Main Points :

- A $100B+ Australian pension fund (Hostplus) is considering crypto exposure via member-directed portfolios

- Bitcoin and digital assets may soon be integrated into retirement systems at scale

- Institutional adoption is accelerating globally across the U.S., Europe, and sovereign funds

- Younger demographics are driving demand for crypto exposure within pension structures

- Regulatory approval remains the decisive bottleneck for full-scale implementation

1. A Pension Giant Enters the Crypto Conversation

Australia’s Hostplus, a pension fund managing approximately $100 billion (≈$16 trillion JPY) in assets, is actively evaluating whether to introduce cryptocurrency investment options for its members. According to recent reports, the proposed integration would occur through its “Choiceplus” self-directed investment platform, allowing members to allocate a portion of their retirement funds into digital assets such as Bitcoin.

Currently, Choiceplus represents only about 1% of total assets under management, indicating that the initial rollout of crypto exposure would likely be limited in scope. However, the symbolic significance far outweighs the allocation size. Pension funds are traditionally conservative institutions, bound by fiduciary responsibility and strict regulatory frameworks. Even a small allocation toward crypto signals a meaningful shift in institutional perception.

Sam Sicilia, Hostplus’ Chief Investment Officer, noted that member demand for crypto exposure is non-negligible, especially among younger participants. Subject to regulatory approval, the fund is targeting a potential rollout as early as the 2026–2027 fiscal year.

This move is not an isolated experiment—it represents a broader structural transition where digital assets are gradually being legitimized within long-term retirement frameworks.

2. From Speculative Asset to Retirement Portfolio Component

Historically, cryptocurrencies have been categorized as high-risk speculative assets. However, the narrative is rapidly evolving. Bitcoin, in particular, is increasingly viewed as a macro hedge, digital gold, and asymmetric return vehicle.

The consideration by Hostplus reflects a critical shift:

- From retail-driven speculation → institutional portfolio allocation

- From short-term trading → long-term retirement exposure

- From unregulated experimentation → compliance-driven adoption

In practical terms, this evolution introduces several implications:

- Portfolio Diversification

Crypto offers low correlation with traditional asset classes such as equities and bonds. Even a small allocation can improve risk-adjusted returns. - Inflation Hedge Narrative

With persistent global inflation concerns, Bitcoin is increasingly positioned as a hedge against fiat debasement. - Access Democratization

Integrating crypto into pension products allows millions of individuals to gain exposure without directly managing wallets or exchanges.

For readers interested in blockchain applications, this represents a crucial inflection point: crypto is no longer just an external asset class—it is becoming embedded into financial infrastructure.

3. Global Institutional Momentum: A Coordinated Shift

Hostplus’ initiative aligns with a growing wave of institutional adoption across jurisdictions.

United States: Retirement Accounts Opening to Crypto

In 2025, U.S. policy took a notable turn when directives were issued to allow cryptocurrency investments within 401(k) retirement accounts. Regulatory sentiment has also softened, with leadership signaling openness toward integrating digital assets into mainstream financial products.

This development is significant because the U.S. retirement market represents trillions of dollars in capital. Even a 1–3% allocation shift into crypto would represent massive inflows into the digital asset ecosystem.Europe: Sovereign Wealth Funds Increasing Exposure

Norway’s sovereign wealth fund—one of the largest in the world—has indirectly increased its Bitcoin exposure to approximately 9,573 BTC, representing a 149% year-over-year increase.

This is not direct speculative investment but rather exposure through equity holdings in crypto-related companies. Nevertheless, it reflects a strategic acknowledgment that crypto is an emerging macro asset class.Asia-Pacific: Structural Adoption Begins

Australia’s Hostplus could become one of the first major pension funds in the region to formally integrate crypto into retirement offerings. If successful, it may trigger:

- Competitive responses from other pension funds

- Regulatory standardization across APAC

- Increased institutional-grade crypto products

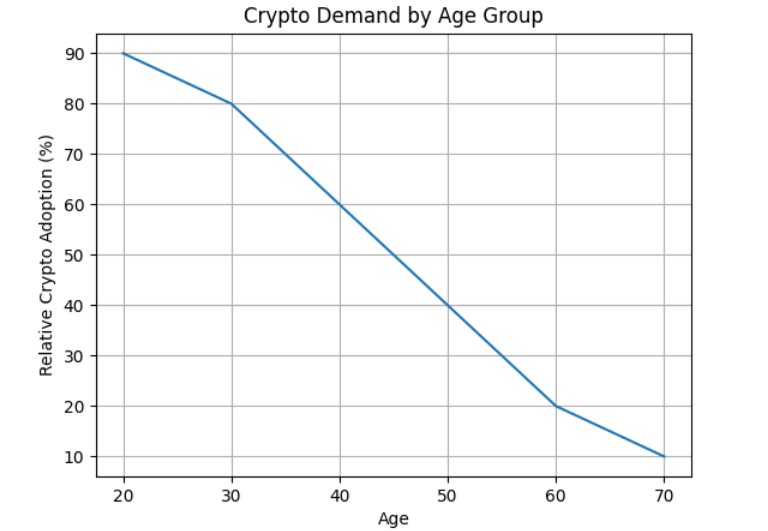

4. Demographics: The Real Driver Behind Crypto Integration

One of the most important factors in Hostplus’ decision is its relatively young member base, with an average age in the mid-to-late 30s.

This demographic shift has profound implications:

- Younger investors are digitally native and crypto-aware

- They exhibit higher risk tolerance compared to traditional retirees

- They demand greater control over investment choices

In contrast to older pension structures that prioritize capital preservation, younger members are increasingly seeking growth-oriented and alternative assets.

