Key Points :

- Coinbase argues that the current U.S. anti-money-laundering (AML) framework — rooted in the Bank Secrecy Act and related 1970s-era rules — is outdated, ineffective and burdensome.

- Rather than stricter rules, Coinbase proposes regulation that emphasises innovation: safe harbours for AI & APIs, recognition of decentralised identity (DID) and zero-knowledge proofs, and the use of blockchain analytics and Know-Your-Transaction (KYT) monitoring.

- The U.S. regulatory environment for digital assets is shifting rapidly in 2025: laws like the GENIUS Act for stablecoins have been passed, while regulators emphasise technology-driven compliance.

- For blockchain practitioners, institutional crypto investors and revenue-seeking participants, this means both opportunity (more clarity, more tech tools, potential new business models) and risk (regulatory uncertainty, compliance burdens, technology investment).

- The momentum suggests a strategic pivot: rather than “crypto needs to be stopped” the message is increasingly “crypto needs to be governed — intelligently, technologically, and with performance focus”.

1. Why Coinbase Is Calling for a Rewrite

In October 2025, Coinbase submitted a detailed response to the United States Department of the Treasury’s request for comment on “innovative methods to detect illicit activity involving digital assets”. The core argument: the Bank Secrecy Act and associated AML regulations were designed decades ago when banking activity looked very different — mostly wire transfers, traditional financial intermediaries, clear KYC/AML paths. In crypto, with decentralised ledgers, pseudonymous wallets, token transfers and global flows, the old tools struggle to keep up.

Coinbase contends that:

- The current system forces firms to collect massive volumes of low-value data (e.g., suspicious activity reports, SARs) that flood regulators but rarely stop sophisticated crimes.

- Consumer privacy is compromised because KYC/AML regimes demand broad personal data collection even when risk is low.

- Criminals use technology and innovation to adapt — “bad guys innovate” — therefore the “good guys” (i.e., regulated firms, compliance teams) must adopt innovative methods too. As Coinbase’s Chief Legal Officer Paul Grewal wrote, “When bad actors innovate, good actors must keep pace.”

For the reading audience — those exploring new crypto opportunities or blockchain use-cases — this background matters: it signals that the regulatory regime might shift from a passive, historical “compliance box-checking” system to an active, innovation-first system.

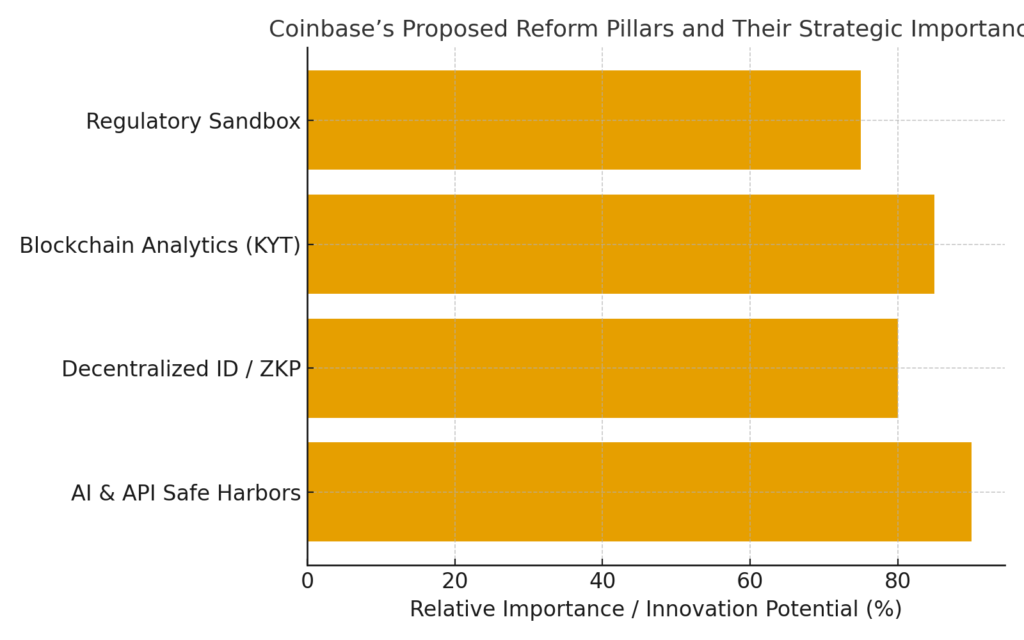

2. The Four Reform Pillars Coinbase Proposes

In its submission (approximately 30 pages long according to public press), Coinbase outlines four key reforms. For people researching crypto revenue models or blockchain application opportunities, each of these suggests concrete operational or strategic implications.

2.1 Safe Harbours for AI & APIs

Coinbase proposes that firms using artificial intelligence, machine learning, and API-driven compliance solutions be given regulatory “safe harbours” — meaning that the firm will face less regulatory risk if it meets defined governance and outcome criteria. The idea is to lower the barrier for firms to deploy real-time transaction monitoring, anomaly detection, wallet-graph analytics, rather than relying on human-intensive, retrospective SAR filings.

