Key takeaways:

- Harvard Management Company (HMC) disclosed ~$116.7 million in BlackRock’s iShares Bitcoin Trust (IBIT) as of June 30, 2025 (~1.9 million shares). The position was HMC’s 5th-largest disclosed holding in Q2 2025, behind Microsoft, Amazon, Booking Holdings, and Meta.

- IBIT has grown to ~$86.17 billion in net assets (as of Aug 8, 2025), cementing its lead among U.S. spot Bitcoin ETFs.

- Harvard also added ~$101.5 million in SPDR Gold Trust (GLD) in the same quarter, highlighting a barbell tilt toward digital gold (BTC) and physical gold.

- The SEC has moved to permit in-kind creations/redemptions for crypto ETPs and to raise position limits on certain Bitcoin ETP options up to 250,000 contracts, improving market plumbing and potentially deepening liquidity.

- Other universities are edging in: Brown University increased its IBIT stake to ~$13 million by Q2 2025, while earlier Wisconsin’s state pension fund exited a prior, large IBIT position—showing institutional positioning is active, not one-way.

- Harvard’s endowment stood at ~$53.2 billion in FY2024, the largest among U.S. universities—so even a sub-1% allocation in public filings is watched as a bellwether.

1) What Harvard disclosed—and why it matters

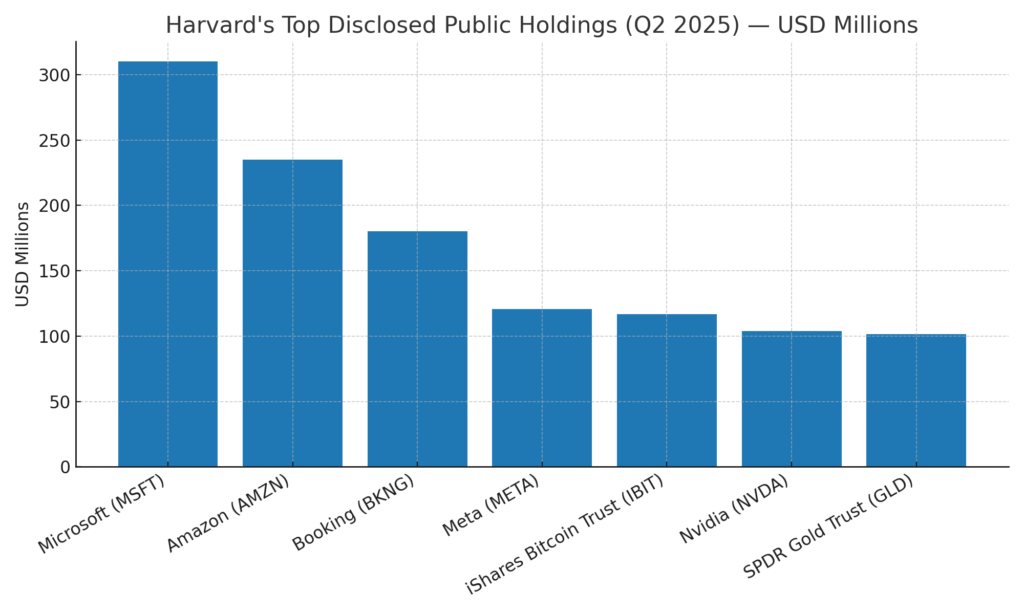

Harvard Management Company’s latest Form 13F shows an entry into BlackRock’s iShares Bitcoin Trust (IBIT) worth ~$116.7 million (about 1.9 million shares) at the June 30, 2025 snapshot. In Harvard’s disclosed public-equities sleeve, IBIT ranked fifth, trailing Microsoft, Amazon, Booking Holdings, and Meta. In the same filing, HMC also reported ~$101.5 million in SPDR Gold Trust (GLD)—a paired allocation to assets often framed as hedges against monetary debasement or macro shocks.

This is notable because Harvard’s filings are closely tracked for signals on how sophisticated pools of capital are adapting to new asset classes. Even modest percentage weights can influence peers’ due-diligence cycles, consultant memos, and investment committee agendas across the endowment, foundation, and pension world. The disclosure also validates the “ETF wrapper” as an operational path for institutions that prefer exchange-traded, custodied exposure over direct coin custody.

[Insert Figure 1 here: “Harvard’s Top Disclosed Public Holdings (Q2 2025)” ]

2) Structure tailwinds: liquidity, options, and in-kind mechanics

Since the January 2024 green light for 11 spot bitcoin ETFs, the U.S. has seen a rapid institutionalization of Bitcoin market structure. IBIT launched the same month and has since pulled in the lion’s share of flows.

In July 2025, the SEC advanced several market-plumbing improvements for crypto ETPs—most notably permitting in-kind creations/redemptions (reducing friction between ETF shares and underlying coins) and raising position limits on certain Bitcoin ETP options to as high as 250,000 contracts. These steps tend to tighten spreads, improve hedging, and draw in options market-makers, which can ultimately make the products more scalable for large institutions.

