Main Points :

- Robert Kiyosaki warns of a potential historic market crash in 2026, possibly worse than the 2008 Global Financial Crisis

- Structural weaknesses from 2008—especially excessive global debt and fragile credit markets—remain unresolved

- Rising stress in private credit markets, including actions by BlackRock, may signal systemic risk

- Retirement funds, especially for aging populations, are highly exposed to market downturns

- Kiyosaki recommends hard assets and crypto, including Bitcoin and Ethereum, as hedges

- Broader macro trends—interest rates, inflation, and liquidity tightening—support the possibility of volatility

1. A Renewed Warning: Echoes of Past Crises

Robert Kiyosaki, best known as the author of Rich Dad Poor Dad, has once again issued a stark warning: the global financial system may be heading toward a historic collapse in 2026. His thesis is not based on short-term volatility, but rather on long-term structural imbalances that have persisted since the 2008 financial crisis.

In his earlier work Rich Dad’s Prophecy (2013), Kiyosaki predicted a massive market crash driven by systemic fragility. More than a decade later, he argues that the very conditions that caused the collapse of Lehman Brothers—excessive leverage, opaque financial instruments, and overdependence on credit—have not only remained but intensified.

From his perspective, the global financial system has been artificially stabilized through monetary expansion and debt accumulation. Central banks injected liquidity, governments expanded fiscal deficits, and financial institutions continued to innovate new credit products. While these measures postponed collapse, they did not resolve the core vulnerabilities.

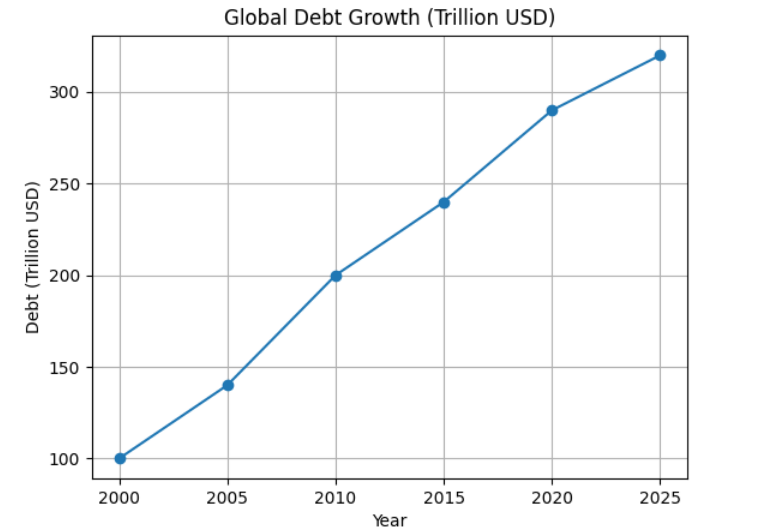

Today, global debt levels—sovereign, corporate, and consumer—have reached unprecedented highs. According to various international estimates, global debt now exceeds $300 trillion. This creates a fragile environment where even minor disruptions in liquidity or credit availability could cascade into systemic failure.

2. Private Credit: The Hidden Fault Line

A central theme in Kiyosaki’s latest warning is the rise of private credit markets. Unlike traditional banking systems, private credit operates largely outside strict regulatory oversight. It involves direct lending by asset managers, hedge funds, and institutional investors to corporations and projects.

Kiyosaki has specifically pointed to concerns surrounding large asset managers such as BlackRock. In early 2026, reports emerged that certain private credit funds limited withdrawals due to a surge in redemption requests. While such measures are often described as “liquidity management,” they can also signal deeper stress within the system.

Private credit has grown rapidly over the past decade, filling the gap left by banks after stricter post-2008 regulations. However, this growth has introduced new risks:

- Liquidity mismatch: Investors expect short-term access to funds, while underlying loans are long-term and illiquid

- Opaque risk structures: Limited transparency compared to public markets

- Concentration risk: Large funds dominating segments of the lending market

Kiyosaki goes as far as calling parts of the private credit ecosystem a “Ponzi-like structure,” arguing that it relies on continuous inflows to sustain valuations. While this characterization is controversial, it reflects growing concerns among analysts about the sustainability of the sector.

3. Debt Saturation and Systemic Fragility

At the core of the argument lies a simple but powerful idea: the world is drowning in debt.

From government bonds to consumer loans, debt has become the foundation of modern economic growth. However, this growth model assumes continuous expansion and stable interest rates. As central banks raise rates to combat inflation, the cost of servicing debt increases dramatically.

This creates a feedback loop:

- Higher interest rates increase debt servicing costs

- Borrowers struggle to meet obligations

- Credit markets tighten

- Asset prices decline

- Financial institutions face losses

Kiyosaki warns that this cycle could accelerate rapidly once confidence begins to erode. Unlike 2008, where the crisis was largely concentrated in housing and banking, the next downturn could be more widespread due to the interconnectedness of global markets.

4. The Retirement Crisis: A Silent Risk

One of the most concerning implications of a major market downturn is its impact on retirement savings.

