Key Takeaways :

- Tom Lee of BitMine warns that many digital asset treasury (DAT) companies are already trading below net asset value (NAV), marking a possible bursting of the “treasury bubble.”

- Ethereum-centric treasuries, led by BitMine, have pursued aggressive accumulation but now face compressed NAV premiums, stock dilution, and short-seller attacks.

- Bitcoin treasury firms are also seeing weaker inflows and falling mNAVs, weakening their capital-raising power.

- Fundamental vulnerabilities—reliance on premium valuations, dilution, lack of revenue, opaque auditing, and regulatory risk—are being exposed.

- The shakeout may separate long-term survivors (with disciplined corporate governance and clear utility) from speculative imitators.

- For those hunting new crypto opportunities, the collapse suggests caution in replicating treasury models and renewed interest in protocol-level innovation, tokenized real-world assets (RWA), and operational blockchain use cases.

1. Introduction: A Bubble in the Making?

Tom Lee, the new chairman of BitMine, recently asserted in a Fortune podcast that the bubble surrounding digital asset treasury companies may already have burst. He observed that many companies holding significant crypto reserves are now valued in the public markets below the net asset value (NAV) of their crypto holdings. Such a development would shatter one of the core tenets enabling the treasury model: that equity markets would afford a premium to such firms, enabling them to issue shares or debt at attractive rates to fund further accumulation.

This claim aligns with recent market data: some prominent crypto treasury stocks have suffered double- or triple-digit declines, NAV premiums have compressed, and capital inflows have slowed dramatically. The environment that looked like a new frontier in 2025 is now testing its fundamentals.

In what follows, I will (1) summarize the background and claims from the original article, (2) inject recent developments and data, (3) analyze the structural risks and failure modes of DATs, (4) map out potential outcomes and survivors, and (5) propose strategic implications for crypto investors and innovators going forward.

2. Summary of the Article: “Crypto-Treasury Bubble or Crash?”

2.1 The Rise of DATs

The original article describes a class of companies, referred to as Digital Asset Treasury (DAT) firms, which hold large quantities of cryptocurrencies (Bitcoin, Ethereum, Solana, etc.) and offer investors exposure to those assets via equities. This model was popularized when MicroStrategy’s Michael Saylor began accumulating Bitcoin in 2020, converting corporate balance sheets into crypto proxies.

Tom Lee, who recently became chairman of BitMine, is actively steering BitMine toward becoming a major holder of ETH. BitMine is reported to hold over 3 million ETH (about 2.5% of the total supply), and Lee has publicly voiced a goal of reaching 5%. Under Lee’s leadership, BitMine positions Ethereum as “Wall Street’s blockchain.”

2.2 Collapse Signals and mNAV / NAV Discount

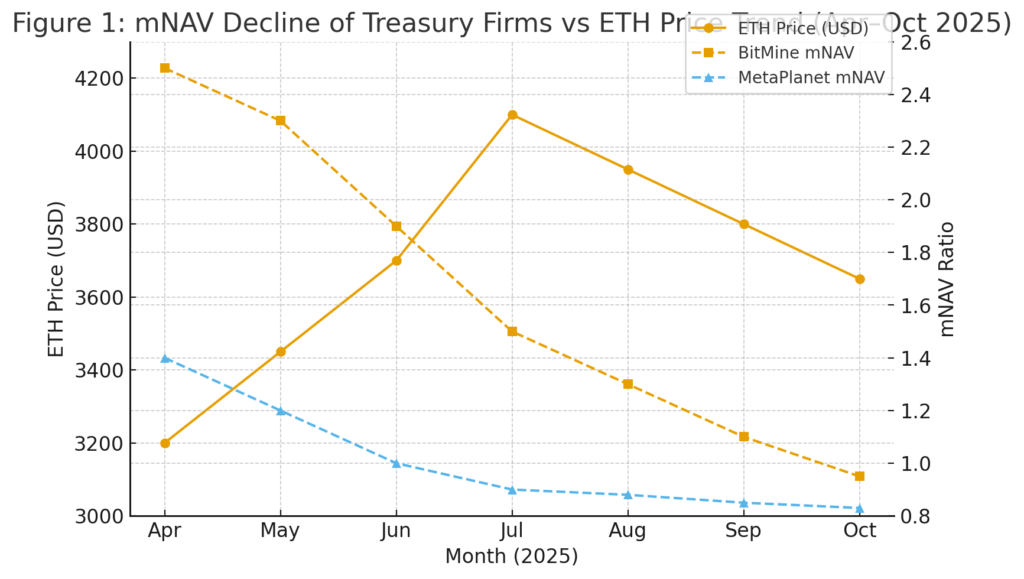

Lee warns that many DATs are now trading below their net asset value (NAV). In fact, in Japan, MetaPlanet recently became the first major player whose mNAV (i.e. market-adjusted NAV ratio) dropped below 1 (0.95), as the market started valuing the company at a discount to its token holdings. BitMine, by contrast, still maintained a high mNAV (11.1×) at the time of the original article.

