Main Points :

- Traditional finance institutions now account for 46% of crypto market influence, up sharply from 31% in 2025

- Crypto ETFs have become the primary gateway for institutional capital, with AUM reaching $140 billion

- Bitcoin is increasingly viewed as a core portfolio asset, not a speculative frontier investment

- Market structure risks remain, as shown by the 2025 Bitcoin crash driven by excessive leverage

- Infrastructure, compliance, and tokenization now dominate investment priorities, while consumer UX declines

- Power dynamics are shifting from retail innovation toward institutional consolidation and absorption

1. A Structural Turning Point for the Crypto Industry

The global digital asset industry has entered a decisive transition phase. According to a newly released survey by CfC St. Moritz, an invitation-only digital asset conference held annually in Switzerland, the long-anticipated institutional adoption of crypto has finally arrived—but not in the way early crypto advocates imagined.

Rather than a gradual coexistence between decentralized innovators and traditional finance, the market is now experiencing a fundamental restructuring. Traditional financial institutions are no longer merely experimenting with blockchain technology. They are actively reshaping market infrastructure, liquidity flows, and competitive dynamics.

CfC St. Moritz surveyed 242 senior participants from crypto firms, banks, asset managers, regulators, and technology providers. Their collective view reflects the perspective of those now operating at the core of global digital finance rather than its periphery.

2. TradFi’s Accelerating Entry: From Skepticism to Market Control

For years, large banks and exchanges dismissed cryptocurrencies as immature or dangerous. That posture has reversed dramatically.

In early 2026, institutions such as JPMorgan Chase and UBS began exploring broader crypto service offerings for clients. BNY Mellon launched tokenized deposit products, while the New York Stock Exchange established a platform dedicated to tokenized securities. London Stock Exchange Group followed with a digital asset settlement initiative.

These moves go far beyond technology pilots. They represent direct competition with native crypto exchanges and infrastructure providers.

According to the CfC survey, 46% of respondents believe that traditional financial institutions are now dominating what was once a retail-driven crypto market, a sharp rise from 31% the year before.

Growth of TradFi Dominance in Crypto Markets (%)

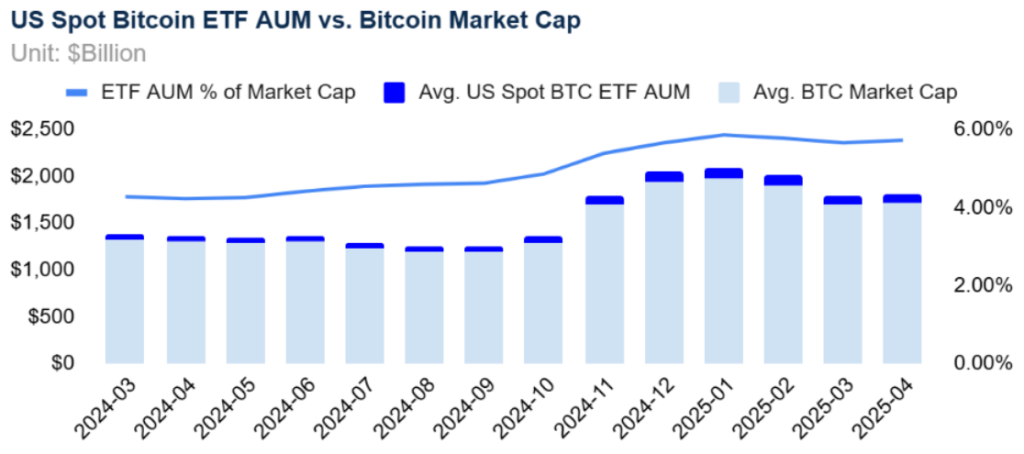

3. ETFs: The Institutional On-Ramp That Changed Everything

One of the most transformative developments has been the explosive growth of digital asset exchange-traded funds.