Pension funds, retirement accounts, and institutional portfolios are heavily invested in equities, bonds, and alternative assets—including private credit. A sharp decline in asset values could significantly erode these savings, particularly for aging populations such as baby boomers.

Kiyosaki emphasizes that many individuals are unaware of the extent to which their retirement funds are exposed to market risk. In a severe downturn, not only could portfolios decline in value, but liquidity constraints could limit access to funds when they are needed most.

This risk is compounded by demographic trends. As populations age, more individuals rely on their accumulated savings rather than active income. A major market correction at this stage of life could have long-lasting consequences.

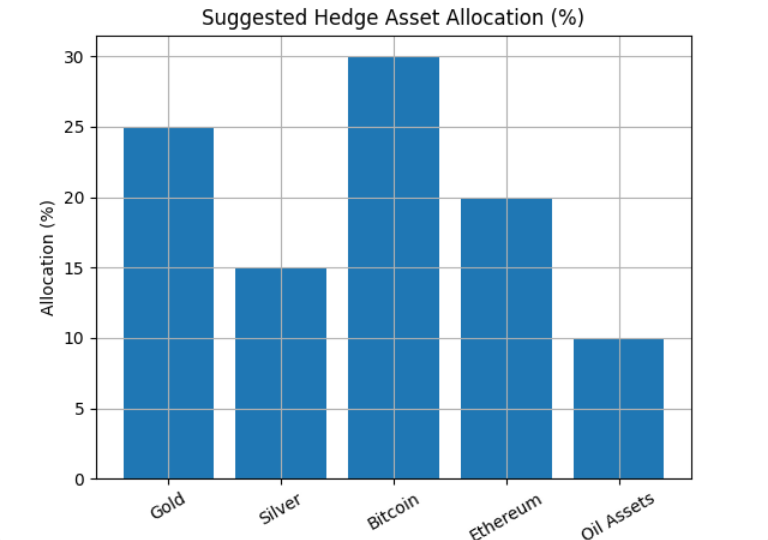

5. Crypto and Hard Assets as Strategic Hedges

In response to these risks, Kiyosaki advocates for a shift toward tangible and decentralized assets. His recommendations include gold, silver, energy assets such as oil wells, and cryptocurrencies.

Cryptocurrencies, particularly Bitcoin and Ethereum, have emerged as alternative stores of value in recent years. While volatile, they offer several characteristics that appeal to investors concerned about systemic risk:

- Decentralization: Not controlled by any single government or institution

- Limited supply (in the case of Bitcoin)

- Global accessibility and liquidity

Institutional adoption has also increased, with major financial firms integrating crypto into their offerings. Exchange-traded funds (ETFs), custody solutions, and regulatory clarity in some jurisdictions have contributed to broader acceptance.

At the same time, gold and silver continue to serve as traditional hedges against inflation and currency devaluation. Energy assets provide exposure to real economic activity and can benefit from supply constraints or geopolitical tensions.

Kiyosaki’s strategy reflects a broader trend among investors seeking diversification beyond traditional financial instruments.

6. Current Market Trends: Signals Beneath the Surface

Beyond Kiyosaki’s warnings, several macroeconomic trends support the possibility of increased volatility:

- Persistent inflation pressures despite tightening monetary policy

- Higher-for-longer interest rate expectations, reducing liquidity

- Geopolitical tensions, affecting energy markets and global trade

- Shifts in capital flows, including reduced risk appetite

Crypto markets, interestingly, have shown relative resilience in recent months. While not immune to macroeconomic shocks, they have increasingly behaved as a separate asset class, driven by both technological adoption and speculative interest.

At the same time, equity markets have remained buoyant, supported by strong corporate earnings and technological innovation. This divergence between optimism in equities and caution in credit markets may indicate underlying fragility.

7. A Balanced Perspective: Warning or Opportunity?

It is important to approach Kiyosaki’s predictions with a balanced perspective. While his warnings highlight real risks, they also represent one interpretation of complex global dynamics.

Financial markets are influenced by numerous factors, including policy decisions, technological innovation, and investor behavior. While a severe downturn is possible, it is not inevitable.

For investors, the key takeaway is not necessarily to predict the exact timing of a crash, but to understand the risks and prepare accordingly. This includes:

- Diversifying across asset classes

- Maintaining liquidity

- Monitoring credit market conditions

- Evaluating exposure to systemic risks

Conclusion: Preparing for an Uncertain Future

Robert Kiyosaki’s warning of a potential 2026 market collapse serves as a reminder of the fragility underlying modern financial systems. Whether or not his prediction materializes, the issues he highlights—excessive debt, opaque credit markets, and systemic risk—are real and significant.

For those seeking new opportunities in crypto and blockchain, this environment presents both risks and potential rewards. Decentralized technologies, alternative assets, and innovative financial models may offer pathways to resilience in an increasingly uncertain world.

Ultimately, the future will depend on how governments, institutions, and individuals respond to these challenges. Preparedness, adaptability, and informed decision-making will be critical in navigating what may be one of the most transformative periods in financial history.