3) IBIT by the numbers

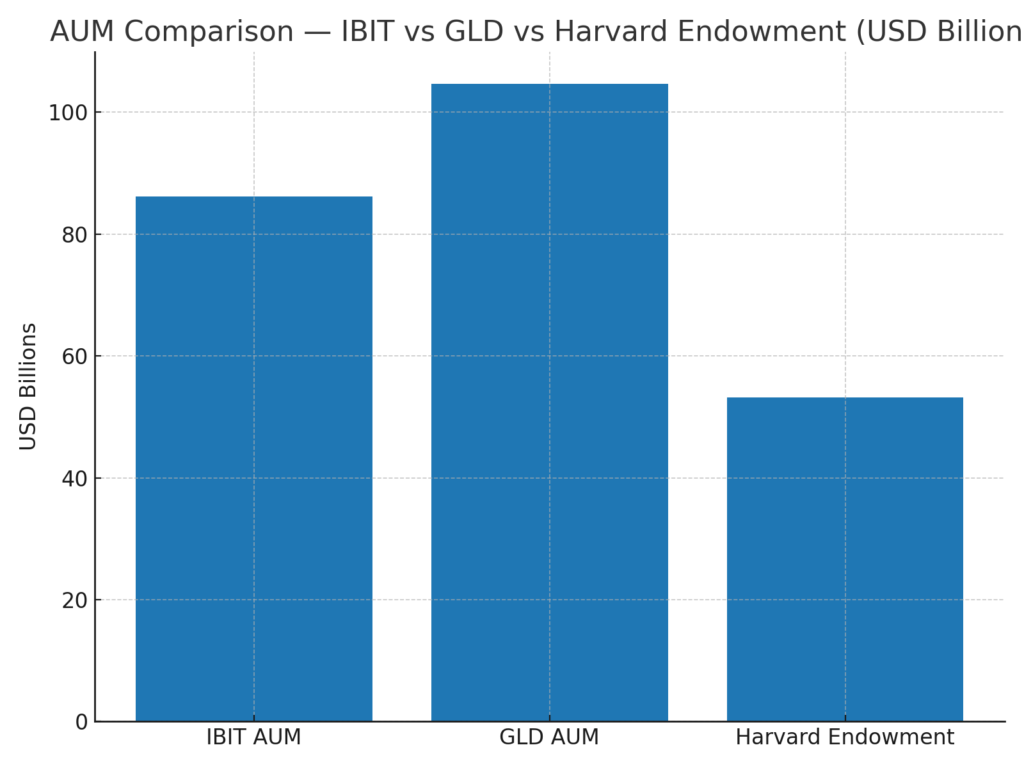

IBIT AUM reached ~$86.17 billion on Aug 8, 2025, reflecting both price appreciation and massive net inflows. That scale matters for allocators who prioritize depth, tight spreads, high turnover, and robust primary/secondary market functioning.

To contextualize size, compare: GLD sits at ~$104.7 billion AUM; Harvard’s endowment is ~$53.2 billion (FY2024). A decade ago, comparing a Bitcoin ETF side-by-side with the flagship gold ETF or the largest university endowment would have sounded far-fetched. Today, it’s just another bar chart.

[Insert Figure 2 here: “AUM Comparison — IBIT vs GLD vs Harvard Endowment (USD Billions)”]

4) Endowment context: risk, diversification, and signaling

Endowments have long-duration liabilities and seek equity-like real returns while diversifying tail risks. In this frame, Bitcoin via ETF can be evaluated as a high-beta, macro-sensitive growth asset with low structural correlation to some traditional sleeves over multi-year windows—albeit with very high volatility and episodic drawdowns. Harvard’s move aligns with a measured, optionality-seeking approach: a position large enough to matter but small enough not to dominate risk budgets in a $53B pool.

HMC’s public filing also shows meaningful positions in Microsoft (~$310M), Amazon (~$235M), Booking (~$180M), and Meta (~$120.5M), suggesting a barbell of tech growth plus “digital/physical gold” hedges (IBIT and GLD).

5) Are universities really coming in? A cautious but visible “yes”