For you: if you are building a blockchain-based compliance tool, or thinking of offering “wallet monitoring analytics” as a service, this suggests regulators are at least open to receiving such solutions — which may become part of the compliance market.

2.2 Decentralised ID and Zero-Knowledge Proofs for KYC

Next, Coinbase argues that customer verification (KYC) does not have to rely entirely on traditional identity documents; instead, decentralised identity (DID) frameworks and zero-knowledge‐proofs (ZKPs) can fulfil the regulatory goals (identifying customer, verifying risk) without exposing all personal data. This is significant: it means blockchain firms may be able to reduce the data burden and privacy risk, which aligns well with Web3 ethos, while still meeting compliance corridors.

2.3 Blockchain Analytics / Know-Your-Transaction over Traditional SARs

Rather than focusing on generic suspicious activity reports (SARs) from fiat banking era, Coinbase suggests embracing transaction-flow analysis, wallet clustering, real-time blockchain monitoring (sometimes called Know-Your-Transaction, KYT) as more effective. For blockchain engineers or data scientists this is an invitation: the compliance function is increasingly technical. Firms that build strong monitoring of token flows, identify illicit clusters, use machine learning, will likely be ahead.

2.4 A Regulatory Sandbox / Public-Private Collaboration

Finally, Coinbase calls for stronger cooperation between private firms and regulators via a sandbox model — regulated firms and the Treasury (or other agencies) can test new compliance models before formal rules are applied. This can accelerate innovation while maintaining oversight. For blockchain & crypto businesses, this is a potential doorway: if you have an innovative startup, you might be able to participate in early regulatory frameworks, which can provide competitive advantage.

3. The Broader U.S. Regulatory Landscape (and Implications for Practitioners)

Understanding Coinbase’s ask is useful, but for context it’s important to see how the broader U.S. regulatory environment is shifting — because this affects market opportunities, risk profiles and business models.

3.1 Landmark Legislation & Stablecoin Framework

In 2025 the U.S. passed the GENIUS Act, which creates a federal framework for stablecoins (cryptos pegged to the U.S. dollar or other low-risk assets) and clarifies banks’ roles in issuing them. This is a major structural development: it means the “wild-west” era for stablecoins is being replaced with clearer rules. For someone looking for new revenue streams, stablecoin issuance or token-backed services may become more accessible under regulated regimes.

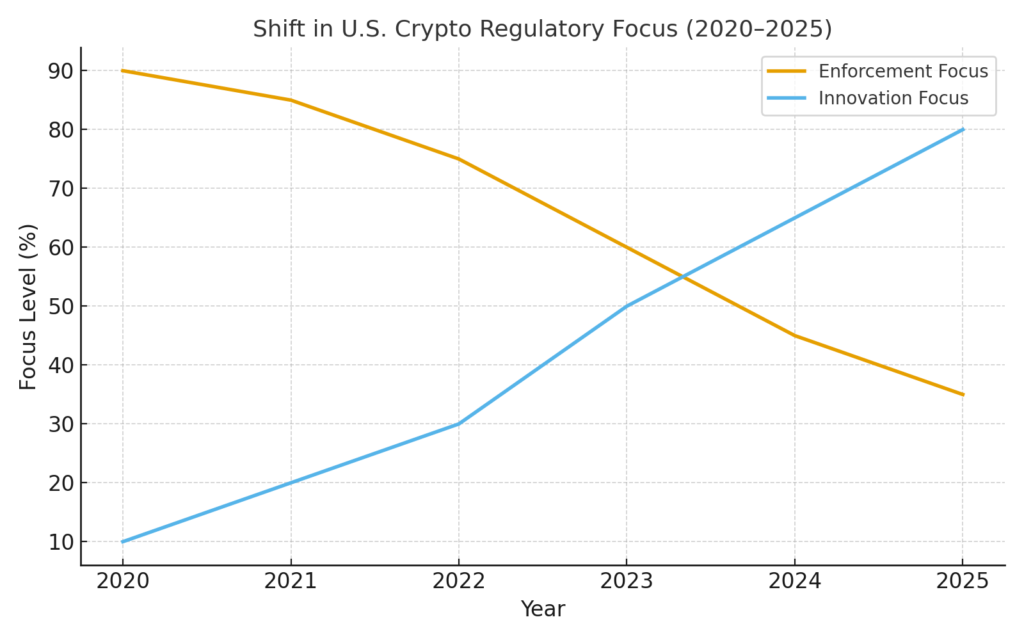

3.2 Shift from Enforcement to Innovation

Concurrently the U.S. political mood regarding crypto is shifting: instead of pure crack-down, the language is more about “govern and innovate”. As one commentary puts it: “after years of avoidance, the United States is now building a regulatory structure for digital assets.” For business-minded individuals, this means regulatory uncertainty may decline, but compliance expectations will rise. It is less about “avoid being shut down” and more about “comply and scale”.

