Main Points :

- Bank Negara Malaysia (BNM) has launched a three-year roadmap exploring asset tokenization via blockchain.

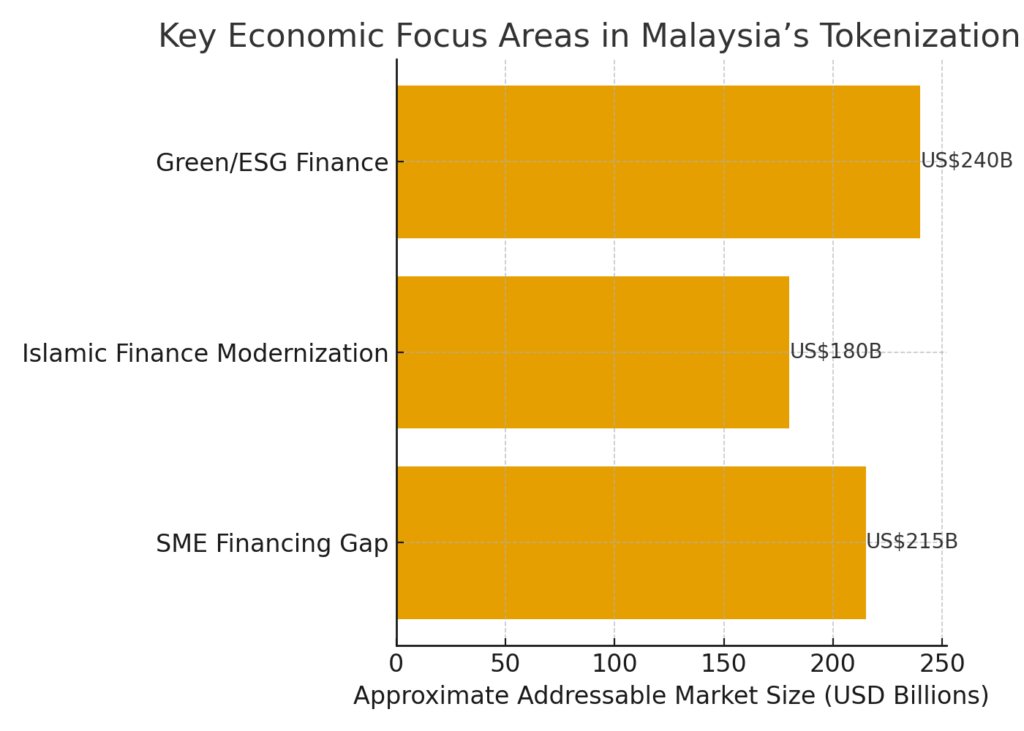

- The initiative emphasises solving concrete economic problems (SME financing gap, Islamic finance, green/ESG-linked finance) rather than toy experiments.

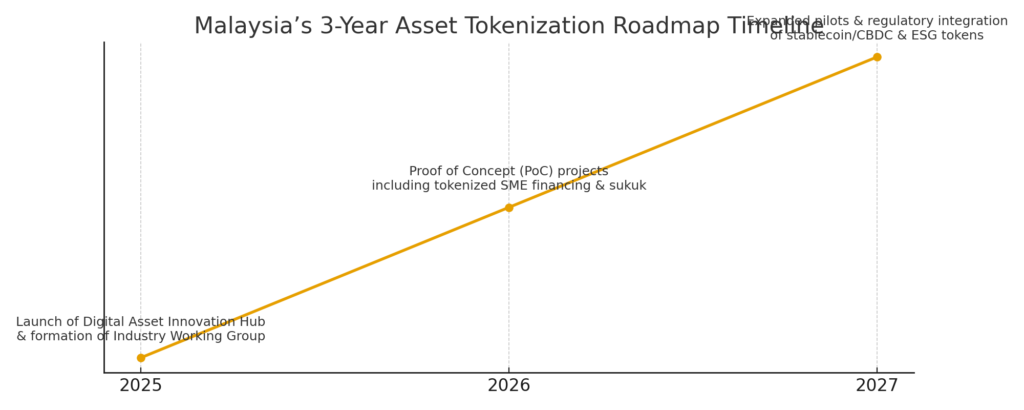

- A dedicated Digital Asset Innovation Hub and an Asset Tokenization Industry Working Group (IWG) will drive proof-of-concepts in 2026 and expanded pilots in 2027.

- The guiding principles: real-world value must be demonstrated; DLT only used when superior to legacy tech; feasibility with current infrastructure is essential.

- Tokenisation use-cases of interest include tokenised invoices and receivables for SMEs, tokenised sukuk (Islamic bonds) via smart contracts, green finance tokens, stablecoin/deposit tokenisation, and integration with wholesale CBDC.

