Main Points :

1. Japan Enters the “Year One” of Domestic Stablecoins

2. Mega-Banks Move Toward Joint Stablecoin Issuance

3. Trade Finance and Securities Settlement as Core Use Cases

4. Government to Establish a Dedicated Digital Financial Assets Bureau

5. Japan’s Strategic Position in the Global Stablecoin Race

1. Japan Enters the “Year One” of Domestic Stablecoins

At the MoneyX 2026 conference, Finance Minister Satsuki Katayama declared Japan’s intention to accelerate the “social implementation” of stablecoins and tokenized deposits. Her remarks signal a shift from regulatory experimentation to practical, economy-wide deployment.

MoneyX 2026, themed around “The New Era of Currency Opened by Official Stablecoin Authorization,” gathered financial institutions, startups, regulators, and investors. Organized by the WebX Executive Committee with participation from JPYC, Progmat, SBI Holdings, and CoinPost, the event reflects Japan’s coordinated industry push toward compliant digital currency infrastructure.

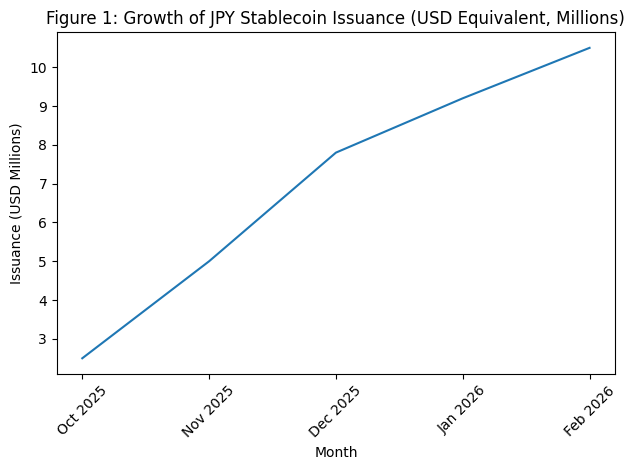

Japan’s regulatory groundwork—established ahead of many major economies—has already enabled the issuance of yen-denominated stablecoins. In October last year, the country saw the launch of its first domestically issued JPY stablecoin. Within roughly three months, cumulative issuance surpassed ¥1 billion, equivalent to approximately $10.5 million.

This rapid uptake marks what many industry observers now call Japan’s “Stablecoin Year One.”

[Growth of JPY Stablecoin Issuance]

The chart above illustrates the steady increase in issuance (USD equivalent). Although modest compared to global giants like USDT or USDC, Japan’s growth is policy-driven and institutionally anchored—qualities that often matter more than raw scale in early-stage infrastructure.

Unlike algorithmic experiments of previous crypto cycles, Japan’s framework mandates clear backing, licensed issuers, and regulated custodial structures. This significantly reduces systemic risk and enhances institutional participation.

2. Mega-Banks Move Toward Joint Stablecoin Issuance

In November, Japan’s three mega-banks announced proof-of-concept initiatives aimed at jointly issuing stablecoins. This development is critical: it represents traditional finance not resisting but actively integrating blockchain-based money.

The distinction between “stablecoins” and “tokenized deposits” is subtle yet important. Stablecoins may circulate on public blockchains, while tokenized deposits typically remain within permissioned banking environments. Both, however, digitize fiat liabilities into programmable form.

Tokenized deposits are already being explored for regional currency applications. Some financial institutions are preparing issuance frameworks that connect local economic ecosystems to blockchain rails. This reflects a broader global trend:

- In the United States, major asset managers are integrating tokenized treasuries.

- In Europe, MiCA regulations are shaping compliant euro stablecoins.

- In Asia, Singapore and Hong Kong are piloting wholesale CBDC-like infrastructures.

Japan’s advantage lies in clarity. Rather than debating definitions, regulators provided legal certainty early.

3. Trade Finance and Securities Settlement as Core Use Cases

Minister Katayama emphasized that stablecoins are not merely faster remittance tools. Their transformative potential lies in synchronizing payment, logistics, and asset transfer.

Trade Finance

Traditional international transfers rely on SWIFT messaging and correspondent banking networks. These processes are slow and costly. Stablecoins eliminate intermediary layering.

More importantly, blockchain-based trade finance enables smart contract integration. Cargo shipment data, customs documentation, and payment settlement can become synchronized events.

