Key Points :

- Italian banks, led by the Italian Banking Association (ABI), have expressed support for the Euro-area central bank digital currency (CBDC) initiative, the Digital Euro, but are urging that the associated costs for banks be spread over several years due to high implementation investment.

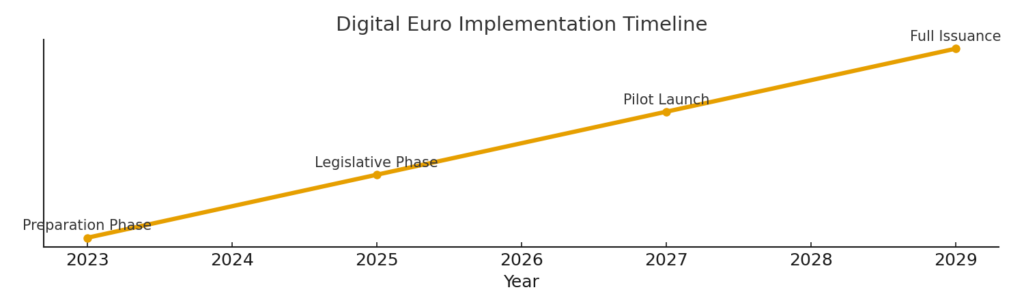

- The European Central Bank (ECB) has moved its digital euro project from the initial “preparation phase” into the next phase, targeting a pilot launch around mid-2027 and a full issuance by 2029, subject to legislation.

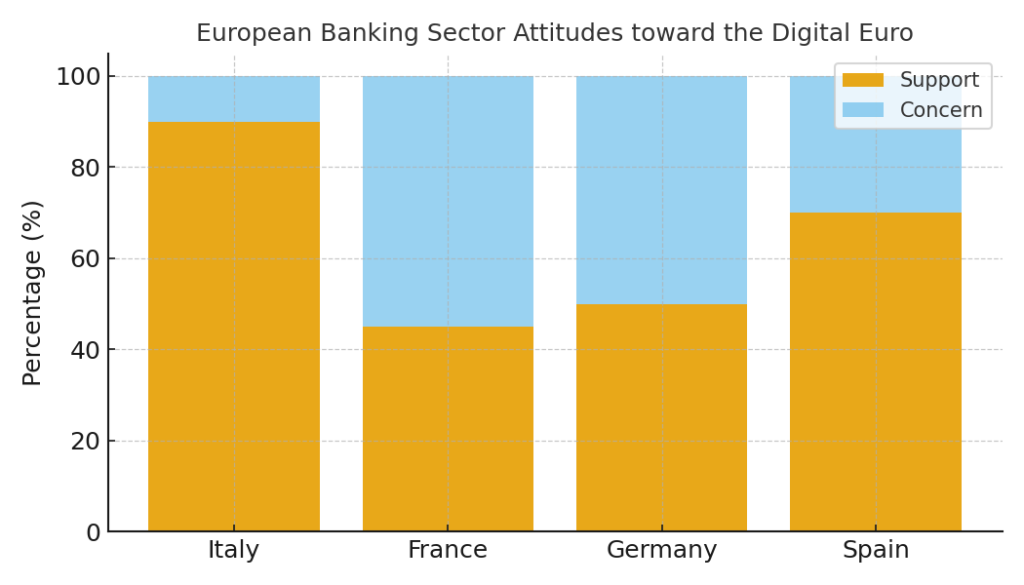

- While some banks in France and Germany have reservations — particularly around deposit migration away from commercial banks to an ECB-wallet — Italy is positioning itself more proactively, proposing a “twin-track” approach where a central bank digital currency co-exists with commercial bank digital currencies (CBDCs).

- For blockchain and crypto asset investors, the digital euro initiative represents both a potential structural shift in how payments and digital money are handled in Europe and an opportunity to monitor adjacent innovation (e.g., stablecoins, tokenised central bank money, infrastructure layers) that may impact the digital-asset ecosystem.

