Main Points :

- The Japanese FSA is proposing to shift crypto asset regulation from the Payment Services Act (PSA) to the stricter Financial Instruments and Exchange Act (FIEA), consolidating oversight and avoiding regulatory duplication.

- Crypto assets lack traditional securities characteristics (rights, revenue distribution), prompting a proposal for a separate regulatory category under the FIEA.

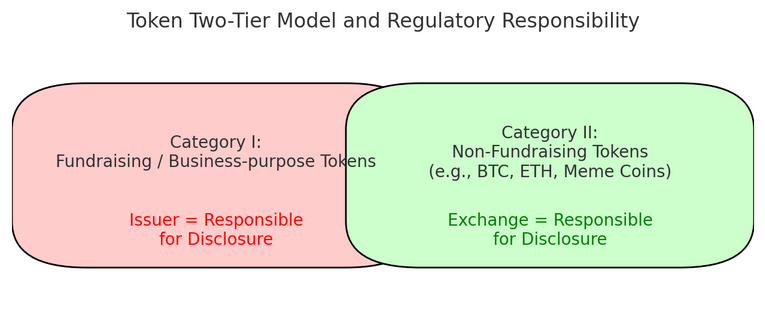

- The FSA is considering a two-tier classification: “fundraising/business-purpose” tokens vs. “non-fundraising” tokens (e.g., BTC, ETH), with differing disclosure and oversight duties.

- Concerns have been raised by experts—especially regarding IEOs, many of which lost over 90% of their value—about bringing such high-risk offerings under investor-protection frameworks like FIEA.

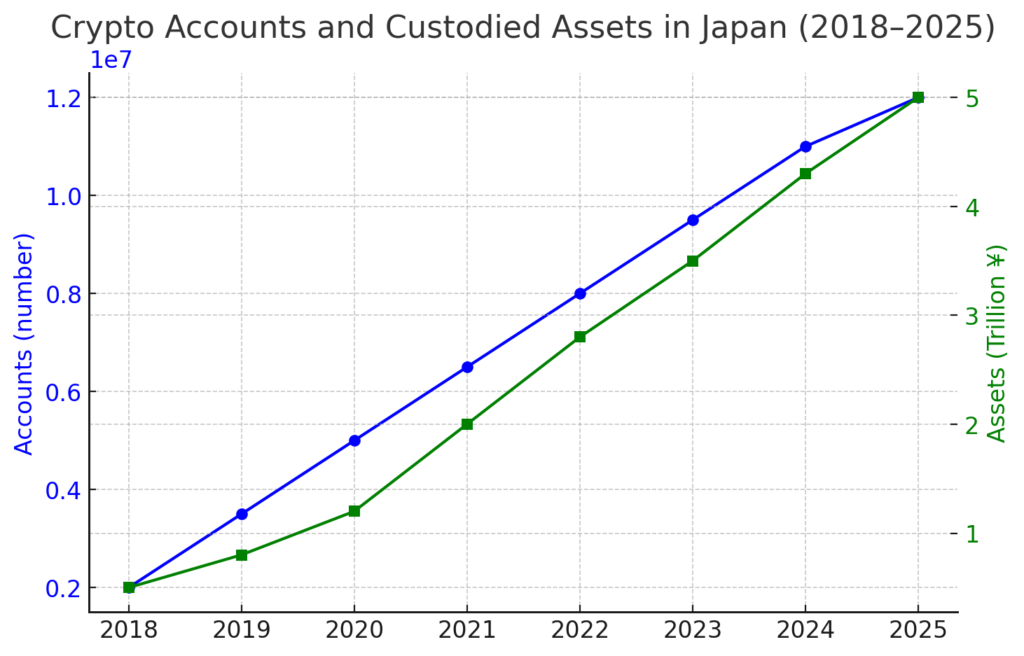

- The FSA’s drive stems from increasing retail participation (over 12 million accounts), small-scale investors, and rising fraud complaints, underscoring the need for stronger protection.

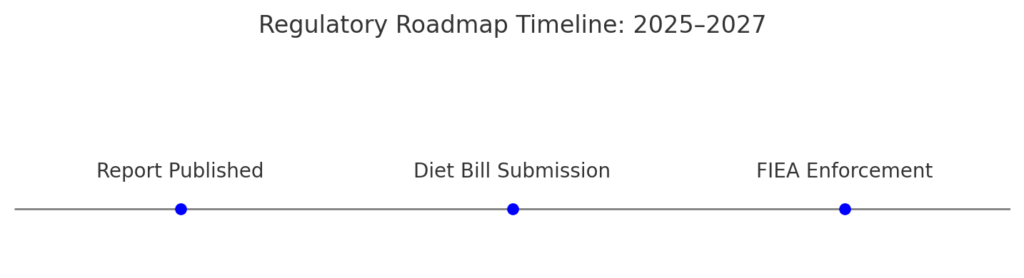

- Legislatively, the roadmap targets a 2025 report, House submission in 2026, and implementation in 2027.

- Global trends—like spot Bitcoin ETFs in the US, better market manipulation regulation in Europe—also motivate Japan’s recalibration.

