Main Points :

- Monet Bank, owned by billionaire Andy Beal—one of Donald Trump’s major financial backers—is entering the crypto-focused banking sector with custody, lending, and blockchain-based transaction services.

- The move aligns with the Trump administration’s rapid rollout of crypto-friendly regulatory reforms, including withdrawal of prior restrictions and new guidance encouraging banks to support digital-asset businesses.

- Monet Bank joins a wave of new U.S. institutions—such as Erebor Bank and N3XT—that are building fully-regulated, blockchain-native financial infrastructure.

- The developments signal a turning point for investors, exchanges, and Web3 payment networks as traditional banking rails merge with programmable money.

- For crypto investors and builders, these moves open pathways for liquidity, institutional trust, and new business models in prediction markets, tokenization, settlement layers, and stablecoin infrastructure.

Introduction: A Traditional Regional Bank Steps Into the Digital-Asset Future

In December 2025, The Information reported that Monet Bank—a Texas-based community bank with under $6 billion in assets and about $1 billion in capital—formally declared its intention to become a cryptocurrency-specialized financial institution.

The transition is notable not only because of the bank’s small size, but because it is owned by Andy Beal, a real-estate magnate and one of the most influential supporters of President Donald Trump.

Beal’s decision to pivot Monet Bank into digital-asset banking arrives at a moment when U.S. federal regulators are rolling back earlier restrictions on crypto engagement and introducing a more predictable regulatory framework. As a result, Monet Bank’s move is widely seen by industry insiders as a symbolic green light for the next stage of U.S. institutional crypto adoption.

1. Background: Who Owns Monet Bank and Why This Matters

Monet Bank—originally Beal Savings Bank established in 1988—underwent several name changes before adopting its current identity. Today, it operates under FDIC oversight and Texas state banking regulation, ensuring customer deposits remain federally insured.

Andy Beal, its owner, is well-known for his contrarian investment strategy. During crises such as the 2001 California energy crisis, post-9/11 airline bond downturn, and the 2008 financial crisis, Beal purchased deeply distressed assets and later sold them for enormous gains.

His entry into the digital-asset arena suggests that he perceives the crypto banking sector as both undervalued and strategically important—consistent with his history of entering markets just before they evolve into mainstream opportunities.

For crypto investors, Beal’s involvement signals the arrival of a new class of institutional liquidity providers: high-capital, risk-tolerant, politically connected traditional bankers.

2. Monet Bank’s Crypto Services: What Exactly Will It Offer?

Monet Bank intends to offer the following services across its six branches:

• Crypto Custody

Bank-grade secure storage of Bitcoin, Ethereum, and other digital assets using cold-wallet and multi-sig frameworks. This is essential for institutional clients who require FDIC-regulated operational standards.

• Crypto Lending

Collateral-backed lending using digital assets—potentially enabling traders, funds, and corporates to access USD liquidity without liquidating positions.

• Blockchain-Enabled Transactions

Support for on-chain payment rails, likely including stablecoins and tokenized dollar settlements.

• Digital-Asset Integrations with FDIC-Insured Deposits

A particularly important feature: FDIC insurance will apply only to fiat deposits, not crypto balances—but the operational oversight and risk management will be held to federal banking standards.

This combination positions Monet Bank as a hybrid institution bridging traditional banking reliability with the efficiency of blockchain-based settlement.

