Main Points:

- US revolving credit—including credit-card balances—has surged to $1.3 trillion, expanding at an annualized 4.9% pace.

- The average credit-card interest rate now exceeds 21%, intensifying household liquidity pressures.

- Consumers increasingly depend on short-term revolving credit while avoiding long-term loans, revealing financial stress rather than confidence.

- As household liquidity tightens, discretionary investment capital shrinks—potentially decreasing retail buyers for Bitcoin and altcoins.

- Credit-limit tightening by banks may reduce the ability of consumers to leverage debt for speculative crypto positions.

- Macro liquidity conditions for 2026 may hinge on holiday-season spending patterns and early-year debt repayments.

- Tight consumer liquidity historically correlates with weaker retail crypto inflows, particularly in high-volatility assets.

Introduction

Over the past year, the cryptocurrency market has shown resilience amid shifting macroeconomic conditions, but a new risk factor is emerging from an unexpected source: US household revolving debt, which has ballooned to an unprecedented level. The Federal Reserve’s latest report shows that October revolving credit—primarily credit-card balances—reached $1.3 trillion, expanding at an annualized 4.9% pace. Although overall consumer credit growth slowed, the composition of borrowing reveals a troubling pattern: Americans are depending more heavily on high-interest short-term credit to manage daily expenses, not discretionary spending.

For crypto investors, particularly those tracking Bitcoin’s liquidity cycles, household debt data matters in a structural way. Retail inflows historically play a decisive role in accelerating bullish trends. When liquidity tightens, speculative capital dries up—and Bitcoin’s price often stagnates regardless of institutional inflows.

This article synthesizes the original report, expands it with broader macroeconomic context, examines data from recent credit-market trends, and evaluates the implications for Bitcoin, altcoins, and the broader digital-asset ecosystem.

Section 1 — US Household Debt Is Rising Faster Than Income

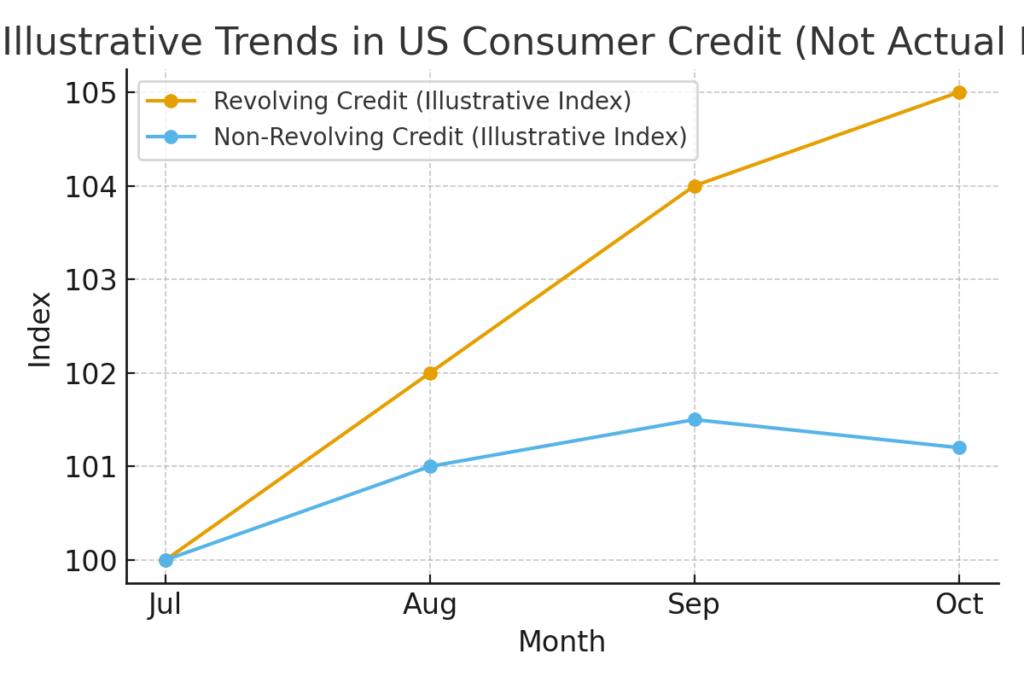

1.1 Revolving Credit Hits $1.3 Trillion

Revolving credit—credit-card balances, flexible borrowing lines, and similar instruments—rose at 4.9%, accelerating from September’s 4% expansion. This uptick directly reflects household cash-flow strain: consumers rely on credit cards not for optional spending but to maintain basic liquidity.

1.2 Long-Term Loans Are Losing Demand

Non-revolving credit (e.g., auto loans), by contrast, slowed sharply from 2.1% to 1.2% growth, signaling consumers’ reluctance to make long-term commitments.

A divergence like this is a known macro signal:

- Revolving up + Non-revolving down = Household liquidity stress, not healthy consumption.

This matters profoundly for crypto markets because constrained households typically reallocate away from volatile assets—including Bitcoin—preferring cash preservation.

