Main Points :

- Hong Kong will launch a tokenized bond issuance and settlement platform in March 2026.

- The government will issue its first fiat-referenced stablecoin licenses, strengthening regulatory clarity.

- The initiative aims to attract global crypto firms and institutional capital under a structured compliance regime.

- The HKMA is advancing Project Ensemble, testing tokenized deposits and digital asset settlement infrastructure.

- The move positions Hong Kong as a strategic bridge between traditional finance, Web3 innovation, and mainland China.

- Stablecoin regulation could accelerate cross-border settlement, RWA tokenization, and institutional DeFi adoption.

Introduction: A Defining Moment for Digital Finance in Asia

Hong Kong is preparing to launch a tokenized bond platform in March 2026 while issuing its first licenses for fiat-referenced stablecoin issuers within months. This dual initiative represents one of the most comprehensive government-backed digital asset frameworks in Asia.

Rather than approaching crypto through speculation alone, Hong Kong is focusing on regulated infrastructure—tokenized sovereign and corporate bonds, licensed stablecoin issuance, and blockchain-based financial settlement rails. For investors seeking new digital assets, yield opportunities, and practical blockchain applications, this development is more than policy news—it is structural market evolution.

In this article, we analyze the implications of Hong Kong’s tokenization strategy, incorporate recent global developments, and evaluate what this means for capital flows, stablecoin markets, and real-world asset (RWA) tokenization.

Hong Kong’s Tokenized Bond Platform: Infrastructure Before Speculation

Hong Kong will introduce a digital asset platform designed to support the issuance and settlement of tokenized bonds. Unlike purely crypto-native initiatives, this platform focuses on regulated fixed-income instruments.

Tokenized bonds allow traditional debt securities to be issued, recorded, and settled on blockchain networks. The benefits include:

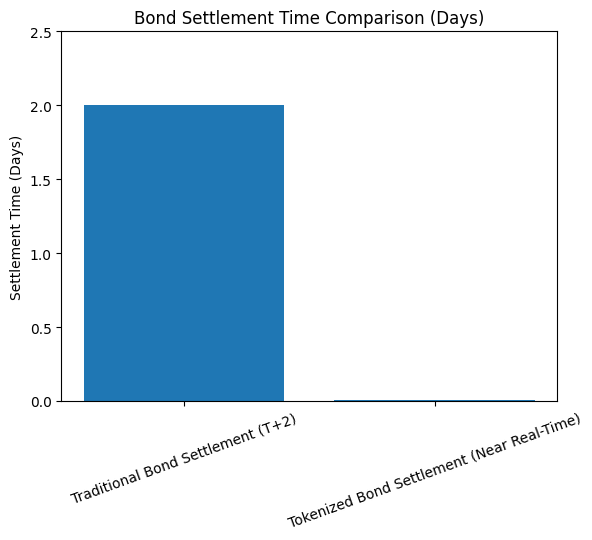

- Reduced settlement time (near real-time vs. T+2)

- Lower reconciliation costs

- Transparent ownership tracking

- Fractionalization for broader investor access

The Hong Kong Monetary Authority (HKMA) has already conducted pilot tokenized green bond issuances in prior years. The new platform represents institutionalization of that effort.

For yield-focused investors, tokenized bonds represent a bridge between traditional fixed income and programmable finance. If Hong Kong succeeds, secondary markets for tokenized sovereign and corporate bonds may emerge, enabling collateralized lending, DeFi integration, and automated compliance logic.

The First Fiat-Referenced Stablecoin Licenses

Hong Kong Financial Secretary Paul Chan announced during the 2026–2027 budget speech that the region will begin issuing stablecoin licenses in March.

Under the new framework:

- Approved companies can issue fiat-backed stablecoins.

- Issuers must operate under clear regulatory supervision.

- Compliance, reserve transparency, and risk management will be mandatory.

This move is critical because regulatory clarity has become the global bottleneck for stablecoin expansion.

Globally, the stablecoin market has exceeded $100 billion in total capitalization (USD equivalent), with USDT and USDC dominating. However, regulatory fragmentation—especially between the U.S., EU (MiCA), and Asia—has limited institutional adoption.

Hong Kong’s approach could provide:

- Institutional-grade stablecoin settlement rails

- Regulated cross-border payment infrastructure

- Integration with tokenized bonds and deposits

For crypto entrepreneurs, this is not merely about launching another stablecoin. It is about building programmable settlement infrastructure connected to one of Asia’s largest capital markets.

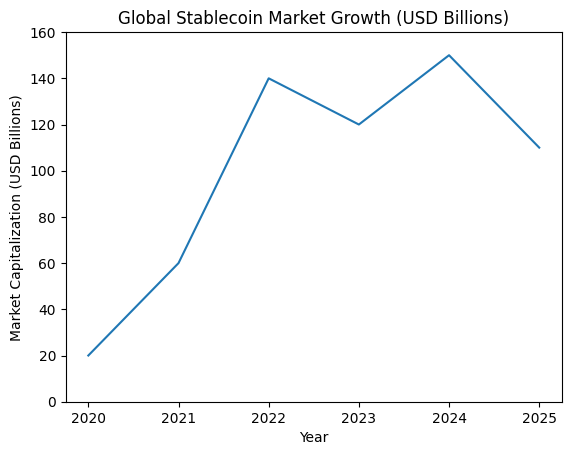

Global Stablecoin Market Growth (USD Equivalent)

Description: A line chart showing growth from $20 billion (2020) to over $100 billion (2025).