- The proposal includes enhanced obligations for exchanges, possibly aligning them with Type I securities firms while avoiding full securities exchange licensing.

- The shift aims to bolster transparency and legitimacy, balancing innovation with retail investor safety.

1. Background — Why Japan Is Reassessing Crypto Regulation

In the second meeting of the Financial System Council’s working group on crypto asset regulation, held on September 2, 2025, Japan’s Financial Services Agency (FSA) revisited how cryptocurrencies are governed. As crypto increasingly serves as an investment vehicle, not merely a payment medium, the FSA proposed transitioning oversight from the Payment Services Act (PSA) to the more robust Financial Instruments and Exchange Act (FIEA).

Under the current regime, regulated under the PSA, crypto exchanges must register with the FSA and adhere to basic consumer protections like segregated custody. However, as investor usage rose—now exceeding 12 million accounts and approximately ¥5 trillion (~$34 billion) in assets—the vulnerabilities of the system became exposed. Many retail users are small-scale (80% holding under ¥100,000), and concerns including illicit solicitation and withdrawals populating dispute channels further underline risk.

2. Why the FSA Advocates a Singular FIEA Framework

The FSA argues dual regulation under both PSA and FIEA would complicate compliance and unnecessarily burden industry participants. Instead, it recommends crypto assets be regulated exclusively under the FIEA. Though FIEA covers instruments possessing rights or revenue-sharing features, crypto lacks these traits, prompting the FSA to propose treating them as a distinct regulatory category within the FIEA rather than as traditional securities.

3. Token Classification: Two Tiers, Tailored Regulation

The FSA outlines a nuanced two-tier model:

- Category I: “Fundraising / Business-Purpose” tokens—those issued to fund projects or enterprise activities. Issuers would face strict disclosure and accountability requirements.

- Category II: “Non-Fundraising” tokens—such as Bitcoin, Ethereum, or meme coins, which lack centralized issuance or fundraising intent. Exchanges, not issuers, would assume informational duties due to the absence of an entity to regulate.

This tiered approach allows differentiated regulation based on token purpose, with oversight mechanisms tailored to unique token dynamics, including the possibility of categorization shifts due to decentralized governance developments.

4. Expert Caveats: IEO Pitfalls and Retail Investor Vulnerability

During the WG meeting, members heard from Prof. Naoyuki Iwashita (Kyoto University), who warned of the “unthinkable” implications of treating IEOs as suitable for FIEA public investment, citing numerous domestic IEOs that plummeted more than 90%—rendering many tokens virtually worthless. His caution reinforces the need for rigorous scrutiny before folding high-risk crypto into formal securities regulatory frameworks.

5. Investor Protection, Fraud Prevention, and Regulatory Strengthening

WG members reinforced the critical need for transparent information disclosure and protections against fraudulent solicitation, given the rise of predatory practices via social media and messaging platforms. The FSA aims to enhance investor confidence through stricter enforcement of standards that go beyond PSA mandates—such as advertising control, best-execution obligation, fund segregation, internal governance, and cyber security—often borrowed from FIEA’s regulatory toolbox.

6. Exchange Regulation: Harder than PSA, Softer than Securities Exchanges

Another major proposal is stronger oversight of crypto exchanges. Reflecting their growing market role and co-existing derivatives operations, exchanges might be regulated similar to Type I FIEA firms. However, strict licensing for exchange operators—akin to securities exchanges—may be deferred, since many have limited price formation capacity. Meanwhile, listing by traditional securities exchanges remains cautious due to cyber-threat risks.

7. Policy Timeline: From Report to Enforcement (2025–2027)

The FSA envisions finalizing a report in 2025, submitting legislative amendments during the 2026 ordinary Diet session, and politically targeting FIEA-based enforcement of crypto regulation starting in 2027. This timeline reflects both ambition and pragmatism, balancing drafting, discussion, and phased rollout.

8. Global Trends Informing Japan’s Approach

International developments are influential: the U.S. has seen spot Bitcoin ETFs become reality, and Europe is intensifying anti–market-manipulation and insider trading rules. These dynamics incentivize Japan to align with global best practices that recognize crypto’s dual nature—as technology and investment—while fostering legitimacy.

9. Implications for Practitioners, Investors, and Projects

- Investors: Enhanced protection through stricter disclosures and fraud controls should increase confidence.

- Exchanges: They’ll face elevated compliance requirements, possibly prompting internal restructuring or new licensing strategy.

- Issuers: Need to align transparency and governance with FIEA demands, especially for fundraising tokens.

- Blockchains & DeFi: The non-fundraising tier may afford some flexibility, but future shifts in decentralization or governance could affect classification.

10. Summary & Outlook

Japan appears to be on the verge of a regulatory transformation that aims to integrate crypto assets into a mature, investor-protection-oriented securities law, while maintaining their unique treatment. The FSA’s proposals reflect a clear intent: protect retail investors, reduce regulatory complexity, and adapt rules proportionally across token types. The 2027 enforcement target signals Japan’s commitment to robust, forward-looking crypto regulation, blending transparency, innovation, and global alignment.