Main Points :

- CleanSpark has surpassed 13,000 BTC holdings, marking a strategic pivot from selling to long-term treasury accumulation

- Miners’ shift to “holding” reduces direct market supply and may intensify supply scarcity ahead of the halving

- This behavior can amplify volatility, increase institutional linkages, and change how investors analyze supply-side metrics

- Japanese and global investors should monitor miner balance sheets, corporate BTC treasury strategies, and indirect exposure via equities

- The broader mining industry is evolving: capital structure innovations, energy sourcing, and competition over clean power shape future profitability

1. CleanSpark’s Milestone and the New Strategy of Miner Treasury Accumulation

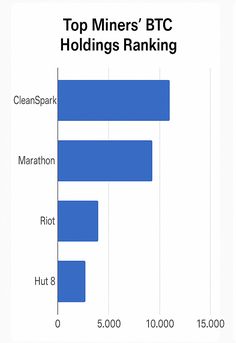

In September 2025, CleanSpark reported that its self-mined Bitcoin holdings had exceeded 13,000 BTC, achieving a key milestone in its operational disclosures. According to its September mining update, the company mined 629 BTC in that month and sold 445 of them (for roughly $49 million) while retaining the remainder. Its total treasury now positions CleanSpark among the top public Bitcoin holders.

This move reflects a deliberate shift in strategy. Rather than selling freshly mined coins to cover operating expenses, CleanSpark is treating Bitcoin itself as a productive capital asset—a treasury reserve that supports growth and potentially generates returns beyond just mining margins. In effect, the company is partly internalizing the notion that Bitcoin’s long-term upside justifies absorbing more of the downside short-term risks, such as energy cost volatility or infrastructure investment.

CleanSpark’s published metrics show improved operational efficiency: average fleet efficiency reached 16.07 J/Th, and the average hashrate hovered around 45.6 EH/s during September. The company also boasts enhanced financial flexibility, having arranged a notable $400 million in Bitcoin-backed credit facilities and issued convertible instruments to support growth.

These developments underscore that CleanSpark is not merely scaling its mining hardware but reshaping its economic model around BTC reserves.

2. What the Miner-to-Hodler Shift Means for Bitcoin’s Supply Structure

2.1 From Seller to Accumulator: The Strategic “Hodling” Paradigm

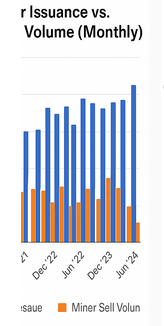

Historically, miners have functioned as essential sellers of newly minted Bitcoin: mining revenue would typically be converted into fiat to cover electricity, maintenance, expansion, and debt obligations. That dynamic imposed a steady supply pressure onto crypto markets.

However, CleanSpark’s pivot—and analogous moves by other miners—signals a transition toward “strategic hodling.” In this paradigm, miners deliberately retain a larger portion of mined BTC as a form of treasury or reserve, rather than liquidating immediately.

This shift has profound implications. Because mined supply is no longer automatically fed into the open market, net market supply shrinks, potentially amplifying scarcity effects. In other words, even before a halving event, miner behavior can mimic a supply contraction.

2.2 Advancing the Halving Effect: Supply Shock in Advance

Bitcoin’s protocol enforces a halving event roughly every four years, cutting the block subsidy (new issuance) by 50%. That predictable supply shock has long been a cornerstone of Bitcoin’s valuation thesis.

But if miners voluntarily withhold supply, then the effective issuance to markets can decrease well ahead of the protocol halving. The result: the market may begin to price in “tightness” earlier, compressing the window of arbitrage and possibly increasing volatility.

Moreover, as miners increasingly internalize beliefs about long-term BTC appreciation, their behavior might compress the traditional “sell zone” after price spikes. Markets may see sharper upswings and flatter declines if miners act less as sellers and more as strategic holders.

2.3 Implications for Institutional and Retail Demand

Beyond supply constriction, this shift delivers structural support for institutional traction. As miners treat Bitcoin as a core treasury asset, their equity performance becomes more correlated with Bitcoin price—offering indirect exposure to traditional investors who prefer securities over direct crypto holdings.

This dynamic could create a feedback loop: strong miner treasury strategies attract investor capital, further reinforcing BTC price strength, which in turn emboldens more hoarding.

At the same time, the narrative moves from pure mining ROI to corporate finance and capital allocation. Investors will increasingly scrutinize miner disclosures—the ratio of mined versus sold BTC, capital expenditures, debt structures, and energy sourcing.

3. Recent Trends & Industry Signals

To place CleanSpark’s move in a broader context, let us examine some of the notable trends and signals emerging in 2025.

3.1 Supply Squeeze Driven by Corporate and ETF Demand

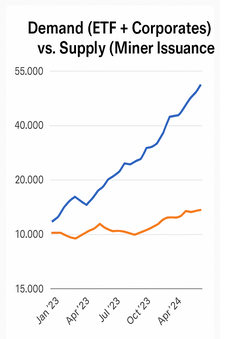

Michael Saylor has publicly noted that in 2025, businesses are reportedly acquiring 1,755 BTC per day, while ETFs are acquiring another 1,430 BTC per day—figures which outstrip daily miner issuance. n other words, demand from treasuries and passive instruments now exceeds supply from mining alone—a potential tipping point.

This inversion signals that pure issuance alone cannot meet buyer appetite, making accumulated BTC held off-chain critical for price support.

3.2 Miner Business Model Diversification & AI/Crypto Convergence

VanEck’s mid-2025 ChainCheck commentary highlights that miners are receiving re-ratings as they pivot into adjacent domains such as AI, hosting, and compute services. The convergence of compute-intensive workloads (e.g., AI inference, HPC) with mining infrastructure is reshaping expectations: miners are no longer one-dimensional crypto play but hybrid infrastructure operators.

