Key Takeaways :

- Jamie Dimon openly identifies blockchain-native technologies as a new class of competitors

- JPMorgan Chase is accelerating its blockchain strategy via Kinexys and JPM Coin

- Institutional blockchain infrastructure is targeting $10B daily transaction capacity

- Regulatory clarity around stablecoins is improving, but yield-bearing stablecoins remain controversial

- The expansion of tokenization into private credit and real estate signals a structural shift in finance

- Integration of AI + blockchain is emerging as a core institutional strategy

- Traditional banks are no longer dismissing crypto—they are competing directly with it

Introduction: A Turning Point in Institutional Finance

The global financial system is undergoing one of the most profound transformations since the advent of electronic banking. In a recent annual shareholder letter, Jamie Dimon, CEO of JPMorgan Chase, made a statement that would have seemed unthinkable just a few years ago: blockchain-based technologies—including smart contracts, stablecoins, and tokenization—are now “a completely new set of competitors.”

This acknowledgment marks a decisive shift. For years, Dimon was widely known as one of Wall Street’s most vocal critics of cryptocurrencies, even calling Bitcoin a “fraud” in earlier cycles. Yet today, his tone has evolved. While skepticism toward speculative crypto assets remains, the underlying infrastructure—blockchain—is now seen as a strategic battlefield.

This article explores what this shift means, how JPMorgan is positioning itself, and why this moment could define the next phase of digital finance.

1. Blockchain as a New Competitive Layer

From Disruption to Direct Competition

Dimon’s statement reflects a broader institutional realization: blockchain is no longer a fringe innovation—it is a competing financial infrastructure.

Traditional banking services such as:

- Payments

- Settlement

- Asset management

are increasingly being replicated—or improved—by blockchain-based systems.

The rise of decentralized finance (DeFi), stablecoins, and tokenized assets has created a parallel financial stack that operates:

- Faster (near real-time settlement)

- Cheaper (reduced intermediaries)

- More transparently (on-chain records)

From JPMorgan’s perspective, these are not just innovations—they are existential threats.

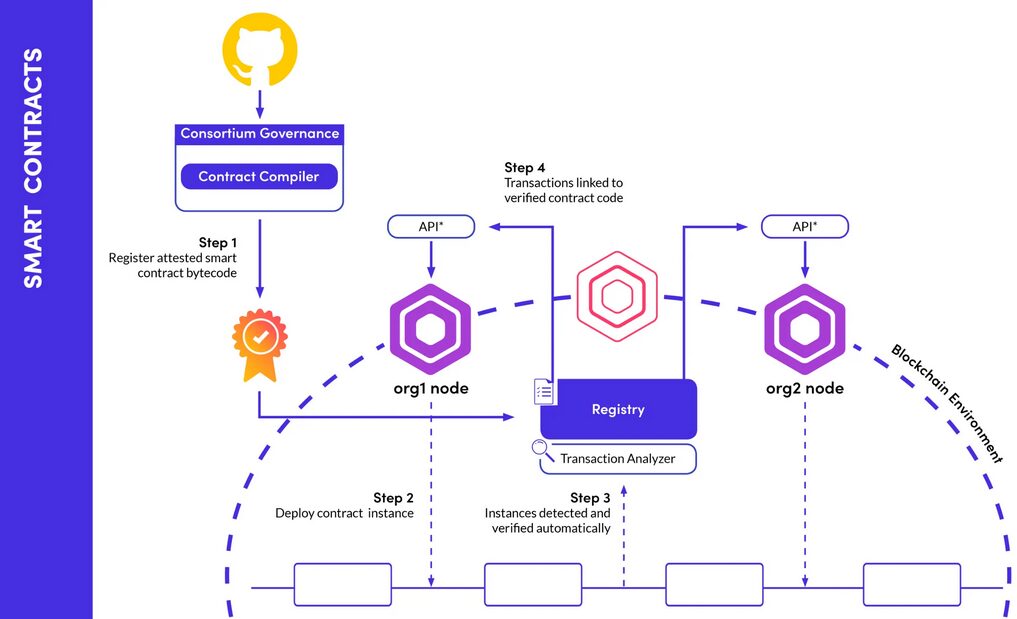

2. JPMorgan’s Counterstrategy: Kinexys and JPM Coin

Building Institutional-Grade Blockchain Infrastructure

To compete, JPMorgan has doubled down on its own blockchain ecosystem.

At the center of this effort is Kinexys, a rebranded evolution of its former Onyx platform.

Kinexys Infrastructure Overview

(Image: Institutional blockchain network architecture, showing banks, asset managers, and tokenized assets connected via smart contracts)

Kinexys aims to process up to $10 billion in daily transaction volume, positioning it as a serious alternative to traditional clearing systems.

Its client roster already includes major global institutions such as:

- BlackRock

- Siemens

- Qatar National Bank

- Mitsubishi Corporation

This signals a critical trend: blockchain adoption is no longer experimental—it is operational.

JPM Coin (JPMD): The Institutional Stablecoin

JPMorgan’s stablecoin, known as JPM Coin (JPMD), represents tokenized bank deposits.

