Key Points :

- The ESRB (European Systemic Risk Board) has recommended banning multi-issuance stablecoins (tokens issued across multiple jurisdictions) to reduce financial stability risks.

- ECB (European Central Bank) supports this recommendation and cites legal, liquidity, and operational risks from foreign-issued stablecoins.

- Major stablecoin issuers like Circle and Paxos could be impacted in the EU market.

- The MiCA regulatory framework’s ambiguity around multi-issuance stablecoins raises credibility concerns.

- The digital euro initiative is advancing, seeking to provide a sovereign, stable digital payment infrastructure.

- A consortium of European banks is preparing a euro-backed stablecoin compatible with MiCA to compete with dollar-based alternatives (launch expected 2026).

- The move signals Europe’s dual strategy: clamp down on foreign stablecoins while building its own CBDC infrastructure.

- For crypto practitioners and developers, Europe’s evolving rules could reshape how stablecoins, cross-border issuance, and on-chain liquidity are structured.

1. Context: Why the EU is Targeting Multi-Issuance Stablecoins

Stablecoins are digital assets pegged to traditional assets (e.g. US dollar) and typically backed by reserves. However, in a multi-issuance design, the same token (same code, same symbol) may be issued by different entities in different jurisdictions, with separate reserve pools per region. This raises the possibility of reserve mismatch, redemption arbitrage, and regulatory arbitrage.

In Europe, regulators worry that in a crisis, redemption demands from users in one region might drain reserve pools elsewhere, leaving local holders exposed. The ESRB recommendation to ban multi-issuance stablecoins is motivated by concern over legal, operational, liquidity, and financial stability risks at the EU level.

ECB President Christine Lagarde has warned that foreign-issued stablecoins could pose “significant legal, operational, liquidity and financial stability risks at the EU level.” The core fear is that foreign issuers might not comply with EU rules during stress, hindering redemption or cooperation.

Thus, the EU is trying to close a loophole: although MiCA (Markets in Crypto-Assets Regulation) already imposes rules on stablecoin issuance, its text is ambiguous about treating foreign versions of the “same” token as identical to EU-issued versions. Some regulators argue that this ambiguity undermines MiCA’s credibility.

2. Implications for Major Stablecoin Issuers: Circle, Paxos, USDC, etc.

Because Circle, Paxos, and other U.S. (or non-EU) stablecoin issuers issue tokens (e.g. USDC) globally — often via affiliates or licensing in various jurisdictions — the proposed ban or stricter oversight may significantly affect their EU operations. Even though Circle is MiCA-compliant for its EU operations, the multi-issuance model where US-origin issuance and EU issuance are fungible raises regulatory scrutiny.

These firms may be forced to segregate issuance strictly by jurisdiction (no cross-fungibility), localize reserves, or cease operations in certain EU markets. The ESRB recommendation is not legally binding, but it would exert strong pressure on national regulators to act.

In parallel, at the Sibos 2025 conference in Frankfurt, a clear transatlantic divide emerged: U.S. officials and Fed-aligned voices emphasize innovation and global stablecoin adoption, while European central bankers stress monetary control and risks of destabilization.

3. MiCA’s Ambiguity and Internal EU Disagreements

MiCA (Markets in Crypto-Assets Regulation) came into force to regulate stablecoins and crypto assets in the EU, but the law lacks clear prohibitions on multi-jurisdiction issuance. This gap has led to conflicting interpretations by EU Commission officials, central bankers, and national regulators.

Some EU Commission actors believe that interchangeable issuance is permissible under MiCA, while ECB and ESRB-backed regulators reject that view as dangerous.

For example, Bank of Italy Deputy Governor Chiara Scotti has called for clearer rules to avoid regulatory fragmentation and confusion. If such ambiguity remains, investors and projects may cite it to challenge national measures, weakening enforcement.