U.S. regulatory disclosures show that more than 2,000 regulated institutional investors now hold crypto ETFs. Total assets under management surged to $140 billion within just two years.

Central banks are taking note. In December, the Banque de France concluded that ETFs represent the most effective mechanism for bringing Wall Street capital into crypto markets at scale.

Digital Asset ETF AUM Growth (USD billions)

This ETF-driven influx has changed market behavior, liquidity distribution, and risk dynamics. Crypto markets now increasingly resemble traditional capital markets—with both the benefits and vulnerabilities that implies.

4. Market Volatility: Stabilization or Illusion?

Institutional participation initially reduced volatility, as deeper pockets and longer investment horizons smoothed price movements. However, this perceived stability was challenged on October 10, 2025, when Bitcoin experienced a sharp and sudden crash.

The event exposed persistent structural weaknesses: excessive leverage, fragile liquidity, and overreliance on automated trading strategies.

Don Wilson, CEO of crypto trading firm DRW, described the crash as “a stress test the industry failed.”

As a result, industry optimism declined. The CfC optimism index fell from 73% to 68%, while expectations for IPOs and venture capital activity dropped sharply. Forecasts of consolidation and M&A doubled, signaling a shift toward fewer, larger players.

5. Bitcoin’s Evolution Into a Portfolio Anchor

Despite these challenges, institutional perception of Bitcoin has fundamentally changed.

- 45% of respondents now see Bitcoin as an established portfolio diversification asset

- 35% view it as digital gold and a long-term store of value

A senior strategist at State Street noted that as global macro volatility increases, Bitcoin may transition from a frontier asset into a foundational component of next-generation portfolio construction.

In a historic milestone during 2025 market turmoil, Bitcoin’s volatility temporarily fell below that of U.S. Treasuries, underscoring how dramatically its risk profile has evolved.

6. Tokenization Takes Center Stage

Tokenization ranked as the second-most promising fintech domain in the survey. A striking 83% of respondents believe that real-world assets and traditional financial instruments will increasingly move on-chain.

This shift reflects growing knowledge transfer between traditional finance and crypto-native firms. As Kaiko CEO Ambre Soubiran observed, tokenization has become the clearest symbol of convergence between the two worlds.

7. Investment Priorities: Infrastructure Over Experience

Institutional logic is now clearly visible in capital allocation.

Institutional Investment Priorities (Ranking)

Infrastructure ranked first, followed by compliance and regulation, then custody and security. User experience placed last for the second consecutive year, signaling a decisive shift away from consumer-driven experimentation toward system-level robustness.

Web3, once a dominant narrative, fell in perceived importance, overtaken by privacy, security, and regulated custody solutions.

8. Consolidation and the Return of Wall Street Playbooks

Executives across the industry increasingly acknowledge this new reality. Kraken CEO David Ripley remarked that crypto exchanges are becoming “indistinguishable from traditional finance,” openly viewing NYSE-style platforms as competitors. Binance CEO Richard Teng has similarly suggested that acquisitions by large exchange groups will accelerate.

This mirrors a familiar Wall Street pattern: absorb emerging competitors rather than be disrupted by them.

9. What This Means for Investors and Builders

For readers seeking new crypto assets, yield opportunities, or practical blockchain applications, the implications are profound:

- Alpha is shifting from retail speculation to infrastructure and market plumbing

- Regulatory alignment is no longer optional—it is a competitive advantage

- Tokenization and custody represent more durable long-term opportunities than consumer apps

Conclusion: A New Power Balance in Digital Assets

The retail-driven era of crypto innovation is not entirely over, but it is no longer dominant. Traditional finance has not merely adopted blockchain—it is actively redefining the digital asset landscape in its own image.

For builders, investors, and entrepreneurs, success in the next cycle will depend less on ideology and more on execution, compliance, and integration with global financial systems.

Crypto’s future is no longer outside the system. It is becoming part of it.