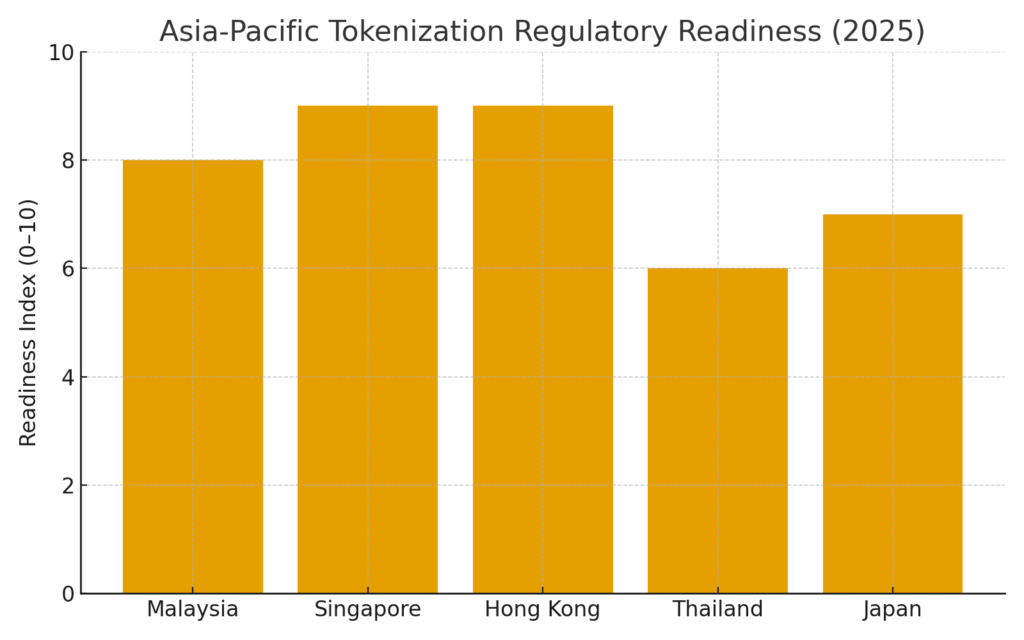

- The roadmap aligns Malaysia with other Asian financial hubs like Monetary Authority of Singapore (MAS) and Hong Kong Monetary Authority (HKMA) in modernising financial infrastructure via tokenisation.

Introduction: A New Chapter for Tokenisation in Asia

In an era where blockchain and digital assets continue bursting into traditional finance, Malaysia has taken a bold step. On 1 November 2025, the Malaysian central bank, Bank Negara Malaysia (BNM), unveiled a three-year roadmap aimed at exploring and implementing asset tokenization across its financial ecosystem.

Unlike many experiments that focus purely on novel tech, this programme is deliberately anchored in solving substantive economic and financial problems—opening a window of opportunity for crypto-asset innovators, blockchain practitioners and investors looking for new revenue streams and real-world applications. For readers seeking next-generation crypto assets, tokenised instruments and practical blockchain utilities, this roadmap offers both direction and signal.

1. The Strategic Framework

BNM’s roadmap is built on a structured timeline and governance architecture.

- First, the establishment of the Digital Asset Innovation Hub (DAIH) creates a regulated sandbox environment where banks, fintechs and blockchain developers can safely experiment under regulatory supervision.

- Second, the formation of the Asset Tokenization Industry Working Group (IWG)—co-led by BNM and the Malaysian Securities Commission—serves as the coordination forum for industry players, regulators and legal/technical experts to share knowledge, surface regulatory issues and steer standards.

- Third, the roadmap adopts a phased timeline: proof-of-concepts (PoCs) in 2026, pilot expansion in 2027, with stakeholder feedback and public consultation open until 1 March 2026.

2. Addressing Real-World Economic Needs

What sets this roadmap apart is its emphasis on tangible economic benefit.—not just “blockchain for blockchain’s sake.”

SME Financing Gap

SMEs in Malaysia face a financing gap estimated at around US $21.5 billion (≈RM 101 billion). BNM envisages tokenising invoice receivables or other supply-chain assets so that smaller companies can unlock liquidity by converting future payments from large anchor buyers into digital tokens, which can then be used as collateral or traded.

Islamic Finance Digitised

Malaysia is a global leader in Islamic finance. Through tokenised sukuk (Islamic bonds) and smart contracts, the roadmap aims to improve automation of payments, enhance liquidity, reduce settlement time and maintain Sharia compliance.

Green Finance & ESG

Tokenisation is extended to green bonds and ESG-linked financing. For example, bonds could be programmed such that payouts are triggered only when verified climate or ESG metrics are met—reducing the risk of “greenwashing” and increasing investor confidence.