This creates a structural pressure on pension funds:

Adapt to new asset classes or risk losing relevance to future generations

From a business perspective, crypto integration is not just an investment decision—it is also a member retention and acquisition strategy.

5. Regulatory Bottleneck: The Final Gatekeeper

Despite growing momentum, regulatory approval remains the single most important constraint.

Key challenges include:

- Custody and security requirements

- Valuation and volatility risk management

- Compliance with fiduciary duty standards

- AML/KYC and reporting obligations

For pension funds, the threshold for regulatory approval is significantly higher than for retail platforms. Authorities must ensure that:

- Members are adequately informed of risks

- Exposure limits are clearly defined

- Operational risks are minimized

In Australia, regulators are still shaping the framework that would allow such offerings. The success or failure of Hostplus’ initiative will likely set a precedent for the entire region.

6. Strategic Implications for Crypto Markets

If pension funds begin allocating capital to crypto, the market dynamics will fundamentally change.

1. Reduced Volatility Over Time

Long-term capital from pension funds is less reactive than retail trading, potentially stabilizing price fluctuations.

2. Increased Institutional Liquidity

Large-scale inflows could deepen liquidity, making crypto markets more efficient and less fragmented.

3. Product Innovation Acceleration

Demand from institutional investors will drive:

- Regulated custody solutions

- Pension-grade crypto funds

- Hybrid financial products (TradFi + DeFi integration)

4. Shift Toward Blue-Chip Crypto Assets

Initial allocations will likely focus on:

- Bitcoin (BTC)

- Ethereum (ETH)

Smaller altcoins may benefit indirectly but will face higher scrutiny.

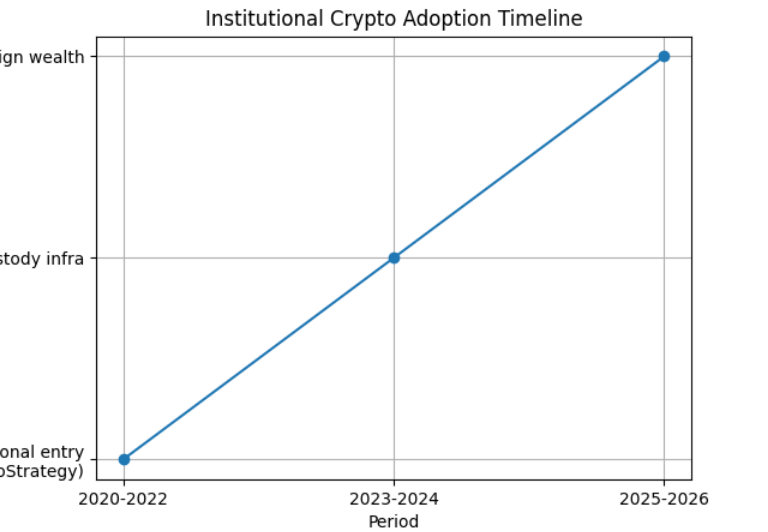

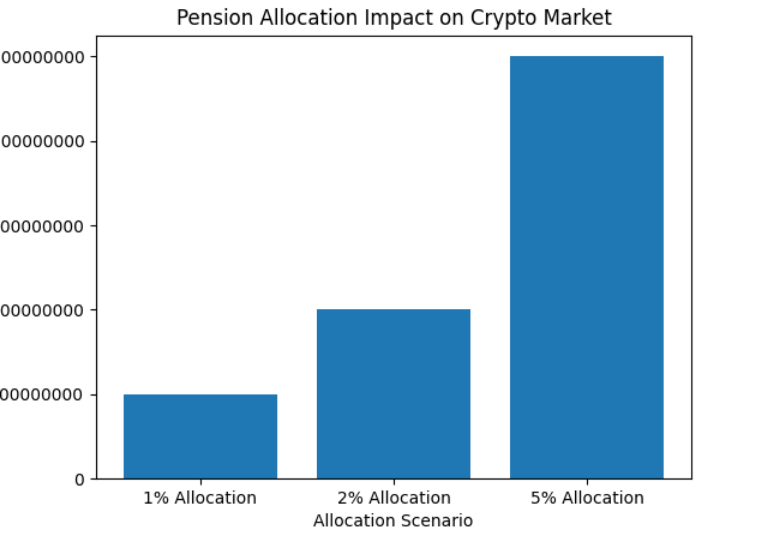

7. Visual Insight (Insert Below Section)

[Institutional Crypto Adoption Timeline]

A timeline chart showing:

- 2020–2022: Early institutional entry (hedge funds, MicroStrategy)

- 2023–2024: ETF approvals and custody infrastructure

- 2025–2026: Pension funds and sovereign wealth participation

[Pension Allocation Impact Model]

A bar chart showing:

- Global pension assets (~$50T+)

- 1%, 2%, 5% allocation scenarios into crypto

- Corresponding inflow estimates

[Demographic Demand Curve]

A curve illustrating:

- Crypto demand by age group

- Younger cohorts showing significantly higher adoption

8. Conclusion: Controlled Experiment or Structural Shift?

The potential move by Hostplus is more than a headline—it is a signal of a deeper transformation in global finance.

At face value, the initiative may appear cautious:

- Limited allocation

- Conditional regulatory approval

- Restricted to self-directed portfolios

However, structurally, it represents something far more significant:

The integration of decentralized assets into the most conservative segment of financial systems—retirement funds.

If successful, this model could scale rapidly:

- Other pension funds may follow

- Regulatory frameworks may standardize

- Crypto could become a default portfolio component

For investors, builders, and institutions, the message is clear:

The question is no longer whether crypto will be institutionalized—but how fast and under what structure.