Main Points :

- The CEO of Standard Chartered emphasises that Hong Kong’s pilot of tokenised deposits and HKD-backed stablecoins could become a key medium of exchange for cross-border commerce.

- The Securities and Futures Commission (SFC) has issued new rules under its “ASPIRe” roadmap enabling locally-licensed virtual asset trading platforms (VATPs) to share global order books with overseas affiliates, aiming to enhance global liquidity, tighten spreads and improve price discovery.

- The regulatory framework, while liberalising access, retains safeguards (pre-funding, delivery-versus-payment, compensation reserves, joint surveillance) to mitigate settlement and operational risk.

- For crypto investors and blockchain practitioners, these developments open new opportunities: HKD-stablecoin use cases in trade finance, tokenised deposits as infrastructure, and a Hong Kong-based regulated hub able to link global liquidity.

- However, risks remain: regulatory execution, adoption curve, interoperability with existing settlement systems, and the actual rollout of tokenised money in trade flows.

1. Setting the Scene: Hong Kong’s Shift Toward Digital Assets

In recent months, Hong Kong has accelerated its ambition to become a global digital-asset and tokenisation hub. The city’s regulator, the SFC, has shifted from a relatively closed-loop model for virtual asset trading platforms (VATPs) — where order books and liquidity were largely confined domestically — toward a model enabling global-order-book access.

This move comes amid broader pressure for financial centres to modernise cross-border payments, digitise settlement mechanisms, reduce frictions and attract institutional capital. For practitioners looking at blockchain use-cases beyond retail speculation, the infrastructure and regulatory backdrop are increasingly important.

Against this backdrop, the CEO of Standard Chartered, Bill Winters, delivered remarks at Hong Kong FinTech Week in November 2025 that underscore the importance of tokenised deposits and HKD-backed stablecoins for trade settlement.

He signalled that while the digital flow of funds is not yet fully realised, the innovations being trialled in Hong Kong point toward a “really interesting currency of exchange” or medium of exchange for international trade: namely a tokenised deposit plus HKD-stablecoin architecture.

2. Tokenised Deposits & HKD-Stablecoins: What’s Going On?

Under the hood, the pilots taking place in Hong Kong include several notable components:

Tokenised deposits – Financial institutions are exploring the issuance of tokenised versions of bank deposits (or deposit-like claims) on blockchain or ledger infrastructure, enabling programmable features, faster transfers, and smart-contract connectivity.

HKD-backed stablecoins – Hong Kong-dollar-pegged stablecoins are being developed under the supervision of the Hong Kong Monetary Authority (HKMA) via a sandbox regime. A joint venture between Standard Chartered (Hong Kong unit), Animoca Brands and HKT announced a licensing application to issue an HKD-stablecoin.

Winters argued these components “could lay the foundation for a new era of digital trade settlement.”

In other words, instead of relying solely on traditional correspondent banking, multiple time-zone delays and FX settlement cycles, a tokenised deposit + HKD-stablecoin could function as a near-instant (or at least highly reduced settlement-time) medium of exchange across borders.

For a blockchain-practitioner or investor, that means the stablecoin and tokenisation infrastructure are not mere speculative assets but part of an overlay on trade flows. If adopted, there may be new business models: trade-finance platforms, tokenised invoice settlement, liquidity on programmable rails, stablecoin pairs pegged to the HKD, etc.

3. The Regulatory Framework: SFC’s ASPIRe Roadmap & New Rules

Crucial to the above is the regulatory infrastructure being put in place by the SFC. At FinTech Week, SFC Chief Executive Julia Leung laid out that Hong Kong is transitioning from a closed regime to one integrated with global liquidity.

The key changes include:

- Licensed VATPs in Hong Kong may share a “global order book” with overseas affiliates — enabling order-flow, matching and pricing that taps global liquidity pools (Pillar A “Access”).

- Platforms may expand their offerings: tokenised securities and HKMA-licensed stablecoins are now explicitly permitted under the rules (Pillar P “Products”).

- Safeguards remain: required pre-funding of overseas affiliates, settlement on delivery-versus-payment (DVP) basis, unified market surveillance across jurisdictions, compensation reserves for client-asset protection.

These changes mark a strategic pivot: Hong Kong is signalling to the crypto industry and institutional players that it intends to align its digital asset ecosystem with global-grade liquidity, while maintaining investor protection frameworks.

