that a CBDC is unnecessary under current conditions.

Why Norway’s Decision Matters for Crypto Investors

Norway’s pause is more than a policy choice—it highlights several structural factors that influence the relationship between CBDCs, stablecoins, and cryptocurrencies.1. Mature Payment Systems Reduce the Need for CBDCs

In countries where private digital payments are already:

- low-cost

- fast

- reliable

- highly adopted

CBDCs bring fewer benefits. This can create space for stablecoins, especially those fully transparent and compliant.

Stablecoin issuers may find greater adoption in markets where CBDCs are progressing slowly or are deprioritized.2. Blockchain-Based Settlement Still Has Momentum

Even if CBDCs slow down, businesses continue to adopt:

- tokenized real-world assets (RWAs)

- programmable payments via smart contracts

- blockchain settlement layers

This creates new markets for specialized tokens, compliance-focused infrastructure providers, and cross-border payment networks.3. Global Fragmentation Favors Interoperable Private Solutions

When central banks move at different speeds, private solutions can fill interoperability gaps:

- multi-chain stablecoins

- tokenized FX and remittance rails

- decentralized liquidity hubs

- hybrid custodial/non-custodial payment platforms

Projects that offer cross-chain, cross-jurisdiction settlement stand to benefit the most.4. CBDC Uncertainty Increases the Strategic Value of Decentralized Assets

Norway’s statement reinforces that CBDCs are not guaranteed to be rolled out universally.

For crypto investors, this suggests:

- Bitcoin and Ethereum maintain their independent value proposition.

- Alternative Layer-1s and modular chains can position themselves as payment layers where CBDCs are absent.

- Interoperability protocols (layer-zero networks, cross-chain bridges) retain long-term importance.

The Future: Will Norway Eventually Adopt a CBDC?

Norway made it clear that it has not closed the door.

Potential conditions that could trigger adoption:

- decreasing cash usage beyond safe thresholds

- dominance of private payment providers causing systemic risk

- increased cyber-threats targeting payment infrastructure

- international pressure to harmonize with European CBDC standards

Norway is technologically ready but strategically cautious—waiting to see whether the global ecosystem matures.

Conclusion: What Norway’s CBDC Pause Means for the Digital Asset Landscape

Norway’s decision demonstrates that CBDCs are not inevitable, especially in countries with strong private payment infrastructures. While Europe pushes forward and China leads the world, other advanced economies are choosing patience.

For the blockchain and crypto ecosystem, this creates significant opportunities:

- Stablecoins may fill the void where CBDCs are delayed.

- Cross-border crypto payment platforms can expand where national solutions lag behind.

- Tokenization and programmable finance remain compelling regardless of CBDC progress.

- Interoperable, regulation-ready digital asset networks will become increasingly valuable.

For investors seeking new crypto assets or blockchain applications, the key takeaway is this:

CBDC hesitation is not a slowdown for blockchain—it is an opening.