Section 2 — Interest Rates: A Painful 21% Reality

2.1 Credit-Card APR Above 21%

Average US credit-card interest rates now exceed 21.3%, compared to 14.7% five years ago. This makes it more expensive than ever for households to carry balances.

2.2 Why Are Balances Rising Even When Rates Are High?

Three explanations dominate:

- Liquidity Preservation Behavior

Consumers prefer to keep cash on hand even if it means incurring high interest. - Inflation’s Lingering Effects

Real wages have not fully recovered relative to cumulative price increases. - Structural Shift After BNPL (Buy Now Pay Later)

The more people juggle payment products, the harder it becomes to escape debt cycles.

This financial pressure reduces the ability of average Americans to allocate funds toward Bitcoin or altcoins—especially during drawdowns where dollar-cost averaging (DCA) typically occurs.

Section 3 — Credit-Limit Dynamics: A Hidden Constraint on Bitcoin Liquidity

3.1 Forty Percent Received a Limit Increase—But Not By Choice

Over the past year:

- 40% of cardholders received credit-limit increases

- 56% of those increases were automatic

- 67% of consumer-requested increases were denied

Banks are clearly tightening risk criteria.

3.2 Behavioral Shifts After Limit Denials

When a request is denied:

- 31% reduce card usage

- 20% apply for a new card

- Others shift to BNPL or alternative financing

Reduced spending power means less speculative capital flows into crypto—particularly from retail traders who use discretionary cash or credit to fund positions.

3.3 Why This Matters to Crypto Markets

Retail liquidity is a major driver behind:

- Rapid altcoin rotations

- Breakout momentum in mid-cap tokens

- Spot buying pressure during Bitcoin rallies

A reduction in credit-driven liquidity represents a structural headwind for the entire crypto ecosystem.

Section 4 — Macro Indicators That Directly Affect Bitcoin

We combine the article’s insights with broader macro data from the Federal Reserve, Bank of America consumer spending reports, and recent crypto-market flows.

4.1 Higher Household Debt → Lower Risk Appetite

Historically, periods of tight consumer liquidity correlate with:

- Decreased participation in spot crypto purchases

- Lower retail volumes on Coinbase, Binance.US, and Robinhood

- Longer accumulation periods before new highs

4.2 Year-End Spending Will Set the Tone for 2026

Between December and February, households typically:

- Increase spending during holidays

- Repay balances in January

- Rebuild liquidity in February–March

If consumer repayment rates fall below seasonal norms, Bitcoin inflows could weaken going into Q1 2026.

Section 5 — Could the “Revolving Debt Spiral” Hit Bitcoin in 2026?

5.1 Retail Investment Capital Is Shrinking

Retail investors were a powerful force during:

- The 2017 bull market

- The 2020–2021 institutional expansion

- The 2024 halving rebound

But current data signals:

- Less disposable income

- Fewer credit options

- Higher debt servicing costs

Bitcoin can rise on institutional demand alone, but it cannot sustain parabolic rallies without retail participation.

5.2 Risk: Decline in Altcoin Discoverability

For your audience—readers interested in new assets and revenue opportunities—one critical effect stands out:

Altcoin rotations will slow when retail investors have less liquidity.

This means:

- Fewer speculative surges

- Longer accumulation periods

- Higher focus on utility-driven tokens

- Strong rotation into fundamentally backed assets (e.g., real-world asset tokens, AI-linked tokens, and infrastructure plays)

Section 6 — Opportunities for Crypto Projects and Investors

Even under liquidity stress, new opportunities emerge.

6.1 Bitcoin as a Long-Term Hedge

Institutional demand continues expanding through:

- Spot Bitcoin ETFs

- Pension fund allocations

- Corporate treasury diversification

This provides structural support even as retail liquidity thins.

6.2 Altcoin Opportunities Shift Toward Utility

In tight liquidity cycles, strong themes typically outperform:

| Theme | Why It Matters |

|---|---|

| AI + Crypto | High VC inflows, strong narrative |

| Real-World Assets (RWA) | Institutional demand for tokenized bonds & treasury exposure |

| Layer-2 (L2) Efficiency Projects | Lower costs attract builders even in down cycles |

| Payments & Stablecoin Infrastructure | Real economic use cases continue expanding |

6.3 When Retail Liquidity Returns

Historically, retail returns when:

- Credit balances decrease

- Wage growth stabilizes

- Consumer sentiment improves

- Interest rates fall

This aligns with possible Fed cuts projected for late 2026.

Conclusion

US household revolving debt continues to rise despite historically high borrowing costs, signaling deepening financial stress. This shift constrains discretionary investment capital, especially among retail investors who have historically driven volatile crypto cycles.

Bitcoin remains structurally supported by institutional adoption, but altcoins may face reduced liquidity until household debt stabilizes. The coming months—especially holiday spending trends and early-year debt repayments—will significantly influence crypto market participation in 2026.

For investors and builders seeking the next wave of opportunity, this environment favors fundamentally strong projects, real-world utility, and institutional-aligned infrastructure, rather than pure speculative plays.