Main Points :

- Japan’s three megabanks plan to enable stock and bond purchases using stablecoins.

- The framework envisions digital securities settled via trust-based stablecoins.

- The move aims to prevent Japan from lagging behind the U.S. in tokenized MMF development.

- U.S. financial giants such as BlackRock and JPMorgan are already operating tokenized MMFs.

- Regulatory clarity in both Japan and the U.S. is accelerating institutional adoption.

- This shift could redefine how capital flows across borders and between asset classes.

1. Japan’s Strategic Entry into Tokenized Securities

Japan’s financial sector is preparing for a structural transformation. According to reports, Nomura Holdings and Daiwa Securities Group are collaborating with Japan’s three megabanks—Mitsubishi UFJ Bank, Sumitomo Mitsui Banking Corporation, and Mizuho Bank—to build a framework allowing investors to purchase stocks, bonds, investment trusts, and Money Market Funds (MMFs) using stablecoins.

The initiative envisions converting traditional securities into digital securities and settling transactions using stablecoins. The target timeline for practical implementation is within several years.

This move is not merely about convenience. It represents a broader attempt to digitize capital markets infrastructure. By integrating stablecoins into securities settlement, Japan aims to:

- Shorten settlement cycles

- Reduce counterparty risk

- Improve cross-border capital mobility

- Attract global institutional liquidity

The underlying concept is that stablecoins can function as programmable settlement cash—bridging traditional finance and blockchain infrastructure.

2. Why MMFs Are the Core Focus

Money Market Funds (MMFs) are low-risk investment trusts that invest in short-term government securities, high-grade corporate bonds, and certificates of deposit. While not principal-guaranteed, they offer deposit-like stability.

In the United States, tokenized MMFs have seen rapid growth. Japan risks falling behind if it does not modernize its infrastructure.

MMFs are ideal candidates for tokenization because:

- They are short-duration instruments.

- They are widely used for liquidity management.

- They already resemble “cash equivalents.”

- They generate yield.

By tokenizing MMFs and allowing stablecoin settlement, Japan could create yield-bearing blockchain-native financial products that compete globally.

3. Trust-Based Stablecoins: Structural Safety

Japan’s megabanks plan to issue trust-type stablecoins. Under this model:

- The issuer’s assets are segregated from the reserve assets.

- Reserve assets are managed as trust property.

- Asset backing is transparent and bankruptcy-remote.

This design enhances safety and aligns with Japan’s conservative regulatory philosophy.

Previously, the three megabanks announced joint experiments to issue yen-denominated stablecoins, supported by Japan’s Financial Services Agency under its FinTech Proof-of-Concept Hub.

The long-term objective includes cross-border payment optimization. Stablecoins are not just domestic settlement tools—they are programmable international liquidity rails.

4. The U.S. Leads: Tokenized MMFs in Practice

While Japan prepares, the U.S. has already operationalized tokenized MMFs.

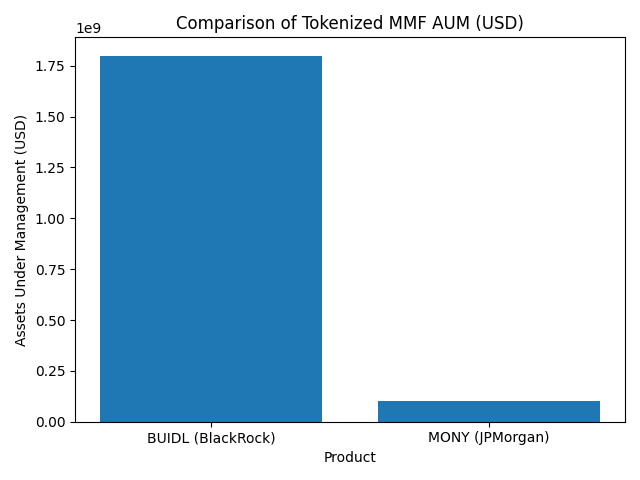

BlackRock’s BUIDL

BlackRock launched its tokenized MMF, BUIDL, in 2024. It is backed by U.S. Treasuries and allows investors to earn yield in USD terms.