- The rollout of the digital euro raises several practical considerations: how banks will integrate the infrastructure, how the commercial-bank ecosystem adapts, regulatory design (holding limits, offline capability, privacy), and what this may mean for tokenised assets or digital-asset rails that may piggy-back on or compete with CBDC infrastructure.

1. Background: Why the Digital Euro Matters

The digital euro project is being advanced by the ECB and the Eurosystem as a response to changing payment habits, the decline in cash usage, and concerns about reliance on non-European payment infrastructures (for example, global card networks or overseas stablecoin issuers).

The concept is that a digital euro would complement (not replace) cash, offering a publicly-issued digital means of payment with legal tender status, central bank backing, and comparable reliability and security to banknotes. From the perspective of monetary sovereignty, Europe wants to ensure that the public retains access to central-bank money even as the economy digitises.

For the crypto and blockchain community, the relevance is two-fold:

- On the one hand, CBDCs may reduce friction in payments, support new rails, and open up tokenised-money infrastructure which blockchain practitioners can leverage.

- On the other hand, they may shift regulatory and competitive dynamics in how digital money and private tokens coexist with public money.

2. Italy’s Stance: Support with Conditions

Italian Banks’ Support

The Italian Banking Association (ABI) has publicly affirmed support for the digital euro initiative, describing it as enhancing Europe’s “digital sovereignty”. ABI’s managing director Marco Elio Rottigni emphasised that the concept of a CBDC is aligned with the notion of Europe retaining control of its monetary infrastructure.

But: High Costs and Implementation Risks

However, ABI also stressed a key caveat: the cost burden on banks is substantial, and therefore they require a gradual cost-rollout over multiple years rather than a front-loaded investment. The banks warned that forcing heavy initial expenditures may impact profitability and bank viability.

Twin-Track Proposal

The Italian position includes advocating for a “twin‐track” approach: while the digital euro is developed by the central bank, commercial banks could also issue their own digital currencies (CBDC-like instruments) in parallel. This would allow commercial innovation to continue while also securing the central-bank anchor.

Competitive Concerns and Deposit Migration

In contrast, banks in France and Germany have voiced concerns that a retail digital euro could lead to deposit outflows from commercial banks into ECB wallets, weakening banks’ credit-intermediation role. Italian banks appear more willing to support the project, perhaps seeing long-term strategic benefit in gearing infrastructure accordingly, subject to manageable cost profiles.

3. Timeline & Technical Readiness

Current Phase

The ECB confirmed that the digital euro has moved into its next phase as of late October 2025 (post the two-year preparation phase). The work now focuses on three streams:

- Technical readiness (core infrastructure, offline payments, pilot systems)

- Market engagement (payment providers, merchants, consumers)

- Legislative process support (co-working with EU legislators)

Pilot and Issuance Forecast

The projected timeline is approximately:

- Pilot exercise: mid-2027 (initial transactions)

- Full issuance: 2029 (subject to legislation and final decision)

Segmented Cost Roll-Out

According to ECB documents, the implementation will be modular and cost commitments will be staged so as to limit large upfront burdens.

4. Implications for Crypto-Assets and Blockchain Practitioners

Payment Rail Innovation

The advent of a digital euro is potentially transformative: it could drive new rails for tokenised money, encourage interoperability, and reduce reliance on non-European payment systems. From a blockchain perspective, this could open opportunities:

- Integrations of commercial bank tokens or tokenised deposits interoperable with the digital euro

- FinTechs and payment platforms building application layers (wallets, settlement, offline capability) with CBDC compatibility

- Stablecoin providers assessing competitive threats or partnership opportunities with central-bank-issued digital money.

Competitive and Regulatory Shifts

The project underscores that public digital money is now a strategic instrument. For crypto investors, this means:

- Private token projects should consider how they fit in a future landscape where CBDCs are established and accepted

- Regulation may increase, especially around tokenised money, wallet services, off-chain/on-chain interactions, and digital-asset rails ‹– with CBDC as the benchmark for trusted money.