4. Implications for Crypto Investors, Blockchain Practitioners & New Asset Searchers

For readers searching for new crypto assets or deploying blockchain in practice, what do these developments imply?

a) New Stablecoin Use-Case Opportunity

An HKD stablecoin issued by regulated participants (banks + fintech + telecom) under the HKMA sandbox could become a significant medium of exchange in trade finance. For example, invoice settlement across Asia-Pacific could leverage such a stablecoin, reducing FX conversion steps and settlement delays. If this adoption occurs, there may be opportunities in platforms that integrate with that stablecoin ecosystem (payment rails, liquidity pools, cross-chain bridges).

b) Tokenisation Infrastructure as Investment & Build Opportunity

Tokenised deposits imply that banks or fintech firms may issue on-chain deposit-claims. For blockchain developers (such as yourself) this means potential work in interoperability, wallet SDKs (non-custodial), settlement engines, smart-contract issuance of deposit tokens, APIs for trade-settlement. The emergence of such infrastructure can open revenue streams beyond speculation on tokens.

c) Liquidity & Global Order-Book Access: Better Pricing for Assets

With the SFC enabling global order-book access, if platforms in Hong Kong acquire large volumes of liquidity, the spreads might tighten and price discovery improve for digital assets listed via those platforms. That potentially reduces one friction for investors looking to deploy capital in new assets.

d) Strategic Geography: Hong Kong as Tokenisation Hub

Hong Kong positioning itself as a hub could attract new entrants: stablecoins, tokenised securities, cross-border payments, trade-finance rails. For new asset projects — e.g., those you might evaluate for ICO/presale or even wallet integrations — leveraging Hong Kong regulatory clarity may become an advantage (depending on jurisdiction implementation).

e) Risk-Adjusted View: Timing Risk, Adoption Risk, Regulatory Risk

However, the unspoken challenge remains: pilots ≠ mainstream adoption. Issuers still need to roll out the HKD stablecoin, banks must embed use-cases, trade-finance participants must adopt. Execution risk remains high. Also, jurisdictions elsewhere (US, EU) are advancing own frameworks — so competitive risk is real.

For an investor, this means any bet tied to these developments (e.g., in tokens, infrastructure companies) must assume a timeline of 1-3 years and risk that regulatory or operational setbacks delay adoption. For a developer/practitioner, it means building for flexibility, cross-jurisdiction, modular infrastructure.

5. Real-World Use Cases & What to Monitor

Let’s sketch a few concrete use-cases and what to track:

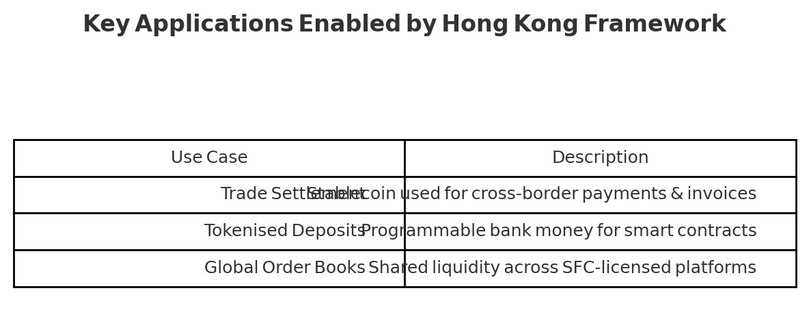

Use-Case 1: Cross-Border Trade Settlement via HKD Stablecoin

Imagine a Hong Kong exporter sells to a buyer in Southeast Asia; payment is made via an HKD-stablecoin issued by the joint venture (Standard Chartered/Animoca/HKT). Settlement is near-real-time on-chain, smart contracts verify invoice/milestones, tokenised deposit holds funds until delivery, then auto-release.

What to monitor:

- When the HKMA issues first stablecoin licences.

- Which banks/fintechs become issuers or participants.

- Which trade-finance platforms integrate the stablecoin in Asia-Pacific corridors.

Use-Case 2: Tokenised Deposits & Interbank Settlement

Banks issue tokenised versions of deposits, enabling programmable money (e.g., interest-bearing deposit tokens, automatic transcend of jurisdictional rails). These can interoperate with stablecoins, enabling more fluid interbank or institutional flows.

What to monitor:

- Pilot announcements of tokenised bank deposits in Hong Kong.

- Partnerships between banks and blockchain infrastructure providers.

- Standards adopted for tokenised money (ERC-20, other chain, inter-ledger).

Use-Case 3: Digital Asset Trading Platforms with Global Order-Book

Hong Kong-licensed virtual asset platforms tap global liquidity, allowing investors (including token projects) to access tighter spreads, deeper markets. This is relevant for new token launches seeking compliant listing and liquidity support in Asia.

What to monitor:

- Which VATPs are pivoting their order-book infrastructure.

- How token issuance and listing requirements evolve under SFC rules.

- Whether projects choose Hong Kong-based platforms for listing vs other jurisdictions.

6. Strategic Advice for Investors and Practitioners

For you, given your interest in new assets, blockchain use, wallet design (non-custodial, swaps) and financial infrastructure, here are some strategic take-aways:

- Explore HKD-backed stablecoin exposure: Keep a watch on which token issuers or platforms will launch HKD pegged coins in Hong Kong. These could become base pairs in Asia-Pacific corridors and offer unique yield or utility possibilities.