Under that framework, a miner’s capacity to allocate power, cooling, and server infrastructure to flexible workloads can stabilize revenues beyond BTC mining margins.

3.3 Energy Strategy and Geographic Shifts

CleanSpark is not alone in reevaluating energy strategies. Globally, mining firms are hunting for cheaper and more sustainable power, negotiating with utilities and positioning operations near surplus renewable energy grids. For instance, several crypto firms are exploring projects in Brazil to capitalize on renewable energy oversupply.

Similarly, mining gear manufacturers (Bitmain, Canaan, MicroBT) are investing in U.S.-based production to sidestep tariffs and optimize supply chains. These moves not only reduce sourcing constraints but also align hardware availability with evolving miner demand.

3.4 Profitability Pressure and Strategic Risk

It’s worth noting that the shift to holding reserves is not without risk. Miners must maintain capital discipline, absorb energy cost swings, and manage leverage. A prolonged Bitcoin downturn or energy price spike could stress balance sheets that bet heavily on hodling.

Moreover, game-theoretic strategies such as “selfish mining” become increasingly relevant in models where not all coins are immediately sold. Recent academic work shows selective withholding of blocks (or manipulative mining strategies) may yield additional advantage when rewards (including fees) are volatile. As miners hoard, incentive structures shift subtly.

4. What This Means for Japanese and Global Investors

4.1 Reassess Supply Metrics Beyond Circulating Supply

In evaluating Bitcoin’s supply-side dynamics, investors should move beyond simple “circulating supply” models to net market supply — i.e. issuance minus miner selling. Miner disclosures (in quarterly reports) of mined vs. sold BTC, treasury balances, and relative sales ratios should become core inputs into price forecasting models.

In the Japanese context, where exchanges and regulatory transparency may lag, these disclosures provide a rare window into future supply constraints hidden behind headline figures.

4.2 Indirect Exposure via Miner Equities

Rather than buying Bitcoin directly, Japanese institutional or retail investors can access BTC exposure through publicly listed mining companies. Stocks of miners that maintain sizeable BTC treasuries effectively become leveraged bets on Bitcoin’s long-term trajectory.

However, this route carries correlation risk, operational risk, and exposure to regional regulations, so due diligence on balance sheets, energy contracts, and capital structure is crucial.

4.3 Allocate with a Long-Term Mindset

Miner behavior suggests that Bitcoin is increasingly viewed not just as a speculative asset, but as a strategic reserve asset—a hedge against inflation, currency depreciation, or monetary debasement. Aligning one’s portfolio with that longer horizon, rather than focusing on frequent trading, may yield better risk-adjusted returns.

For Japanese investors confronting low interest rates and economy-wide deflationary pressure, Bitcoin’s fixed supply logic becomes more compelling in diversified portfolios.

4.4 Watch for Macro and Regulatory Shocks

Structural moves like miners hoarding increase sensitivity to regulation, taxation, or macro shocks. A change in electricity pricing, a clampdown on cryptocurrency reserves in corporate balance sheets, or central bank policy shifts could upend these strategies. Thus, portfolio risk management must be continuous.

5. Forecasts, Risks, and Strategic Takeaways

5.1 Price Outlooks and Market Sentiment

Analysts remain bullish: for instance, VanEck projects Bitcoin could reach $180,000 by end-2025, assuming favorable ETF inflows, institutional momentum, and macro tailwinds. Others suggest even more aggressive targets near $200,000+ if supply constraints and demand exceed expectations.

Adding weight to that bullish thesis is the fact that 99.4% of Bitcoin supply is currently in profit, signaling generally positive market sentiment.

Yet, risks exist: a regulatory crackdown, macro liquidity reversal, or miner insolvency under extended downturns could lead to abrupt corrections.

5.2 Structural Risks in the Miner-Hodler Regime

- Liquidity mismatch: If miners hoard too much, short-term cash needs may push abrupt sales under stress, creating cascade effects.

- Operational leverage: As miners accumulate BTC, they lock capital into non-yielding reserves, reducing flexibility in cost shocks.

- Adversarial mining behavior: Strategic withholdings or tactics like selfish mining can exploit miner collusion in tighter issuance regimes.

- Regulation over reserves: Tax authorities or securities commissions might redefine how BTC held on corporate balance sheets are treated—possible valuation, capital, or reserve implications.

5.3 Strategic Recommendations for Investors

- Track miner disclosures meticulously: Mined vs. sold BTC ratios, reserve growth, capital facility terms.

- Diversify across exposure routes: Combine direct BTC allocations, miner equities, and protocol-level opportunities to mitigate correlated risks.

- Favor miners with clean energy and operational flexibility: These firms better survive volatility.

- Adopt scenario-based models: Simulate aggressive supply constriction and shock unwind paths.

- Maintain optionality: Keep liquidity to respond to forced sellings or market repricing.

Conclusion

CleanSpark’s surpassing of 13,000 BTC is far more than a milestone—it embodies what may be a structural reorientation in how Bitcoin’s supply dynamics unfold. Miners are no longer mere suppliers to the market, but strategic holders of the asset itself. That shift creates downstream effects: accelerating scarcity ahead of halving, intertwining mining equity performance with Bitcoin returns, and reshaping investment models.

For forward-looking investors—especially in Japan and Asia—the task is clear: elevate your analysis from demand-side narratives to supply-side disclosures. Monitor miner treasury behavior, understand the capital and energy models underpinning them, and think in multi-year frames. The coming cycle may reward those who see not just the next trading opportunity, but the evolving role of Bitcoin in finance, corporate treasury, and capital formation.