Therefore, the fight over multi-issuance stablecoins is also a test of the EU’s ability to enforce unified crypto standards. If MiCA is perceived as teetering under internal tension, external observers may lose confidence in Europe as a regulatory safe haven.

4. The Digital Euro: Europe’s Sovereign Response

While cracking down on multi-issuance stablecoins, the EU is concurrently accelerating its digital euro (CBDC) efforts. The digital euro is envisioned as a public, central bank–issued digital currency that complements cash, offering a safe, trusted electronic form of (central bank) money.

The ECB has been exploring this project since 2021, and in its “preparation phase” (launched November 2023), it is working with member central banks to define design, privacy, distribution, and resilience. Executive board member Piero Cipollone has indicated that EU member states might reach agreement by year-end 2025. The target earliest deployment is around 2029.

The rationale is that by having a strong, trusted digital euro in public hands, Europe can reduce dependence on privately issued (especially dollar-based) stablecoins, thereby preserving monetary sovereignty.

However, political back-and-forth continues. ECB President Lagarde has urged the European Parliament to fast-track the legislation underpinning the digital euro law—suggesting an autumn 2025 decision could be possible. Some studies estimate disruption to commercial banks, with deposit outflows estimated in the tens of billions of euros.

Yet, proponents argue the digital euro is essential to anchor Europe’s digital payments system and ensure that citizens have access to safe, central bank–guaranteed money even in a digital age.

5. European Private Sector Response: A Euro-Denominated Stablecoin Consortium

To offer an alternative to U.S.-dominated stablecoins, a group of nine major European banks (including ING, UniCredit, CaixaBank, DekaBank, SEB, KBC, Raiffeisen, etc.) has formed a consortium to issue a euro-backed stablecoin under MiCA standards, with an expected launch in the second half of 2026.

This initiative signals that Europe is not simply banning external competition — it plans to compete. The goal is to offer a payments and settlement token native to Europe, leveraging blockchain programmability and real-time settlement capabilities.

Even though ECB has expressed caution toward privately issued stablecoins, this project is structured to comply with MiCA and to be EU-based, aiming to avoid regulatory backlash.

If successful, this euro stablecoin could plug into DeFi rails, support tokenized asset settlement, and become the eurozone’s programmable money infrastructure. But it must navigate challenges: governance, reserve transparency, custodial risk, regulatory licensing, and trust.

6. Recent Developments and Global Trends (2025 Update)

- At the Sibos 2025 conference, U.S. and European central bankers openly diverged. Federal Reserve Governor Christopher Waller expressed strong support for private stablecoins and innovation. Meanwhile, European counterparts warned of systemic risk and defended central bank primacy.

- The Bank of England also recently called for regulating widely used stablecoins like banks (with depositor protections), reflecting a trend of stricter regulation in G7 jurisdictions.

- The European Commission has signaled that it may treat stablecoins issued outside the EU as equivalent to compliant ones inside, downplaying jurisdictional origin as decisive — a stance critics say undermines ECB concerns.