Unlike public stablecoins such as USDC or USDT, JPM Coin operates within a permissioned ecosystem.

It has expanded beyond internal systems and is now deployed on:

- Base (Coinbase-supported network)

- Canton Network

This multi-network expansion highlights a key strategy:

Interoperability between institutional and public blockchain ecosystems

3. Regulation: Opportunity and Constraint

Stablecoin Legislation and Institutional Entry

The regulatory environment is evolving rapidly.

The passage of the GENIUS Act (U.S.) has provided a clearer framework for stablecoin issuance, enabling:

- Institutional participation

- Compliance standards

- Risk controls

However, unresolved issues remain—particularly around yield-bearing stablecoins.

Banks argue that such products:

- Blur the line between deposits and securities

- Could destabilize traditional financial systems

Meanwhile, legislative efforts like the U.S. Clarity Act continue to face political friction, particularly around:

- DeFi regulation

- Ethical provisions

- Market structure definitions

This regulatory uncertainty creates both:

- Barriers (compliance complexity)

- Opportunities (first-mover advantage for compliant players)

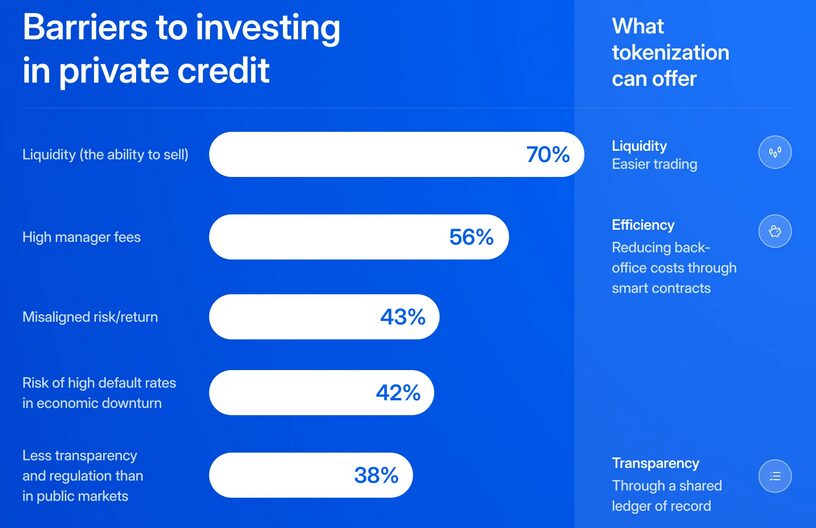

4. Tokenization: The Next Trillion-Dollar Market

Expanding Beyond Payments

JPMorgan is not limiting blockchain to payments.

Its roadmap includes tokenizing:

- Private credit

- Real estate

- Traditional financial instruments

Tokenization Flow

(Image: Real-world asset → tokenization → blockchain trading → settlement)

Tokenization offers:

- Fractional ownership

- Increased liquidity

- Global accessibility

According to multiple industry forecasts, tokenized assets could reach trillions of dollars in value within the next decade.

For readers seeking new revenue streams, this is critical:

Tokenization is not just a technology—it is a new asset class infrastructure.

5. AI + Blockchain: The Dual Engine Strategy

Dimon also emphasized that AI will be embedded “in every process” within JPMorgan.

This signals a convergence of two transformative technologies:

- Blockchain (trust, settlement, ownership)

- AI (decision-making, automation, risk analysis)

Use cases include:

- Automated compliance (AML/KYC)

- Smart contract optimization

- Fraud detection

- Portfolio management

This combination could redefine:

- Operational efficiency

- Risk management

- Customer experience

6. Competitive Landscape: Banks vs. Crypto-Native Players

Who Wins?

The competition is no longer theoretical.

On one side:

- Traditional banks (capital, regulation, trust)

On the other:

- Crypto-native firms (innovation, speed, decentralization)

Dimon remains confident:

“In most cases, we will maintain our leadership position.”

And the numbers support his confidence:

- Revenue: $185.6 billion

- Net income: $57 billion

- 8 consecutive years of record performance

Yet the battlefield is changing.

Crypto firms are:

- Building global payment rails

- Offering yield products

- Tokenizing assets without intermediaries

Banks are:

- Integrating blockchain

- Leveraging regulatory advantages

- Scaling institutional networks

The outcome may not be a winner-takes-all scenario—but a hybrid financial system.

7. Strategic Expansion: Beyond Finance

JPMorgan is also exploring:

- Prediction markets

- Expanded digital finance services

- Broader ecosystem integration

This suggests a long-term vision:

Becoming a platform, not just a bank

Conclusion: The Beginning of a New Financial Architecture

The significance of Dimon’s statement cannot be overstated.

For the first time, one of the world’s most powerful bankers has publicly acknowledged that blockchain is not just a tool—but a competitor.

This marks the transition from:

- Denial → Adoption → Competition

For investors, builders, and institutions, the implications are profound:

- Blockchain is becoming core infrastructure

- Tokenization will reshape asset ownership

- Stablecoins will redefine money movement

- AI will amplify everything

And most importantly:

The next phase of crypto is not rebellion—it is integration.