- Design wallet infrastructure with settlement rails in mind: Since you are working on a non-custodial wallet and implementing swaps (BTC→ETH etc), consider supporting emerging rails (tokenised deposits, regulated stablecoins). For instance, your wallet could integrate HKD-stablecoin flows or tokenised deposit tokens as settlement options.

- Position for token-economy infrastructure adoption rather than just speculation: Projects which build infrastructure (settlement stacks, wallet SDKs, trade-finance smart contracts) may gain from the regulatory tailwinds in Hong Kong. Evaluate projects beyond token price—look at real usage, partnerships with regulated entities.

- Monitor regulatory milestones and rollout timelines: Because pilots are in progress, get clarity on when licences are issued, when institutional adoption begins, and when trade-finance flows shift to on-chain rails. These will signal when infrastructure and associated token/asset value may ramp.

- Consider cross-jurisdiction arbitrage: Hong Kong’s move may create new entry-points for digital-asset issuance or trading services in Asia that are different from US/EU norms. For token projects or wallet integrations, being early in this corridor may offer advantages (liquidity, regulatory clarity, stablecoin pairs).

- Risk-manage and stay flexible: While the tailwinds are strong, the real-world adoption maybe slower than hype. Build for modularity, avoid over-commitment to one rail or chain, and evaluate token/infrastructure projects with scepticism—especially regarding time to adoption and regulatory execution.

7. Emerging Trends & Additional Context

Beyond the immediate article, some recent developments add context:

- Hong Kong is actively issuing digital-asset platform licences and evaluating derivatives/margin trading products for digital assets.

- The regulatory shift toward global order-book linkage is seen as necessary because fragmenting liquidity is a major barrier in crypto markets; Hong Kong’s move aims to link to global pools.

- Meanwhile, mainland China has given informal guidance to some brokerages to pause real-world-asset (RWA) tokenisation business in Hong Kong, signalling a potential regulatory headwind from Beijing.

- For stablecoins, the global race is heating: US, EU and Asia are working on frameworks. Hong Kong’s HKD-stablecoin initiative competes in that broader narrative, meaning projects in this region may benefit from being early.

- From an asset-allocation perspective, stablecoins backed by regulated fiat and issued by major banks/sandboxes may be viewed more as infrastructure tokens than speculative coins—but still require adoption.

8. What This Means for “Next Source of Revenue” in Crypto & Blockchain

From a revenue-perspective, especially for those looking beyond simply trading coins, the developments in Hong Kong offer several avenues:

- Fee models around settlement/rails: If trade-finance uses HKD-stablecoin rails, there will be demand for wallet integrations, transaction-monitoring services, compliance SDKs, regulatory interface modules.

- Token issuance platforms and listing services: Projects seeking to issue in or via Hong Kong may require issuance infrastructure, token-engineering, compliance frameworks—this is a service market.

- Liquidity-providing and market-making for regulated order-book access: As platforms open to global order books, market-making, liquidity-provision services, and token-listing strategy will be important.

- Wallet features for non-custodial users bridging the old and new rails: Your wallet’s ability to swap between traditional assets and tokenised/stablecoin rails could become a differentiator. Integrating HKD-stablecoin, tokenised deposits, bridging protocols adds utility and revenue potential (swap fees, integrations, SDK licensing).

- Data, analytics, compliance and audit layers for tokenised money: Regulators will expect transparency, monitoring, settlement-risk control. Companies that provide these layers will be sought after.

Thus, for readers seeking “the next revenue source,” building services and infrastructure around tokenised money and stablecoins (especially in Asia-Pacific) may deliver more sustainable value than pure speculative token plays.

Conclusion

In sum, Hong Kong’s strategic push toward tokenised deposits and HKD-backed stablecoins, combined with the SFC’s new regulatory framework enabling global liquidity access, is a material step in the evolution of blockchain-enabled trade-finance and cross-border settlement. For investors and practitioners focused on new crypto assets and practical blockchain applications, this opens avenues beyond speculation: infrastructure building, service revenue, wallet and settlement integration, token issuance assistance, and pairing with regulated fiat-token rails.

However, as always, timing, execution and ecosystem adoption remain critical. Pilots need to scale; trade flows need to migrate; the rails must interoperate with the real world. By monitoring key milestones (licences, pilot roll-outs, trade-finance use-cases, platform launches) and positioning your wallet/dev stack accordingly, you increase your chances of capturing value when these rails move from “being tested” to “being deployed at scale.”

For those hunting for the next source of revenue: consider stablecoins not just as “coins to trade” but as foundational infrastructure that underpins new business models in tokenised money and blockchain rails. And consider regions like Hong Kong, where regulatory clarity and institutional participation are aligning, as strategic early-adoption theatres.