For example:

- Shipment leaves port

- Customs verification completed

- Smart contract triggers stablecoin payment automatically

This reduces reconciliation delays and counterparty risk.

Securities Settlement

The Financial Services Agency (FSA) is supporting pilot programs where government bonds, corporate bonds, and equities are recorded on blockchain infrastructure. Settlement occurs via stablecoins.

This could compress settlement cycles from T+2 to near real-time.

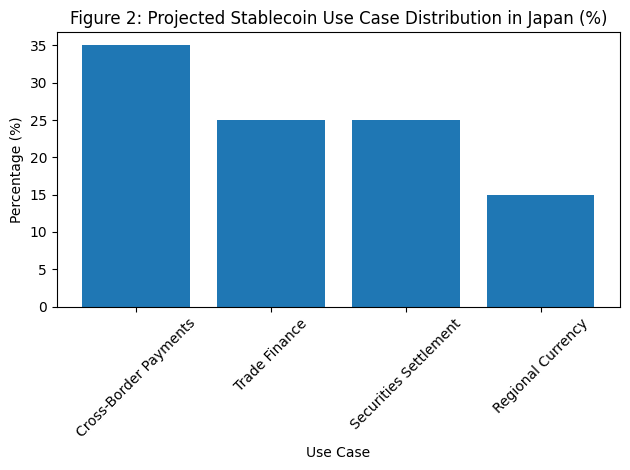

[Stablecoin Use Case Distribution]

The chart above shows projected allocation across use cases. Cross-border payments remain dominant, but trade finance and securities settlement represent high-value institutional flows.

If implemented effectively, these sectors could unlock billions in efficiency gains annually.

4. Establishment of a Dedicated Digital Financial Assets Bureau

A major policy announcement at MoneyX 2026 was the planned establishment of a specialized bureau within the Financial Services Agency by summer.

This bureau will exclusively oversee:

- Digital financial assets

- Stablecoin frameworks

- Tokenized deposits

- Regulatory sandbox expansion

Institutionalizing oversight reduces regulatory ambiguity and increases foreign investment confidence.

The government also encourages firms to leverage the FSA’s Payment Platform support framework for legal interpretation assistance during pilot experiments.

Such proactive regulator engagement contrasts with jurisdictions where innovation faces reactive enforcement.

5. Japan’s Strategic Position in the Global Stablecoin Race

Globally, stablecoins already represent over $130 billion in circulation (primarily USD-based). Their use in decentralized finance, cross-border settlement, and treasury management is expanding rapidly.

Japan’s opportunity is not to compete in USD dominance—but to:

- Strengthen JPY’s digital presence

- Reinforce domestic banking innovation

- Export compliant financial infrastructure

The geopolitical dimension is also notable. Minister Katayama previously mentioned potential Japan–US cooperation on stablecoin standards. As the U.S. considers federal stablecoin legislation, interoperability standards could shape global digital currency markets.

For investors seeking new crypto assets, the focus may shift toward:

- Infrastructure tokens enabling regulated settlement

- Blockchain middleware for financial institutions

- Compliance-layer Web3 startups

- Tokenized real-world asset platforms

Stablecoins themselves may not generate speculative upside—but the ecosystems around them likely will.

6. Implications for Revenue and Practical Blockchain Deployment

For entrepreneurs and investors, three strategic themes emerge:

A. Infrastructure Monetization

Custody, compliance APIs, identity verification, on-chain audit tools.

B. Institutional Middleware

Bridging core banking systems with blockchain networks.

C. Real-World Asset Tokenization

Government bonds, corporate bonds, trade receivables.

The “social implementation” phase means revenue now shifts from token price volatility toward transaction throughput and financial service margins.

This is where blockchain becomes invisible infrastructure rather than speculative narrative.

Conclusion

MoneyX 2026 marked a decisive transition in Japan’s digital asset strategy. The country has moved beyond theoretical regulation into applied financial architecture.

By combining:

- Legal clarity

- Mega-bank participation

- Government-backed pilot programs

- Institutional oversight expansion

Japan is positioning itself as a leader in compliant digital currency markets.

The next phase will test scalability, interoperability, and international alignment. If successful, Japan’s model may serve as a blueprint for how advanced economies integrate blockchain into the core of financial systems—quietly, structurally, and sustainably.

Stablecoins are no longer just crypto instruments. In Japan, they are becoming financial infrastructure.