Stablecoins and CBDC Integration

The bank is also exploring MYR-denominated tokenised deposits, stablecoins and wholesale CBDC integration—while emphasising the “singleness of money” principle (i.e., preserving the unit of account and payment standard).

3. Guiding Principles for Tokenisation Projects

BNM makes clear that not all ideas will qualify and sets three core principles:

- Demonstrable Real-World Value: Use-cases must show clear economic benefit rather than rely on assumptions or marketing hype.

- Technological Justification: DLT (distributed ledger technology) should only be employed when it is truly superior to existing solutions (e.g., APIs, traditional infrastructure). BNM explicitly acknowledges that conventional tech may remain best for certain business challenges.

- Technical Feasibility: Projects must be feasible within current infrastructure—i.e., not so futuristic they remain theoretical. As maturity grows, more complex use-cases may follow.

4. Implications for Crypto Investors, Blockchain Developers & Practitioners

For those of you engaged in or seeking to engage in crypto assets, tokenisation and practical blockchain applications, this roadmap is a signal worth noting:

- New Asset Types: Tokenised receivables, tokenised sukuk, tokenised green bonds—in effect, real-world asset (RWA) tokenisation—represent new classes of digital assets that may duplicate or complement crypto-native tokens.

- Platform Opportunities: If you’re a blockchain developer (and you mentioned you are a JavaScript developer working with web3.js) the controlled sandbox model may present opportunities to build or integrate with the DAIH environment, especially around smart contract design for tokenised assets.

- Regulatory-First Mindset: Given Malaysia’s permissioned, regulated approach (only licensed financial institutions at first) the environment will favour enterprise-grade, compliance-aware tokenisation rather than purely speculative tokens.

- Time Horizon: The roadmap suggests pilots in 2026, scaling in 2027. So while this is a multi-year play, positioning now may allow you to participate early in infrastructure, tooling or asset issuance.

- Cross-Border and Regional Ripple: Since Malaysia is aligning with peers (Singapore, Hong Kong), there may be regional interoperability implications—if you build a tokenised asset platform in Malaysia it may have broader ASEAN relevance.

5. Recent Developments and Competitive Context

- Outside Malaysia, regulators in Singapore (MAS) and Hong Kong (HKMA) have also been advancing tokenisation pilots, meaning Malaysia’s move is part of a broader regional trend of tokenising financial infrastructure.

- The fact that Malaysia is explicitly emphasising regulated institutions and real-world assets (versus purely cryptocurrencies) suggests a maturation of the digital asset market’s focus from speculation to infrastructure and utility.

- For you as a practitioner developing non-custodial wallet functionality (you mentioned interest in wallet design) this suggests increasing demand for tokenised-asset custody, interoperability and settlement features—especially as real-world assets enter token form.

- For income-seeking crypto investors: tokenisation may open up fractionalised access to assets (e.g., receivables, sukuk) previously reserved for institutional investors. This may represent new yield-oriented token opportunities.

6. Risks and Considerations

While promising, there are factors to keep in mind:

- The permissioned nature may mean tokenised assets are initially closed to only regulated institutions—not retail.

- Technology adoption may face legacy systems inertia; DLT may not always win out if simpler tech suffices (per BNM’s principle).

- Regulatory clarity and legal frameworks (e.g., for smart contracts, tokenised securities, Sharia compliance) remain evolving.

- Market adoption is not guaranteed; PoCs may not scale. The timeline (2026–27) suggests patience is required.

- For crypto assets: if tokenised instruments become available only via closed ecosystems, this may limit decentralised access—though it also raises quality/credibility for first-movers.

Conclusion

Malaysia’s three-year asset tokenisation roadmap signals a meaningful shift from the hype around blockchain to a structured, value-oriented, regulated deployment of tokenised real-world assets. For those seeking the next wave of crypto innovation—whether as developers, investors or ecosystem participants—this offers a timely signal: tokenisation is transitioning into serious financial infrastructure. Because the initiative emphasises real-world problem solving (SME finance, Islamic capital markets, green finance) it is aligned with your stated interest in new crypto assets, income opportunities and practical blockchain use-cases.

If executed well, by 2027 Malaysia may emerge as a regional leader in regulated tokenised finance—and potentially a launchpad for tokenised asset models that can replicate in other jurisdictions. For you as a JavaScript/web3 developer designing wallet and swap systems, now may be an opportune time to consider how your tooling could plug into tokenised-asset ecosystems, handle tokenised debts or liabilities, integrate smart contract automation and support regulatory/compliance features. The next couple of years may be less about “coins to chase” and more about “tokens that represent real-world value”.