Main Points :

- Japan’s financial regulator, the Financial Services Agency (FSA), has launched the “Payment Innovation Project (PIP)” to support blockchain‐based payment experiments.

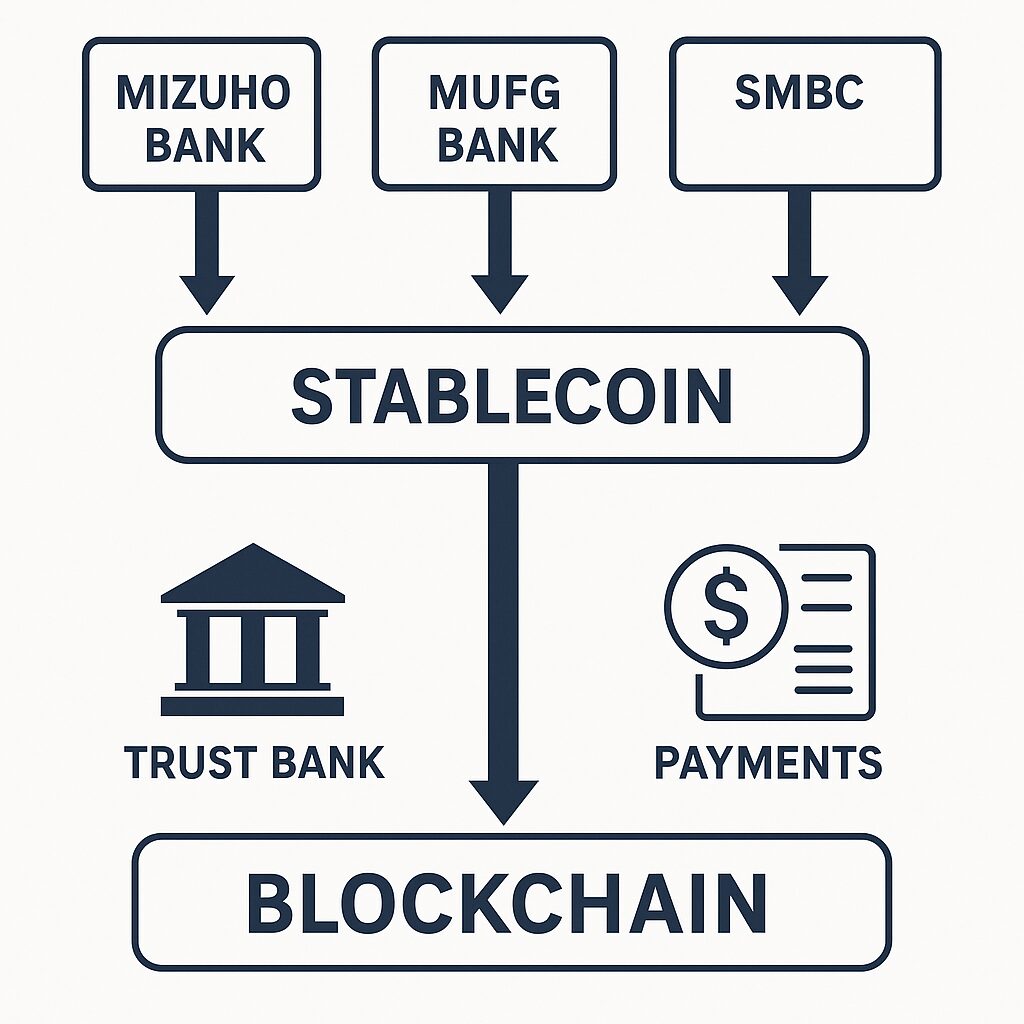

- The three major Japanese banks—Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Financial Group (SMFG) and Mizuho Financial Group—will jointly issue a stablecoin, exploring both yen- and US-dollar-pegged versions.

- The stablecoin will be issued under a trust structure via Mitsubishi UFJ Trust and Banking Corporation and supported by infrastructure from fintech firm Progmat Inc..

- The project exempts the conventional ¥1 million (≈ US$6,600) transfer limit that applies under existing second-class fund transfer instruments in Japan.

- The objective is to create unified standards across banks to avoid fragmentation of stablecoin issuance, streamline corporate and cross-border settlement, and position Japan as a leader in regulated digital finance.

