Main Points:

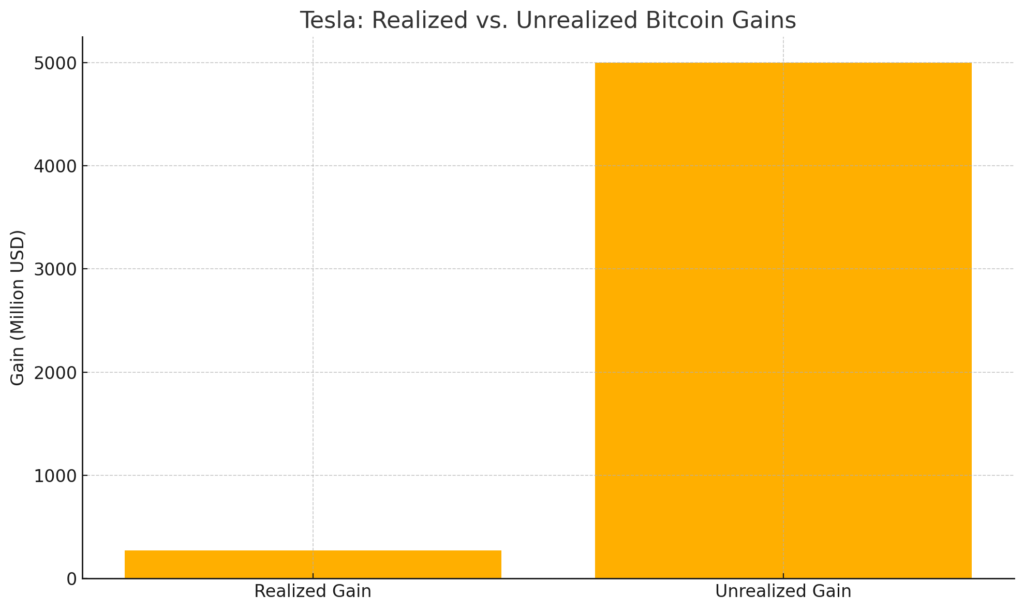

- Tesla’s July 2021 sale realized $272 million but forfeited potential paper gains that could have reached $5 billion by mid-2025.

- Bitcoin’s high volatility offers both opportunity and significant risk for corporate balance sheets.

- Strategic objectives—liquidity, ESG, inflation hedge—must guide any corporate crypto allocation.

- Japanese firms can benefit by defining clear goals, building robust risk-management frameworks (derivatives, diversification), and engaging tax/accounting experts early.

1. Tesla’s Regret: Realized vs. Unrealized Gains

In February 2021, Tesla announced a $1.5 billion purchase of Bitcoin, immediately positioning itself among the first major corporations to embrace crypto on its balance sheet. By July 2021, Tesla sold part of its holdings, locking in $272 million of realized gains while citing liquidity needs and ESG considerations. Yet, by mid-2025, the remaining Bitcoin position would have appreciated to an estimated $5 billion—an unrealized gain magnitudes higher than what was captured .

This “what if” scenario underscores the profound impact of timing decisions on corporate finances. While the $272 million realized profit improved short-term liquidity, Tesla missed out on a multi-billion-dollar windfall had it maintained its full position. Such an outcome forces investors and executives alike to confront the dilemma: seize certain—but modest—gains now, or ride out volatility for potentially extraordinary returns.

[Insert Chart 1: Realized vs. Unrealized Bitcoin Gains by Tesla]