- Assets under management: approximately $1.8 billion.

- Issued on Ethereum and BNB Chain.

- Purchasable using USD or USDC.

- Redeemable for USD or USDC.

This hybrid structure allows both traditional and crypto-native investors to participate.

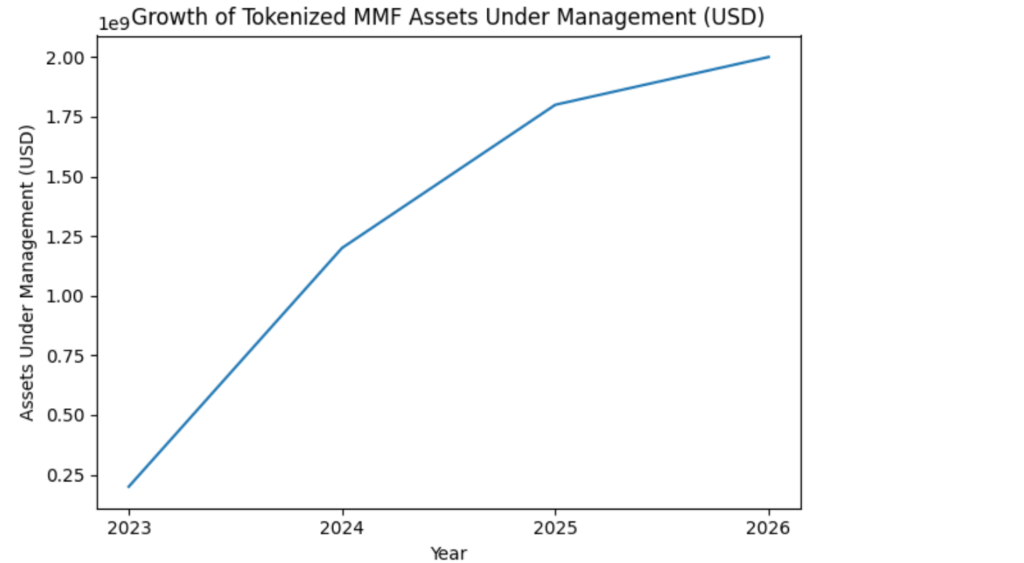

[Tokenized MMF Growth]

The rapid increase in tokenized MMF assets demonstrates institutional appetite.

JPMorgan’s MONY

In December, JPMorgan launched MONY, another tokenized MMF issued on Ethereum.

- Backed by U.S. Treasuries and repo transactions.

- Restricted to qualified investors.

- Purchasable and redeemable in USD and select stablecoins.

- Assets under management: approximately $100 million.

[BUIDL vs MONY Comparison]

JPMorgan executives have stated that tokenization fundamentally changes transaction speed and operational efficiency. Other global banks are expected to follow.

Franklin Templeton’s Adjustments

Franklin Templeton has also updated institutional MMFs to align with regulatory reserve requirements under the U.S. stablecoin regulatory framework known as the GENIUS Act.

The U.S. passed comprehensive stablecoin legislation in July last year, providing clarity for issuers and reserve requirements. Regulatory certainty has catalyzed innovation.

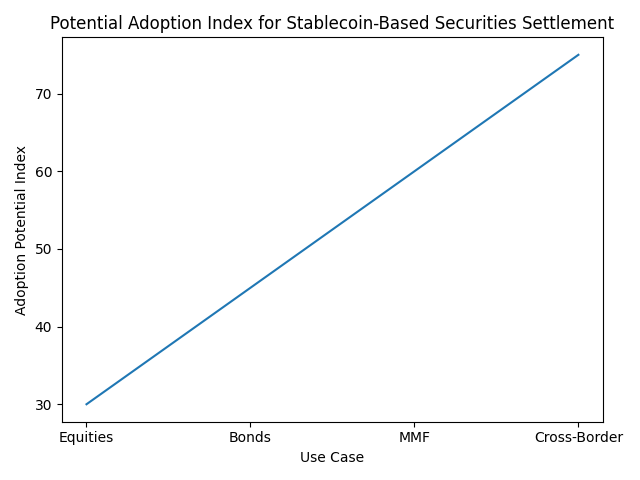

5. The Bigger Picture: Settlement as Infrastructure

Stablecoin-based securities settlement changes the architecture of finance.