An analyst, Mark Chadwick, interpreted the collapse in MetaPlanet’s rating as a sign of “bubble bursting” in crypto treasury stocks, though some more bullish voices view the decline as a buying opportunity.

2.3 The Warning: No Guarantee of Success

Despite the momentum behind the DAT model, Lee cautions that success is far from guaranteed. He notes that many firms—especially those holding altcoins—are already trading at discounts to their NAV, which undermines their ability to issue further shares or debt to expand holdings. This risk is especially acute for companies that rely on the assumption of perpetual investor willingness to pay a premium over NAV.

Thus, the article frames the situation as a speculative bubble, now under stress, with the potential for systemic distortions in how crypto-based equity models are pitched.

3. Recent Developments & Reinforcing Evidence

Since the publication of the original article, multiple corroborating signs and deeper analyses have emerged.

3.1 Worsening Stock Performance and Discounting

- DAT stock declines: BitMine (Ethereum treasury) has plunged ~67% from its high, while Strategy (Bitcoin treasury firm) has dropped ~30% over recent months.

- NAV premium compression: Ethereum treasury firms have seen their mNAVs dip below 1 in many cases—for example, SharpLink, The Ether Machine, and ETHZilla reporting values of 0.99, 0.07, and 0.88 respectively

- Crypto treasury capital raising slows: The pace of capital inflow into Bitcoin treasury firms has collapsed. Daily net inflows recently dropped to ~140 BTC—lowest levels since mid-June—down from summer peaks of over 8,000 BTC/day.

- MetaPlanet in freefall: MetaPlanet’s enterprise value now trades below its Bitcoin holdings, with its mNAV falling to 0.99. The share price has plunged ~70% from peak.

- Short-seller attacks: Kerrisdale Capital has shorted BitMine, criticizing the business model and noting that the firm’s rate of ETH-per-share accretion is slowing and share count is ballooning.

These developments deepen concern that the equity valuations behind DATs may not be sustainable.

3.2 Analytical and Structural Critiques

- “How DATs Die” framework: NYDIG published an analysis of failure modes, arguing that once a DAT cannot sustain a premium to NAV, the core growth mechanism (issuing equity to buy more crypto) breaks down.

- Forbes criticism: An article for Forbes notes that when DATs trade below NAV, their ability to raise fresh capital is undermined, particularly in volatile market conditions.

- Dot-com parallels: Some commentators compare the rise and possible collapse of crypto treasury companies to the dot-com mania of the late 1990s, warning of speculative overshoot and eventual shakeout.

- Regulatory & audit opacity: Concerns have also been raised about auditing practices for crypto treasuries—how reliably auditors can verify token holdings, custody, pledging, and the potential for manipulation.

- Overcrowding & dilution: The market is now saturated—data suggests over 200 companies have announced plans to go public or raise funds to accumulate crypto assets, collectively targeting ~$102 billion.

- Role reversal risk: Some firms may have to sell crypto or equity to meet obligations if token prices fall or investor confidence reverses.

3.3 Macro & Capital Market Context

- Weakening institutional demand: With inflows into treasury vehicles slowing, these firms lose a core source of support for crypto prices.

- Volatile crypto macro: ETH and BTC have seen recent corrections, reducing the cushion for treasury portfolios.

- Regulatory pressure: Global financial risk bodies (e.g. FSB) are raising concerns about regulatory gaps in crypto markets.

- Financial stability risks: Institutions like the IMF warn of overvalued asset markets and fragile linkages between regulated and unregulated sectors.

The broader market environment is thus tilting from exuberance toward stress.

4. Anatomy of the DAT Business Model & Failure Modes

To understand why many treasuries are under pressure, let’s break down their mechanics and fragilities.

4.1 The Core Model: NAV Premium → Capital Issuance → Accumulation Loop

The core assumption for DATs is that equity markets will value them at a premium to the NAV of their crypto holdings. This premium allows them to raise capital (issuing shares or debt) at favorable terms, then use that capital to purchase more crypto, thereby growing per-share holdings of crypto over time.

If the premium holds or expands, the cycle is virtuous. But the moment the premium compresses or reverses, the engine stalls.