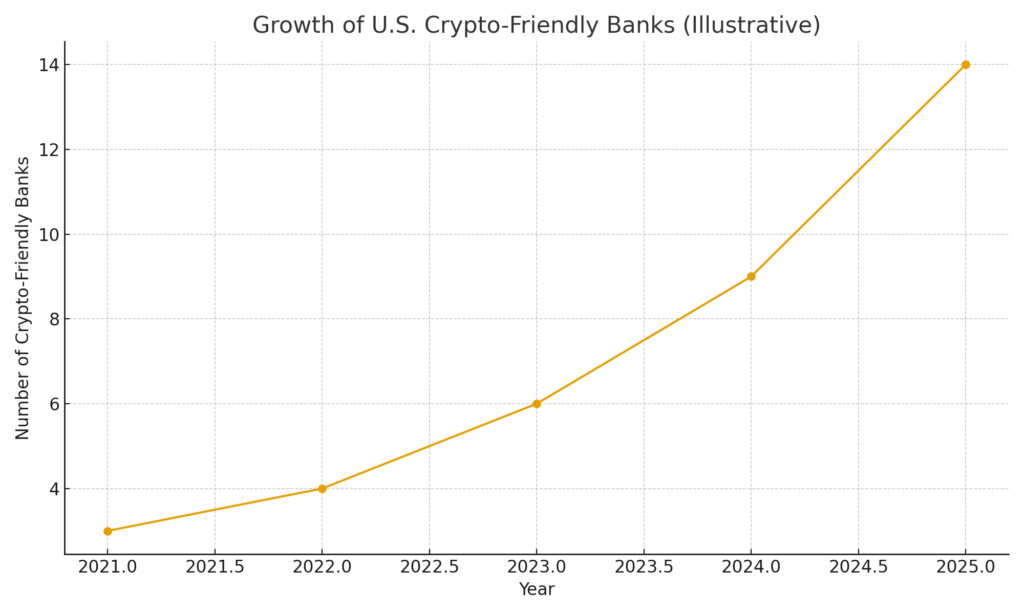

3. The Surge of U.S. Crypto-Friendly Banks

Monet Bank is not alone; crypto-aligned banks are increasing.

- Erebor Bank, backed by Peter Thiel, received conditional approval from the OCC in October 2025.

- N3XT, founded by former Signature Bank executives, launched in December 2025 as a full-reserve blockchain-native bank, leveraging Wyoming’s SPDI framework.

- These institutions are building new clearing, settlement, and liquidity models relying on tokenized dollars and programmable transactions.

Below is an illustrative chart showing the growth in the number of U.S. crypto-friendly banks:

4. Regulatory Context: The Trump Administration’s Crypto Pivot

Under the Trump administration, regulators have rapidly changed course from the restrictive stance seen in 2022–2023. Key developments include:

• Withdrawal of earlier warnings that discouraged banks from engaging with crypto customers.

Federal agencies previously expressed concern that digital-asset firms presented heightened liquidity and fraud risks. Those guidelines have now been removed.

• Introduction of new “crypto-access guidance” for banks.

The updated guidance encourages institutions to build infrastructure supporting tokenization, programmable payments, and custody operations.

• OCC Chief Jonathan Gould’s statement

Upon approving Erebor Bank, Gould emphasized that the OCC does not impose blanket barriers on banks seeking to run digital-asset operations.

• FDIC Acting Chair Travis Hill’s remarks

Hill indicated that the FDIC will propose its own regulatory framework for stablecoins—particularly relevant for banks offering blockchain-based USD settlement.

This represents the strongest federal push yet toward legitimizing digital-asset finance.

5. Why Monet Bank’s Entry Matters for Investors and Web3 Builders

• Institutional Liquidity Is Expanding

Banks reentering the crypto market provide deeper liquidity pools for exchanges, prediction markets, lending platforms, and token issuers.

• Banks Provide Trust and Onboarding Infrastructure

Regulated bank custody is crucial for large institutions, pension funds, and corporates that cannot self-custody assets.

• Opens the Door to U.S. Dollar Tokenization at Scale

Banks like N3XT and Monet may pioneer fiat-backed programmable dollars, enabling real-time settlement for B2B payments.

• Better Rails for On/Off-Ramps

Crypto-native businesses—especially those supporting USDC, tokenized securities, or Web3 gaming—gain reliable, compliant rails for customer deposits, withdrawals, and settlements.