- The design choices (holding limits, privacy features, offline capability, deposit migration) may set precedents for how public and private digital money coexist. Research suggests that without constraints (e.g., holding limits), CBDCs can amplify bank-run risk.

Strategic Timing for Investors

For those seeking new crypto-assets and income sources:

- Watch for opportunities around the infrastructure build-out: companies providing CBDC switch, wallets, rails, offline functionality may benefit.

- Tokenised instruments compatible with the digital euro or enabling layered services (e.g., merchant incentives, digital asset bridges) may become interesting.

- Be aware of regulatory risk: as central banks advance, private digital-money projects may come under closer scrutiny or need to differentiate in value-added services rather than “money substitution”.

5. Challenges & Considerations

Commercial-Bank Role and Deposit Outflows

One highlighted challenge is the potential for retail digital euro wallets to attract bank deposits, reducing banks’ funding bases. This is a concern raised especially in France and Germany. If many depositors migrate to an ECB wallet, banks may face higher funding costs or reduced intermediary roles. This tension between public money and commercial bank deposits is a structural one.

Cost & Technology Burden for Banks

Banks must invest significantly in infrastructure: compliance, wallet support, settlement, offline payments, cybersecurity. The ABI insists the costs must be spread out. According to some estimates, costs for banks could run into tens of billions for European retail banks.

Legislative & Design Uncertainty

The digital euro project remains contingent on EU legislation. The regulatory framework (e.g., on holding limits, privacy, offline use) is still being negotiated. From a crypto/blockchain viewpoint, these design decisions will influence how public money competes with or complements tokenised money and services.

Financial Stability Risks

Research shows that the introduction of a retail CBDC can increase bank-run risk in agent-based models unless proper safeguards are in place (e.g., holding limits). For the investor or developer, this means the broader ecosystem (banks, central banks, regulators) must manage stability, which may impact rollout speed and design.

6. What This Means for Japan-Based Investors and Blockchain Practitioners

For a user located in Tokyo (as per your profile) and interested in new crypto assets, income opportunities and practical blockchain applications, the digital euro initiative is not just European-centric:

- A successful digital euro may become a model for other major economies (e.g., digital yen, digital dollar). Observing its design and market response offers early-mover insight.

- FinTechs, wallet developers or token projects in Asia may look to Europe’s model for interoperability, compliance and infrastructure strategy.

- New cross-border use-cases may emerge: for example, European entities using the digital euro for payment into Asia, anchor-for tokens, or settlement between European and Asian counterparties.

- Crypto asset projects may position themselves as complementary to CBDC rails rather than purely competitive — e.g., offering programmable money services, layered smart-contracts on top of CBDC-compatible infrastructure.

7. Summary & Outlook

In summary: Italian banks support the digital euro project led by the ECB, but want a phased cost model and a twin-track approach with commercial bank currencies. The project has advanced into a new phase with technical readiness and legislative work underway, targeting a pilot by mid-2027 and possible issuance by 2029. For crypto investors and blockchain practitioners, the digital euro is a timely structural development — signaling how public digital money may evolve, how private tokenised money must adapt, and where new rails and services may emerge.

Looking ahead:

- Key upcoming milestones: the legislative process in 2026, pilot programmes starting in 2027.

- Infrastructure build-out by banks and payment providers will create opportunities for firms offering wallets, onboarding, settlement and interoperability services.

- Token-projects should consider how they align with or differentiate from public digital money — focusing on utility, programmability, value-added layers.

- Regulatory designs (holding limits, privacy, offline features) will shape the competitive landscape and the role of commercial bank digital currencies vs. public CBDC.

In conclusion: the digital euro is more than just another central-bank project — it may mark a pivot point in the way digital money and blockchain-based assets interplay. For those hunting new crypto assets, income opportunities and practical blockchain use-cases, this is a domain to watch closely.