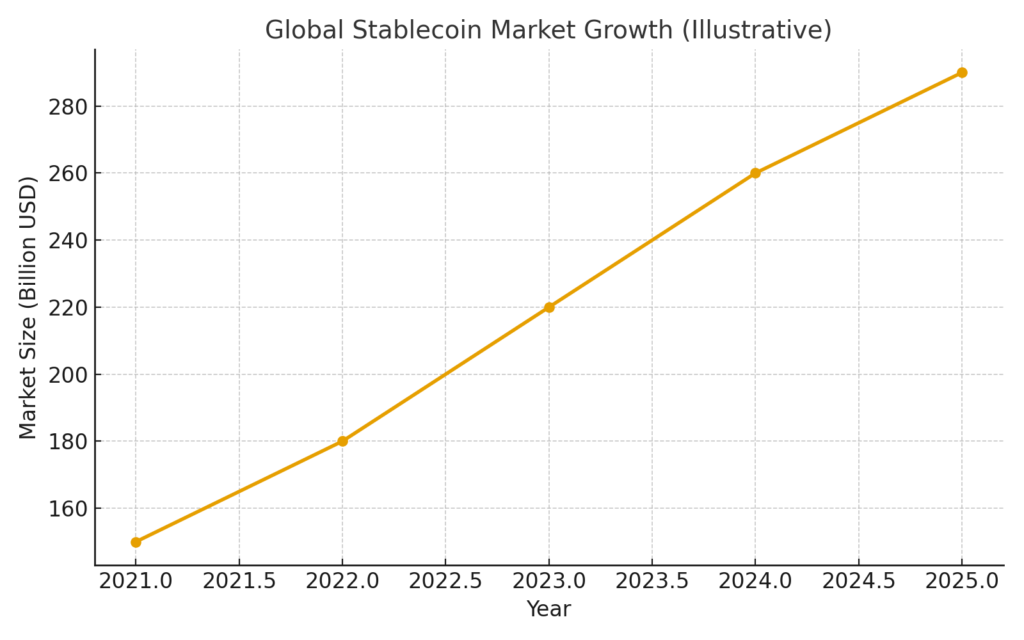

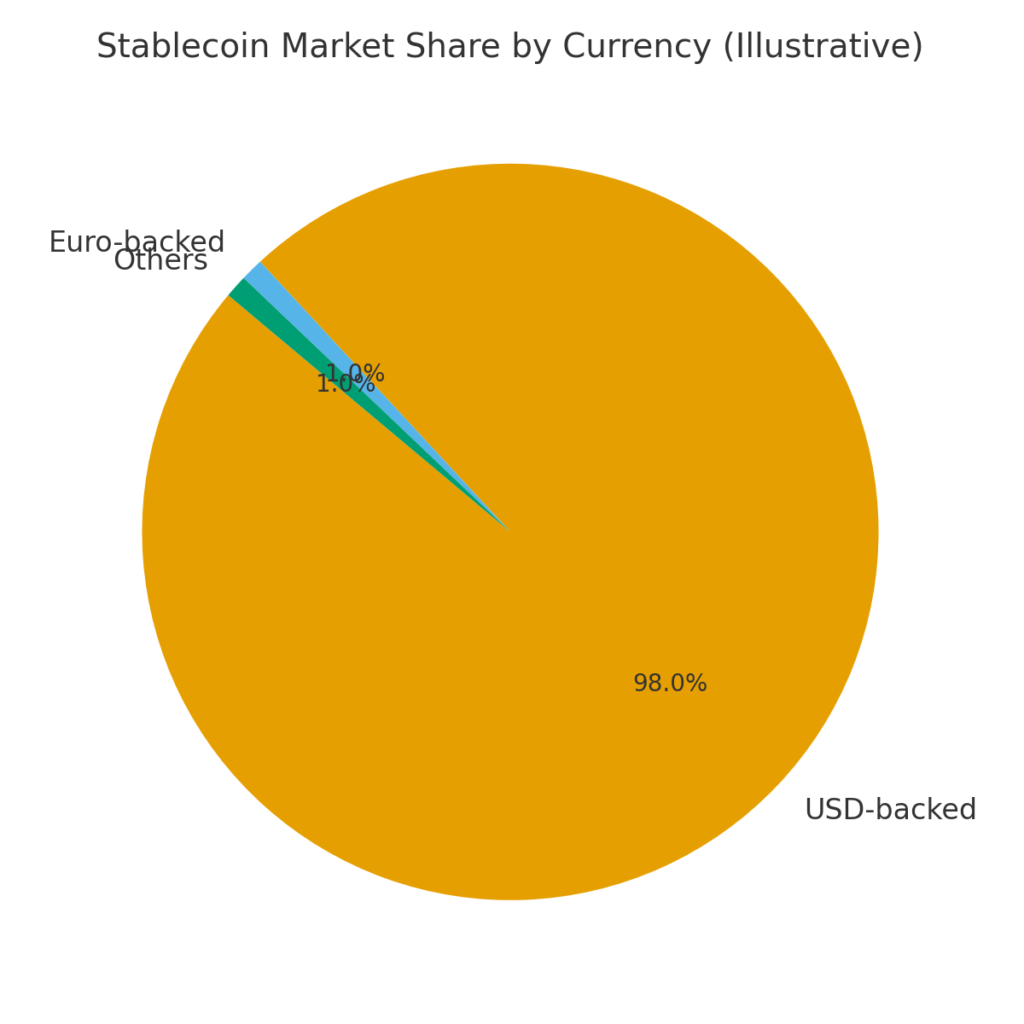

- With the global stablecoin market exceeding $290 billion, EU-denominated stablecoins remain massively underrepresented (only ≈ $620 million).

- The cross-jurisdiction tension is intensifying. As the U.S. introduced the GENIUS Act to enable stablecoin issuance by banks and financial institutions, Europe is pushing the reverse direction: greater limitation and oversight.

These trends suggest that stablecoin architectures, regulatory compliance, and jurisdictional design will be battlegrounds in 2025–2026.

7. What This Means for New Crypto Projects & Builders

For individuals or projects exploring next-generation crypto use cases, Europe’s evolving stance presents both risks and opportunities:

- Jurisdictional design matters: Issuing a token that is identical across multiple jurisdictions may draw regulatory scrutiny or prohibitions—especially if reserves or redemptions are managed cross-border.

- Reserve architecture must be transparent, localized, and compliant with regional supervision.

- Token interoperability and liquidity have to reconcile regulatory constraints (e.g. fungibility restrictions).

- Collaboration with regulated institutions (banks, licensed issuers) may become essential to gain access to EU markets.

- Working in tandem with a CBDC regime might open novel infrastructure: e.g. bridging stablecoins to a digital euro, building layered services, or acting as settlement layers within sovereign rails.

- First movers in the euro-denominated stablecoin space (or in Europe-native DeFi rails) may gain advantage if regulation becomes restrictive for outsiders.

Thus, developers should closely monitor European regulatory signals, align issuance strategy accordingly, and consider designing flexible jurisdictional modules.

8. Summary & Outlook