- For crypto investors and blockchain practitioners, this shift highlights stablecoins’ evolving role from retail speculation to institutional infrastructure, and opens up new potential use-cases for tokenised liquidity, corporate treasury, and cross-border settlement.

1. Regulator Launches the “Payment Innovation Project (PIP)”

On November 7, 2025, the FSA announced the creation of its new initiative called the “Payment Innovation Project (PIP)”, focused on advancing next-generation payments using blockchain. This initiative will serve as the first venue under the FSA’s FinTech proof-of-concept hub to examine regulated experiments around payments, digital coins and tokenisation.

In this context, the PIP’s very first supported project is the joint stablecoin issuance by Japan’s three major banking groups. This signals a policy shift: the regulator is not merely observing crypto experiments, but actively enabling them, provided they comply with legal and operational standards.

From a blockchain perspective, this is significant: one of the world’s major banking markets is embracing tokenised payment rails and exploring stablecoins beyond retail speculation. For developers, infrastructure providers and investors, this opens a new frontier: regulated stablecoins backed by banks with corporate settlement use-cases.

The launch of PIP also reflects Japan’s broader aim to modernise its payments infrastructure, improve cross-border settlement efficiency, reduce reliance on legacy rails, and maintain competitiveness in Asia amidst rising fintech initiatives in places like Singapore, South Korea and China.

2. The Three Megabanks’ Joint Stablecoin Initiative

The initiative involves MUFG, SMFG and Mizuho joining forces to issue stablecoins under a unified standard. According to reports, the stablecoins will be pegged first to the Japanese yen (JPY), with future potential for a US-dollar (USD) pegged version.

Why jointly issue? One of the key motivations is to avoid fragmentation: if each bank issued its own token independently, the result would be multiple standards, interoperability issues and higher integration cost for corporate clients. By issuing under a single brand/standard, the banks hope to accelerate adoption.

Technically, the stablecoin issuance is structured as a trust-type tokenisation via Mitsubishi UFJ Trust and Banking, and infrastructure partner Progmat will provide the blockchain engine. The transfer-limit exemption is noteworthy: the funding instrument will not be subject to the ¥1 million (~US$6,600) transfer ceiling applicable to “second class” electronic payment instruments under Japanese law. This gives more flexibility for larger corporate transactions.

For practitioners and investors, this initiative means that stablecoins are being built not for retail day-to-day purchases, but for corporate treasury, cross-border, internal group settlements, global trading houses and inter-bank flows. One major trading firm (Mitsubishi Corporation) is set to be the first user via its 240+ global subsidiaries.

3. Implications for the Crypto/Blockchain Ecosystem

a) Stablecoins as Infrastructure, Not Just Speculation

The move by Japan’s top banks repositions familiar stablecoin narratives. Instead of purely retail speculation (hedge against volatility, yield farming), we are seeing stablecoins become institutional rails—digital representations of fiat used for settlement, intra-company transfer, cross-border, B2B flows. For crypto investors seeking new assets or tokenisation themes, this means stablecoins will have dual roles: as bridges between fiat and crypto, and as building blocks for programmable money.

b) Tokenisation & Programmability of Fiat

With bank-backed stablecoins, programmable payments (smart contracts, automated settlement, global supply-chain payments) become more credible. For example: a corporate group receives USD-pegged tokens, triggers automatic conversion/settlement, pays suppliers in multiple jurisdictions, all via blockchain. This is consistent with the user’s interest in “blockchain’s practical use” and new income streams.

c) Competitive Positioning & Currency Diversification

Globally, US-dollar-pegged stablecoins dominate (>99% of supply) according to the Bank for International Settlements. The Japanese initiative signals a move toward more currency-diverse stablecoins (yen, dollar, other FX). For crypto investors, this could mean new stablecoin assets, or underlying tokenised liquidity pools in different currency regions. For wallet developers (such as the user’s interest in swaps between BTC and ETH), this could mean stablecoin bridges to yen or other fiat-pegged tokens.

d) Regulatory Clarity & Institutional Confidence

The FSA’s active approval of the project reduces regulatory uncertainty. For projects in the Philippines or cross-border, this is a positive signal: regulated stablecoins backed by banks are becoming possible. This influences how VASPs, EMIs and wallets structure partnerships, custody, AML/CTF controls, and jurisdictional settlement flows.

