Main Points :

- Mastercard is reportedly in advanced negotiations to acquire ZeroHash for approximately $1.5 billion to $2 billion.

- ZeroHash is an API‐first crypto & stablecoin infrastructure startup that enables banks, fintechs and brokerages to integrate crypto trading, custody, tokenization and settlement.

- The move signals a major push by Mastercard into stablecoin settlement rails and tokenisation of real-world assets, aligning with the broader trend of legacy financial firms embracing blockchain rails.

- Institutional interest in stablecoins and tokenisation is rising: ZeroHash reported over $2 billion of tokenised fund flows in a four-month period.

- Regulatory momentum (in the US and EU) around stablecoins is strengthening, making infrastructure plays like ZeroHash increasingly strategic for payments firms.

1. The Deal in Context

According to multiple sources, Mastercard is in late-stage talks to acquire ZeroHash for about $1.5 billion to $2 billion. While neither company has officially commented, the magnitude of this deal (if it closes) would represent one of Mastercard’s largest investments into blockchain infrastructure to date.

The timing is significant. Mastercard previously pursued another stablecoin/start-up target, BVNK (London-based), in a deal reportedly around the $2 billion mark—though it appears to have been outbid by Coinbase. That loss likely accelerated Mastercard’s pivot toward ZeroHash, with a view to gain control of tokenisation and settlement infrastructure rather than just supporting integrations.

For crypto investors and infrastructure watchers, this deal (if completed) signals that major payments networks view blockchain rails—especially stablecoins—as core infrastructure, not niche add-ons. Mastercard appears to be preparing to own the plumbing rather than just hitching onto it.

2. Why ZeroHash Matters

ZeroHash, founded in 2017 and based in Chicago, operates as an API-first infrastructure provider. It enables financial institutions (banks, fintechs, brokerages) to embed crypto trading, custody, stablecoin transfers, tokenisation of assets and settlement into their existing platforms.

Key data points:

- It processed over $2 billion in tokenised fund flows during a recent four-month period.

- It supports major tokenised funds: for instance, with clients like BlackRock’s “BUIDL” initiative, Franklin Templeton’s “BENJI Token”, Hamilton Lane’s HLPIF.

What this means: ZeroHash doesn’t only focus on retail crypto trading; it provides the backbone for tokenised asset flows and institutional settlement. In the context of our audience—searching for new crypto assets, yield opportunities, and practical blockchain applications—ZeroHash’s model suggests several implications:

- Tokenisation of traditional assets (funds, real estate, securities) is gaining traction. ZeroHash’s infrastructure may drive growth in this sector.

- Stablecoins as settlement rails are increasingly being embedded into fintech/financial platforms via infrastructure providers like ZeroHash.

- For developers or wallet projects (for example, you in the context of your non‐custodial wallet “dzilla Wallet”), the trend means more API‐driven infrastructure options for integrating tokenisation and stablecoin rails.

3. Implications for the Payments & Crypto Ecosystem

Elevated Strategic Significance

This acquisition push showcases that payment networks (Mastercard, Visa, etc.) are moving beyond pilot blockchain projects into acquiring full infrastructure stacks. As one analyst put it: “Whoever owns those rails will own the flow of value in the next decade.”

Mastercard’s prospective bid aligns with other moves: for instance, a prior partnership with fintech firm Fiserv to integrate a stablecoin (FIUSD) into its network. Meanwhile, the broader regulatory environment is clarifying, reducing one major barrier to large-scale stablecoin adoption.

What This Means for Crypto Assets & Infrastructure

For the crypto investor or ecosystem builder, here are key take-aways:

- Stablecoins are becoming strategic settlement rails. Institutions that issue or integrate stablecoins may gain first-mover advantage.

- Tokenisation infrastructure is accelerating. Firms like ZeroHash demonstrate that traditional firms are ready for tokenised real-world assets. New asset classes may emerge, and liquidity could shift.

- Partnerships/integrations will proliferate. Non-custodial wallets, fintechs, and tokenisation projects should monitor how payments giants integrate stablecoin rails—this may open new business/model opportunities.

- Regulatory clarity boosts adoption. As stablecoin regulation consolidates (especially in the U.S. and Europe), previously high‐risk infrastructure plays become more viable.

Potential Risks & Considerations

- The deal is not yet finalised; acquisitions can fall through, valuations may change.

- Integrating blockchain infrastructure within large legacy systems is operationally complex (compliance, AML/KYC, etc.).

- While payments firms accelerate, regulatory risk remains (e.g., stablecoin reserves, redemption rights, cross-border flows).

- For investors in crypto assets: the strategic focus is shifting from speculative tokens to infrastructure and settlement rails—asset selection criteria may need adaptation.