The EU’s push to ban multi-issuance stablecoins marks a strategic effort to defend financial stability and preserve monetary sovereignty. The ESRB recommendation, backed by the ECB, aims to curtail the risks posed by foreign-issued stablecoins operating fungibly across borders. While the recommendation is not legally binding, it exerts strong regulatory pressure and may trigger national-level restrictions.

At the same time, the digital euro project is advancing, offering Europe a sovereign digital payment infrastructure that can counterbalance private stablecoins, particularly those denominated in dollars. In parallel, a consortium of European banks is preparing a MiCA-compliant euro stablecoin to compete on-chain. This dual strategy—limiting foreign stablecoins while building its own—is the EU’s playbook for crypto sovereignty.

For builders, projects, and investors seeking new crypto or blockchain-based income streams, Europe is becoming a regulatory frontier. Designs that cross jurisdictions with shared tokens may soon be untenable. The safe path, for now, is to align issuance architecture with regional rules and consider how to interface with or complement sovereign digital currency rails.

Outlook to watch:

- Whether EU member states adopt the ESRB recommendation into national law (thus making multi-issuance bans legally binding).

- How the European Commission will interpret cross-jurisdiction issuance under MiCA — will it yield to softer stances or align with ECB.

- Progress on the digital euro’s legal framework, design, and pilot implementation.

- The success, governance, and traction of the euro-denominated stablecoin project by the banking consortium.

- How U.S. vs EU regulatory philosophies diverge over stablecoins, and whether global coordination emerges.

In short, Europe is repositioning itself from passive recipient of stablecoin innovations to active regulator and innovator. For those exploring new crypto territory, paying attention to Europe’s rules and rails could be crucial to long-term viability.