Project Ensemble and Tokenized Deposits

Beyond bonds and stablecoins, HKMA has launched the testing phase of Project Ensemble, a sandbox exploring tokenized deposits and digital asset transactions.

Tokenized deposits differ from stablecoins:

- Stablecoins are typically issued by private entities and backed by reserves.

- Tokenized deposits are representations of commercial bank liabilities on blockchain.

If successfully implemented, tokenized deposits could:

- Enable atomic settlement of securities

- Reduce counterparty risk

- Facilitate programmable escrow

- Integrate directly with central bank systems

This positions Hong Kong at the frontier of real-world asset tokenization—one of the fastest-growing segments in blockchain.

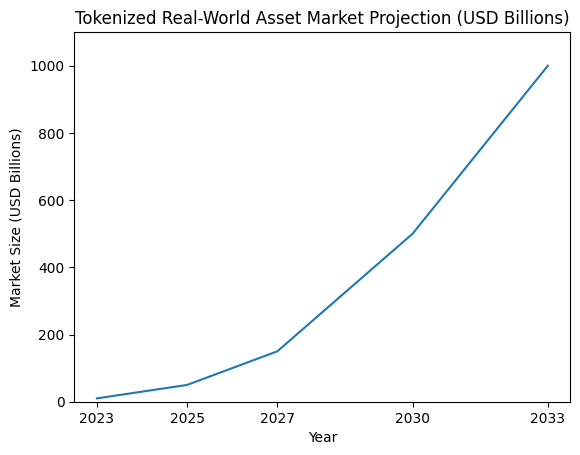

According to various industry reports, tokenized real-world assets could exceed $1 trillion (USD equivalent) within the next decade. Bond markets alone represent over $100 trillion globally. Even a small percentage moving on-chain would reshape financial infrastructure.

Tokenized Real-World Asset Market Projection (USD Equivalent)

Description: Bar projection from $10 billion (2023) to $1 trillion (2033).

Strategic Positioning: China, Asia, and Global Capital

Hong Kong’s digital asset expansion must be understood geopolitically.

Mainland China maintains strict crypto trading restrictions. However, Hong Kong operates under a separate regulatory framework. By developing compliant tokenization infrastructure, Hong Kong becomes:

- A testing ground for regulated digital finance

- A capital bridge between China and global crypto markets

- A compliant alternative to offshore crypto hubs

Paul Chan indicated the initiative would strengthen China’s position in digital asset development. While mainland retail crypto remains restricted, infrastructure experimentation through Hong Kong could shape regional financial modernization.

For institutional investors in Japan, Singapore, the Middle East, and Europe, Hong Kong may offer:

- Regulatory clarity

- Deep capital markets

- Proximity to Chinese enterprises

- Strong legal frameworks

Implications for Investors and Builders

1. Stablecoin Issuers

Companies seeking to issue fiat-backed stablecoins may now view Hong Kong as a strategic base. The licensing regime reduces regulatory ambiguity and may attract both fintech startups and traditional banks.

2. RWA Tokenization Platforms

Firms specializing in tokenized bonds, funds, or structured products may integrate with Hong Kong’s platform to gain legitimacy and institutional access.

3. Cross-Border Settlement Providers

With stablecoins and tokenized deposits, cross-border trade finance, remittances, and treasury operations could become significantly more efficient.

4. DeFi Institutionalization

Regulated tokenized bonds could serve as compliant collateral in permissioned DeFi environments.

Tokenized Bond Lifecycle vs Traditional Bond Settlement

Description: Side-by-side process flow comparison showing reduction in intermediaries and settlement time.

Risks and Challenges

Despite optimism, several challenges remain:

- Stablecoin reserve transparency must be audited rigorously.

- Interoperability with global stablecoins (USDT, USDC) must be addressed.

- Liquidity fragmentation may occur between licensed and offshore markets.

- Regulatory arbitrage remains a risk if standards differ across jurisdictions.

Moreover, institutional adoption depends on secondary market liquidity. Without active trading venues, tokenized bonds risk becoming merely digitized static instruments.

Broader Market Context

Globally, governments are converging on three themes:

- Regulated stablecoins

- Tokenized sovereign debt

- Central bank experimentation with digital settlement

The European Union’s MiCA regulation, the U.S. stablecoin legislative debates, and Singapore’s Project Guardian all signal structural change.

Hong Kong’s model combines all three in a coordinated manner.

For investors seeking new revenue streams, tokenized fixed income may provide yield exposure, while stablecoin infrastructure may underpin next-generation payment rails.

Conclusion: Infrastructure Is the Real Bull Market

Hong Kong’s March launch of a tokenized bond platform and its first stablecoin licenses represents more than incremental regulation—it signals the institutionalization of blockchain within mainstream finance.

Rather than speculative hype cycles, the focus is shifting toward:

- Regulated issuance

- Compliance-based innovation

- Infrastructure modernization

- Cross-border programmable settlement

If successful, Hong Kong could become Asia’s primary digital asset gateway—bridging sovereign debt markets, stablecoin liquidity, and blockchain-native capital flows.

For investors, the opportunity lies not only in token prices but in:

- Licensed stablecoin ecosystems

- RWA tokenization platforms

- Infrastructure providers

- Compliance-first fintech builders

The next crypto cycle may not be driven solely by memes or narratives—but by governments building the rails.

And Hong Kong intends to be at the center of that transformation.