4. Trends to Watch & Opportunities

a. Tokenised Asset Growth

With infrastructure providers such as ZeroHash already processing billions in tokenised flows, look for asset classes being tokenised (private equity, real estate, funds). Projects enabling interoperability or scaling token-issuance may present new investment or integration opportunities.

b. Wallet & Infra Integration

Given your background in developing a non-custodial wallet (dzilla Wallet), the consolidation of infrastructure (e.g., payments network + stablecoin rails) means wallets that integrate tokenisation, custody, trading, and stablecoin rails will likely gain competitive edge. Explore how APIs from firms like ZeroHash can plug into wallet UX flow (swap, settlement, tokenised asset issuance).

c. Stablecoins as Payment Rails

Stablecoins are not just trading tokens—they increasingly serve as settlement systems. Payments firms see them as cheaper and faster alternatives to traditional rails. This opens scope for blockchain payments, cross-border remittances, and business settlement models. For potential token launches, integrating a stablecoin or using a partner’s stablecoin rail could enhance utility.

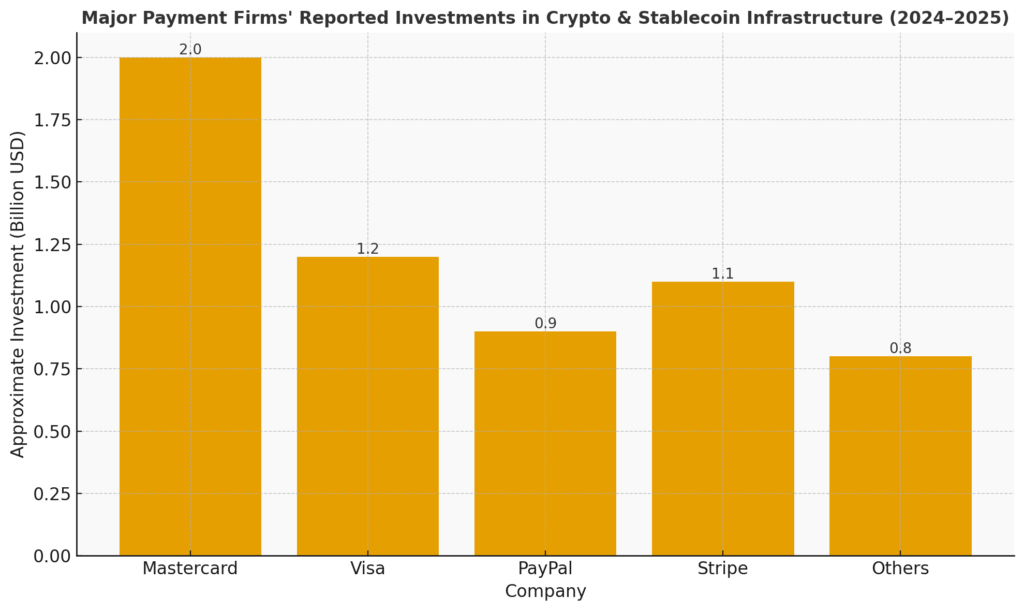

d. Competitive Landscape Among Payment Giants

Mastercard isn’t alone: Visa, Stripe, PayPal and others are expanding in stablecoin and tokenisation spaces. For projects, aligning or integrating with these rails could accelerate adoption vs going solo.

e. Regulatory & Compliance Frameworks

As stablecoin legislation becomes clearer (e.g., in the U.S. and EU) the infrastructure risk reduces. Projects that build compliance-friendly token rails (e.g., full-reserve backing, transparent audits) may have lower regulatory friction and higher institutional uptake.

5. What This Means for New Crypto Assets & Revenue Sources

For Investors:

- Look beyond tokens alone: infrastructure plays (stablecoin rails, tokenisation platforms) may deliver long-term value rather than pure speculation.

- Assets tied to tokenised real-world asset projects could benefit from accelerating institutional flows facilitated by firms like ZeroHash.

- Stablecoin-linked yield mechanisms (e.g., settlement, marketplaces) might gain traction when integrated with payments networks.

For Builders/Wallet & Platform Developers:

- Integrate stablecoin rails and token-issuance capabilities early. If major payments networks support wallets that connect to tokenised asset flows, being compliant and UX-friendly is a differentiator.

- Leverage API infrastructure: ZeroHash’s model shows that APIs for tokenisation, trading, settlement exist and are accessible—think of assembling modular stacks rather than building everything in-house.

- Explore value-added services: tokenised fund flows, asset on-boarding, institutional settlement—wallets that serve as gateways for these use cases may unlock new revenue streams beyond retail trading.

- Stay compliant: As major players enter infrastructure, regulatory scrutiny rises—embedding compliance by design helps scale.

Conclusion

The reported acquisition of ZeroHash by Mastercard for up to $2 billion marks a watershed moment in crypto and payments infrastructure. It underlines the shift from crypto being a fringe asset class toward stablecoins, tokenisation and blockchain rails being central to the next generation of global payments. For investors and builders, this means the real action lies not just in speculative tokens, but in the plumbing of blockchain finance: token-issuance, settlement, and infrastructure. The journey ahead will reward those who understand how traditional finance meets blockchain—wallets like yours (dzilla Wallet) that integrate tokenised assets, stablecoin rails and institutional flows may well capitalise on this trend. As stablecoin regulation becomes clearer and institutional flows rise, the next crypto infrastructure cycle is likely already underway.