4. Recent Developments & Broader Trends

The first licensed yen-pegged stablecoin: JPYC

Apart from the bank project, Japanese startup JPYC Inc. launched the first fully licensed yen–pegged stablecoin, JPYC. Each token is pegged 1:1 to the yen and backed by bank deposits and Japanese Government Bonds (JGBs). The company targets issuance of up to ¥10 trillion (≈ US$66 billion) over three years, initially zero transaction fees to drive adoption, and support for major chains like Ethereum, Avalanche and Polygon.

This illustrates that multiple players (banks + fintech) are moving in parallel in Japan’s stablecoin ecosystem.

Slow Retail Adoption But Growing B2B Focus

While Japan remains a cash-heavy economy (cash still accounts for more than half of transactions), the adoption of stablecoins for everyday retail is expected to be gradual. Experts note the real value currently lies in corporate, settlement and cross-border flows.

Global Competitive Landscape

Japan’s stablecoin push comes as other jurisdictions accelerate: the U.S. has codified stablecoin rules, the EU is discussing digital euro or euro-stablecoin, South Korea and China are exploring won/yen/yuan-based digital tokens. For crypto investors, this means stablecoins will increasingly be part of the digital-asset infrastructure landscape, not just tokens for yield farming.

5. Practical Insights for Crypto Asset Hunters & Blockchain Practitioners

For Investors Seeking New Assets and Income Streams

- Monitor stablecoins beyond USDT/USDC: the yen-stablecoin space (e.g., JPYC) and bank-issued tokens offer new markets.

- Consider tokenised liquidity pools that may include yen- or USD-pegged tokens, especially in Asia-Pacific corridors.

- Understand that stablecoins backed by banks may carry lower volatility risk and higher reliability—but also may deliver lower yield (since they are infrastructure, not speculative yield farms).

For Blockchain Developers & Non-custodial Wallet Builders

- If you are building a wallet (e.g., “dzilla Wallet”) with BTC-to-ETH swap features, consider integrating stablecoins as routing rails (e.g., BTC → yen-stablecoin → ETH) for on-ramp/off-ramp flexibility.

- The regulatory wrap in Japan suggests institutional banks/trusts may serve as anchor issuers—so partnering with licensed entities may be required for real-world rails.

- Programmability matters: smart contracts triggering settlement, trust-type issuance, multi-chain support—all need to be architected accordingly.

For Remittance/EMI/VASP Frameworks in the Philippines (and beyond)

- The Japanese model shows how banks/trusts issue tokens and regulator approves under specific frameworks. In the Philippines, your EMI/VASP audit frameworks and suspicious transaction monitoring may require similar considerations: token origination, reserve backing, cross-border flows, AML/CFT.

- For token issuers: trust structure, auditing of reserves, redemption mechanisms (1:1 peg), transfer limit exemptions—all are governance features you should benchmark.

6. Risks and Considerations

- Although institutional traction is high, retail adoption remains uncertain: Japan’s cash culture slows uptake.

- Regulatory and compliance demands may intensify: stablecoins could trigger systemic-risk concerns, especially if they scale. The FSA will publish results of the pilot including compliance/monitoring issues.

- Tokenised stablecoins rely on underlying infrastructure (blockchain networks, smart contract security), so technological and custody risks persist.

- Interoperability matters: if banks issue tokens under different standards (even within Japan), fragmentation risk remains. The joint bank issuance aims to mitigate this but global compatibility is still a work in progress.

Conclusion

The joint stablecoin initiative by Japan’s top banks under the FSA’s Payment Innovation Project marks a watershed moment in the evolution of crypto and blockchain infrastructure. For asset hunters, it signals that stablecoins are no longer just speculative vehicles—they are becoming infrastructure rails for corporate settlement, cross-border payments, and tokenised liquidity. For blockchain practitioners, especially wallet developers and VASP/EMI frameworks, the lesson is clear: build with regulatory-compliant rails, integrate tokenised fiat, plan for multi-chain support, and enable programmability. For those focused on developing markets like the Philippines, this is a blueprint: trusted institutions issuing backed tokens, governed by regulator, with practical use-cases in settlement and remittance. As the stablecoin ecosystem institutionalises, the opportunities for new assets, new settlement mechanisms, and new business models increase. Staying ahead means moving from “which coin will pump” to “which tokenised infrastructure will power the next wave of payments and finance.”