Traditional securities settlement relies on:

- Central clearinghouses

- T+2 or T+1 cycles

- Banking intermediaries

Tokenized settlement can enable:

- Near-instant settlement

- Atomic delivery-versus-payment

- Reduced reconciliation costs

- Cross-chain interoperability

[Adoption Index]

This infrastructure-level change may be more significant than crypto speculation cycles.

6. Implications for Investors Seeking Yield and Opportunity

For readers searching for new crypto assets or next-generation revenue streams, tokenized MMFs represent a bridge between DeFi and TradFi.

Potential implications:

- Yield-bearing on-chain instruments backed by sovereign debt.

- Stablecoin reserve integrations.

- Collateral for decentralized lending protocols.

- Institutional-grade liquidity on public blockchains.

- Reduced FX friction in cross-border investment.

If Japan integrates stablecoin settlement into equities and bonds, secondary markets could eventually migrate to blockchain rails.

7. Cross-Border Capital Flow Acceleratio

One of the most powerful implications is cross-border efficiency.

Imagine:

- Japanese digital bonds purchasable via USD-backed stablecoins.

- U.S. tokenized Treasuries purchasable via yen stablecoins.

- Real-time settlement across jurisdictions.

Such interoperability could:

- Compress FX spreads.

- Reduce correspondent banking layers.

- Enable 24/7 capital markets.

This is not speculative. Institutional pilots are already occurring.

8. Competitive Dynamics: Japan vs U.S.

The U.S. currently leads in:

- Institutional tokenization

- Stablecoin regulatory clarity

- Blockchain liquidity depth

Japan’s strength lies in:

- Regulatory discipline

- Banking stability

- Corporate partnerships

If Japan executes effectively, it may leapfrog by integrating stablecoins directly into mainstream securities markets rather than isolating them in crypto-native silos.

9. Risks and Structural Considerations

However, challenges remain:

- Regulatory harmonization across jurisdictions.

- Custody frameworks.

- Smart contract risk.

- Liquidity fragmentation.

- Cybersecurity concerns.

Trust-based stablecoins mitigate issuer risk, but blockchain infrastructure risk remains.

10. The Long-Term Vision

The convergence of:

- Tokenized MMFs

- Trust-based stablecoins

- Digital securities

- Cross-border programmable liquidity

signals the emergence of a new capital market layer.

Instead of crypto replacing traditional finance, what is unfolding is integration.

The next phase of financial innovation will not be driven by meme tokens—but by infrastructure tokens, yield instruments, and programmable sovereign liquidity.

Conclusion

Japan’s three megabanks moving toward stablecoin-based securities settlement marks more than a technological experiment. It is a strategic repositioning in global capital markets.

The U.S. has demonstrated institutional appetite for tokenized MMFs. Regulatory clarity has accelerated adoption. Now Japan is responding with a trust-based, security-oriented framework that may integrate stablecoins directly into mainstream financial instruments.

For investors seeking new crypto-native revenue sources, the most promising opportunities may lie not in speculative altcoins—but in the tokenization of traditional assets.

Stablecoins are evolving from payment tools into settlement infrastructure. MMFs are evolving from cash substitutes into blockchain-native yield instruments. Securities are evolving into programmable digital assets.

The financial system is not being disrupted. It is being rewritten—quietly, institutionally, and structurally.

Those who understand this transition early may be best positioned for the next wave of value creation.