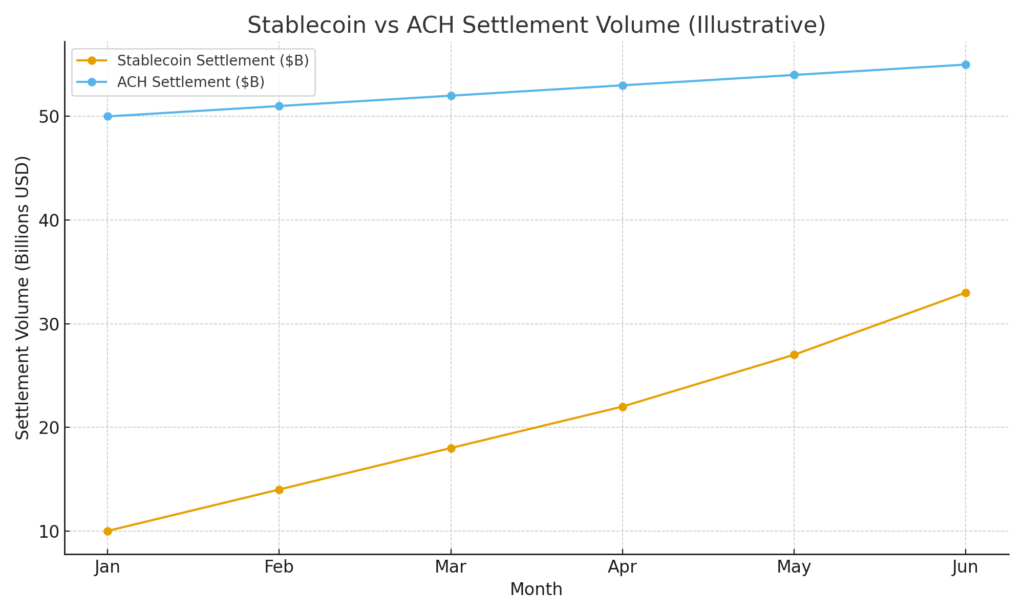

6. A Parallel Trend: Stablecoin Usage Is Quietly Surging

According to market data, stablecoin settlement volumes now rival or exceed some traditional ACH payment flows. To illustrate:

This trend reveals growing corporate and institutional comfort in using digital dollars for cross-border transfers, treasury operations, and automated payouts.

Monet Bank’s new services align perfectly with this macro trajectory.

7. Industry Reactions: “A Milestone Moment”

Crypto industry leaders and fintech executives responded positively to Monet Bank’s announcement:

- “This is the liquidity breakthrough we’ve been waiting for.”

- “The return of U.S. crypto banking is the catalyst for the next bull market.”

- “Programmable dollars backed by FDIC-regulated institutions will redefine how businesses settle payments.”

There is a clear expectation that crypto banking—long constrained by debanking waves—will experience renewed growth and stability.

8. What This Means for Crypto Investors Seeking New Opportunities

For readers exploring new tokens, yield opportunities, and practical blockchain applications, several insights emerge:

1. Tokenization Platforms Will Expand

Real-world asset (RWA) protocols may partner with banks for compliant issuance.

2. Prediction Platforms, Gaming Finance, and On-Chain Derivatives May Become Safer

As banks integrate with Web3 rails, compliance-compatible versions of these services may flourish.

3. USD Yield Products May Reemerge

Full-reserve banks like N3XT could enable yield opportunities based on blockchain settlement fees rather than lending risk.

4. Liquidity Migration Will Favor U.S.-Regulated Institutions

Investors may increasingly prefer exchanges and wallets connected to compliant U.S. banks.

Conclusion: A New Phase of U.S. Crypto Banking Has Begun

Monet Bank’s pivot into crypto finance marks a pivotal moment for the U.S. digital-asset ecosystem.

With regulatory frameworks stabilizing, new full-reserve and hybrid banks emerging, and traditional institutions preparing to tokenize dollars and streamline settlements, the sector is entering a growth phase backed by political, financial, and technological momentum.

For investors, builders, and businesses seeking new revenue models, this new class of crypto-integrated banks represents:

- A return of institutional trust

- A surge of compliant liquidity

- New rails for global payments

- And the foundation of a more programmable financial future

The U.S. crypto banking revival is no longer theoretical—it has already begun.