2. A New Frontier in Corporate Finance: Valuation Upside vs. Volatility

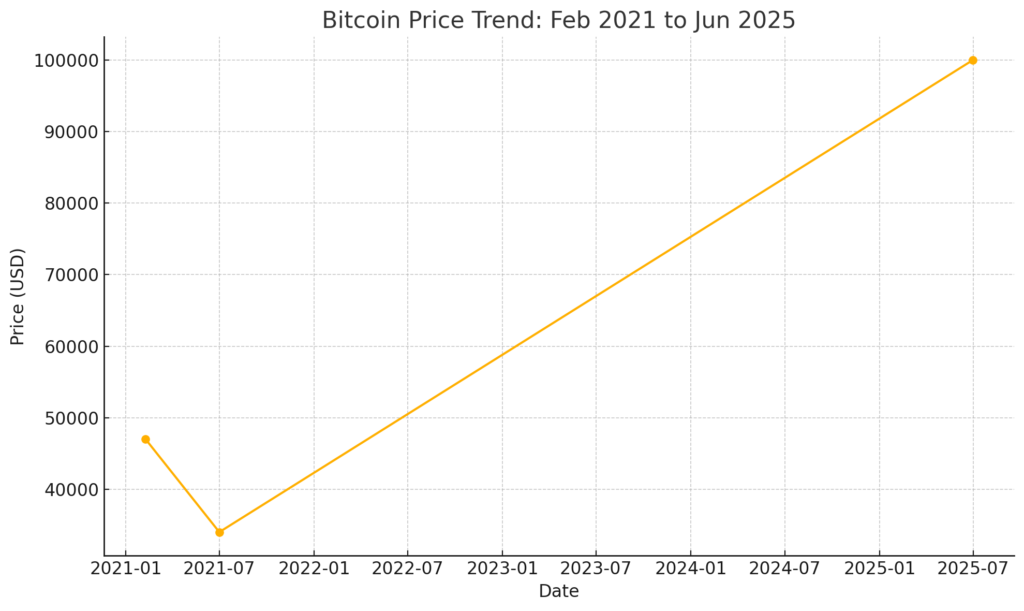

Bitcoin’s allure stems from its pronounced price swings. On one hand, corporations can achieve outsized returns, as Tesla did following its initial purchase when prices surged. On the other hand, the same volatility can generate steep drawdowns: Bitcoin plunged from around $47,000 on February 8, 2021, to $34,000 by July 1, 2021, before climbing past $100,000 by mid-2025 .

[Insert Chart 2: Bitcoin Price Trend: Feb 2021 to Jun 2025]

For finance teams accustomed to predictable asset classes, absorbing Bitcoin’s volatility demands new methodologies. Traditional metrics—beta, Value at Risk (VaR), and stress-testing—must be recalibrated for this digital asset. Moreover, directors and CFOs need to balance the upside potential against downside scenarios when presenting forecasts to stakeholders.

3. Aligning Strategic Objectives with Crypto Allocations

Integrating Bitcoin into a corporate treasury is not a purely speculative move. Companies must ground their crypto strategies in clearly defined objectives:

- Liquidity Management: As Tesla demonstrated, converting crypto to cash can address short-term capital needs, but firms should determine threshold levels for profit-taking.

- ESG Considerations: Energy consumption concerns around proof-of-work mining may conflict with sustainability goals. Firms might opt for carbon-offset purchases or only hold Bitcoin if vetted against ESG criteria.

- Inflation Hedge: With rising global inflation, Bitcoin’s fixed supply can offer a hedge, akin to digital gold. However, hedge ratios—percent of treasury exposure—should be set judiciously.

Establishing a formal policy document that outlines trigger events (e.g., price targets, macroeconomic shifts) for buying or selling Bitcoin helps avoid ad hoc decisions driven by market emotions.

4. Risk-Management Frameworks: Diversification and Derivatives

No corporate treasury should hold Bitcoin in isolation. Key risk-mitigation tactics include:

- Portfolio Diversification: Blend Bitcoin with other assets (e.g., government bonds, equities) to smooth overall volatility.

- Derivatives Usage: Employ futures, options, or swaps to hedge directional exposure or to lock in profits. For instance, put options can cap downside risk while preserving upside potential.

- Dynamic Rebalancing: Automate rebalancing rules (e.g., sell 10% of gains once portfolio Bitcoin allocation exceeds 3% of total assets) to maintain risk tolerances.

Collaboration between treasury, risk, and accounting teams is vital. Bitcoin’s classification under accounting standards (e.g., IFRS, US GAAP) may result in impairment-only models, affecting how unrealized gains and losses flow through financial statements.

5. Implications for Japanese Corporations

Japanese firms, long accustomed to low-yield government bonds, now face an inflection point. To harness Bitcoin:

- Define Clear Investment Goals: Is crypto a short-term trading play, an inflation hedge, or part of a broader strategic partnership (e.g., tokenization projects)?

- Develop Expert Partnerships: Engage external advisors—legal, tax, and audit—to navigate Japanese regulations, BSP guidelines for crypto, and potential tax treatments of digital asset gains.

- Implement Incremental Pilots: Start with small, controlled allocations. Use sandbox approaches to test workflows, custodial solutions, and reporting before scaling up.

- Adopt Transparent Reporting: Share policy rationales and performance metrics with stakeholders to build confidence and comply with disclosure norms.

By learning from Tesla’s pioneering steps—both its successes and its “missed” opportunities—Japanese companies can craft bespoke crypto strategies aligned with corporate values and risk appetites.

Conclusion

Tesla’s decision to sell a portion of its Bitcoin holdings in July 2021 yields a cautionary tale: realized profits are tangible, but unrealized gains can dwarf initial returns if volatility favors holders. For corporations worldwide, especially Japanese firms seeking new revenue streams, the key lies in marrying ambition with discipline. Defining strategic objectives, building robust risk frameworks, leveraging derivatives, and consulting experts will enable companies to navigate the emerging frontier of corporate crypto. As blockchain’s real-world applications expand—from treasury diversification to tokenized assets—the firms that balance foresight with prudence stand to thrive in the next era of digital finance.