4.2 Key Risks and Failure Mechanisms

- NAV Premium Compression

If the market loses faith and values the equity at a discount to NAV, the issuance of fresh shares becomes dilutive, not accretive. This can trigger downward spirals. - Share Dilution and Overissuance

To raise funds, many firms issue new shares aggressively. If token prices drop or new capital inflows weaken, dilution undermines investor value. For example, MetaPlanet’s share count ballooned multiple times within a year. - Volatility in Crypto Markets

Sharp declines in the underlying crypto assets can erode NAV dramatically, putting pressure on balance sheets and triggering margin calls or forced liquidations. - Lack of Operational Revenue

Many DATs have minimal business operations or revenue streams outside crypto holdings. They largely survive on market narrative and asset appreciation. - Audit and Custody Risks

Verifying ownership, preventing mismanagement or rehypothecation, and addressing custodian and wallet complexity adds opacity. Some smaller DATs provide weak disclosure, inviting skepticism. - Regulatory and Legal Risk

Regulatory scrutiny over securities issuance, disclosures, token classification, and market manipulation may constrain the free operation of these models in different jurisdictions. - Overcrowding and Capital Fatigue

With dozens or hundreds of firms all pursuing the same accumulation strategy, competition for capital intensifies, investor appetite may saturate, and marginal returns diminish. - Feedback Loops and Death Spiral Risk

If confidence collapses, selling pressure on shares depresses value, further discouraging capital flows, leading to more dilution or asset sales.

NYDIG frames this as a “premortem” scenario: once a DAT can no longer sustain premium pricing, it ceases to function as a growth engine.

5. Possible Scenarios and Survivors

Given the current stress, how might this space evolve? Below are plausible trajectories and characteristics of survivors.

5.1 Scenario A: Controlled Consolidation

In this scenario, weaker DATs are acquired or delisted; only a handful of well-managed ones survive. Survivors will likely share characteristics:

- Conservative issuance policies (only raising capital when premium is strong)

- Transparent and robust auditing and custody processes

- Operational revenue or ancillary business lines (e.g., lending, staking, derivatives)

- Low leverage and cautious risk management

- Strong governance and credible leadership

In this outcome, the sector contracts, but a more sustainable basis for treasury-style firms may emerge.

5.2 Scenario B: Broad Collapse and Reversion

If the wave of negative sentiment accelerates, many DATs may collapse or be forced to liquidate assets. Some could default on obligations or restructure. The broader crypto markets may suffer contagion, with investor risk appetite retrenching into core protocols and away from hybrid equity/crypto plays.

5.3 Scenario C: Hybrid Evolution to Protocol + Utility Focus

Another possibility is that DATs evolve into more utility-driven entities. Instead of purely holding tokens, they may integrate protocol-level operations—staking, validator functions, liquidity provision, tokenized real-world assets, or infrastructure services. Over time, their business models might shift from passive accumulation to active participation in blockchains.

5.4 Wildcard: Macro or Regulatory Tailwinds

In a favorable turn—crypto rallying sharply, regulatory clarity emerging, institutional flows re-accelerating—the DAT model could get a second wind. But such a rebound would likely favor the largest, most disciplined firms with credibility intact.

6. Strategic Implications for Crypto Investors and Builder

Given all of the above, here’s what people seeking new crypto opportunities should consider:

6.1 Be Very Cautious of “Copy-DAT” Strategies

The treasury model may now be overhyped. Replicating the playbook without differentiation or capital discipline is high risk. Many future DATs may end up as value traps.

6.2 Focus on Protocols with Real Utility

Investors may find better long-term upside in cryptographic infrastructure, DeFi protocols, layer-1 or layer-2 networks solving real problems (scaling, privacy, interoperability), rather than speculative equity proxies.

6.3 Tokenized Real-World Assets (RWA)

As crypto matures, tokenization of real assets (real estate, credit, commodities) will continue to attract interest. While liquidity is currently limited, the long-term thesis is compelling. (See academic work on RWA liquidity challenges.)

6.4 Hybrid Treasury + Utility Approaches

Some firms may blend treasury holdings with operational roles—staking, lending, infrastructure—to diversify revenue and reduce dependency on token price appreciation.

6.5 Embrace Transparency, Auditability, and Compliance

Given regulatory scrutiny and the trust issues exposed in DATs, projects and companies with strong disclosures, third-party audits, proof of reserves, and on-chain verifiability will likely gain favor.

6.6 Monitor Macro & Regulatory Signals

Macro shocks, interest rate shifts, regulatory action or clarifications can reignite or crush sentiment. Keep a watch on institutional flows, crypto-friendly jurisdictions, and government stances.

7. Conclusion: What We Learn from the Burst

The rise of digital asset treasury companies was a bold experiment: can capital markets reprice token exposure into equity? It rode on a powerful narrative—a new bridge between traditional finance and crypto. But like many narratives, it depended heavily on investor confidence, perpetual premium valuation, and market momentum.

The recent tumble in DAT stocks, narrowing of NAV premiums, drying capital inflows, and critiques of governance and auditing suggest that the bubble is indeed deflating. For many firms, the core growth engine may be broken.

Yet this unraveling is not necessarily the end of the story. Some survivors may emerge stronger—those combining disciplined capital strategy, transparency, operational value, and protocol-level contribution. For crypto investors and project builders, the shift suggests a renewed emphasis on fundamentals, utility, and sustainable revenue models.

If you’re searching for the “next big thing” in crypto, now may not be the time to pile into treasury proxies. Instead, look to infrastructure innovation, tokenization, DeFi primitives, and real-world asset bridges—spaces where value lies more in use than narrative.