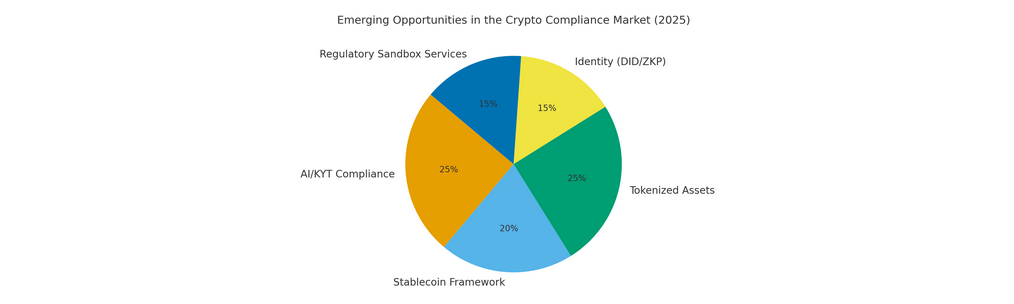

3.3 What This Means for Blockchain Use-Cases and Revenue Models

From a practical viewpoint, the shift has three implications:

- Compliance as a Service: There is an emerging market for firms offering blockchain-analytics/KYT/AI-monitoring. These could become services to exchanges, wallet providers, or DeFi platforms.

- Tokenised Assets and On-Chain Use-Cases: With stablecoin clarity and AML reform, tokenisation of real-world assets (RWAs), token-native payments or wallets integrated with institutional rails may become more mainstream.

- Competitive advantage from tech-first firms: Firms that build compliant systems using innovative technologies (e.g., DIDs/ZKPs/blockchain analytics) can differentiate themselves and perhaps benefit from regulatory sandboxes or safe harbour pathways. For investors seeking new crypto assets or service-businesses, companies enabling these capabilities may be worth watching.

4. Risks and Strategic Considerations for Investors and Builders

While the reform momentum is an opportunity, it is not without caution — for someone looking for new assets or revenue models, you should weigh the following:

- Implementation risk: Even if safe harbours are proposed, actual regulatory rule-making takes time and may vary across agencies. Coinbase’s submission does not guarantee fast regulatory change.

- Technology and cost burden: Deploying AI systems, blockchain analytics, DID/ZKP infrastructure requires investment; smaller startups may struggle to compete unless they partner or carve niche functions.

- Global regulatory mismatch: The Financial Stability Board (FSB) warns global crypto regulation remains uneven, which means cross-border business will face patchwork rules.

- Compliance vs usability trade-off: As more tech tools are introduced, balancing privacy, speed and compliance will remain tricky. For example, using zero-knowledge proofs may protect user data but still satisfy regulators — but these systems are relatively nascent.

- Asset risk for new crypto offerings: If you’re seeking new crypto assets or service tokens, note that regulatory clarity for token classification remains in flux (security vs commodity). The CLARITY Act and others are still evolving.

5. Practical Takeaways for You: What to Do Now

If you’re exploring new revenue sources in crypto or blockchain use cases, here are actionable ideas derived from this reform context:

- Scan for compliance-enabling tools: Consider building or investing in protocols that help firms meet AML/KYT/identity needs (e.g., wallet-graph analytics, DID infrastructure, real-time token monitoring).

- Keep eyes on regulated stablecoins and tokenisation: With the GENIUS Act and stablecoin clarity, new financial products may become viable — tokenised real-world assets (RWAs), institutional stablecoin issuance, wallet-based payment rails.

- Explore sandbox-friendly jurisdictions: If U.S. regulators move toward sandboxes, some firms may pilot early models. Seek partnership opportunities.

- Monitor asset classification changes: For new crypto assets you may invest in or build, the distinction between security, commodity, and payment token still matters — regulatory shifts could affect value.

- Manage compliance burden from the start: If you are launching a blockchain project (exchange, wallet, DEX, token), embed compliance/review from design-phase — regulators are signalling expectation of tech-driven compliance, not ignoring it.

6. Conclusion

In sum, Coinbase’s push to modernise U.S. AML rules for crypto is not just a corporate lobbying document — it represents a strategic inflection point for the digital assets ecosystem. For investors, blockchain practitioners and service-builders, the message is clear: the future of crypto is increasingly one where innovation and compliance are twin priorities.

Where once the narrative was “crypto needs to be stopped or regulated into oblivion”, we are now entering a phase where “crypto can scale, but must do so in ways that meet modern compliance, technology and transparency expectations”. That environment not only reduces some of the regulatory uncertainty, but creates new business models around compliance, analytics, identity, tokenisation and institutional-grade crypto infrastructure.

If you are looking for your next revenue stream in blockchain, the interplay between innovation and regulation is your opportunity — build or partner with firms that provide the compliance-tech backbone, engage with the new stablecoin rails, and consider tokenised asset models that are increasingly permitted. The risk is not regulatory prohibition per se but failure to meet the emerging compliance and technology expectations. In the coming years, those who innovate with regulators — rather than in spite of them — are likely to capture disproportionate value.