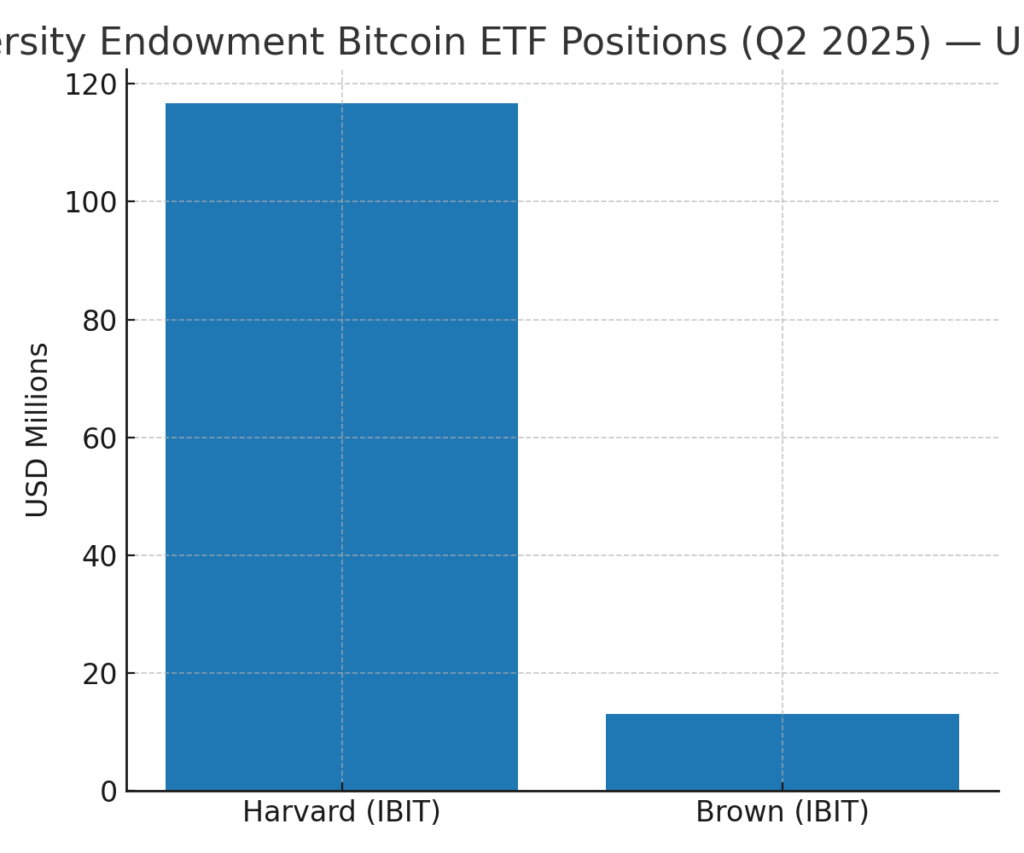

Harvard isn’t alone. Brown University disclosed an IBIT position in Q1 2025 and roughly doubled it to ~$13 million by Q2. At the same time, the State of Wisconsin Investment Board (SWIB)—an early, headline-grabbing adopter—fully exited a large IBIT stake by mid-May 2025. The message is not “everyone’s buying,” but rather that Bitcoin exposure is now part of the mainstream institutional toolkit, to be sized up or down like any other macro-sensitive asset.

[Insert Figure 3 here: “University Endowment Bitcoin ETF Positions (Q2 2025)”]

6) What this means for allocators and crypto-native builders

For allocators:

- Wrapper risk is declining. With SEC permissioning in-kind flows and higher options position limits, ETF plumbing is more robust, reducing basis/flow distortions and improving hedging.

- Scale enables strategies. At $86B+, IBIT supports block trading, derivatives overlays, and programmatic rebalancing without undue footprint.

- Peer benchmarking has started. With Harvard and Brown visible in filings, investment committees can calibrate sizing and policy language (e.g., “digital assets via regulated ETPs”).

For crypto-native builders:

- Institutional demand migrates to “ETF-friendly” infrastructure. Liquidity, qualified custody, market data, surveillance, and auditable processes become decisive.

- Second-order opportunities (execution, treasury, tax/ops, analytics, risk overlays) are ripe for SaaS-like productization aimed at RIAs, OCIOs, and treasury teams onboarding spot BTC ETPs.

7) How to evaluate spot Bitcoin ETFs (a quick checklist)

- Net expense ratio and implied trading cost (spreads, depth). Fee differentials compound; spreads matter for rebalance-heavy strategies.

- AUM and volume as proxies for depth and resilience during stress. IBIT’s scale currently leads, a non-trivial advantage for block liquidity.

- Creation/redemption mode (in-kind vs in-cash) and AP network breadth—now improving under the SEC’s July 2025 actions.

- Custody concentration (several ETFs use the same major custodians); assess operational and legal safeguards.

- Options availability and limits for overlays/hedging—now rising for certain BTC ETPs to 250,000 contracts, enabling more sophisticated risk management.

8) Risks to monitor

- Volatility and path risk. Bitcoin’s drawdowns can be severe; allocation sizing and rebalancing rules are critical.

- Policy/regulatory drift. The SEC’s posture has evolved since Jan 2024 approvals, but political cycles can alter priorities.

- Liquidity in stress. Even with in-kind functionality and big AUM, spreads can widen in shocks; governance and trading playbooks matter.

- Correlation spikes. During cross-asset selloffs, defensive assumptions can break; test the whole-portfolio behavior, not just standalone metrics.

- Custody/operational concentration. Shared service providers across ETFs introduce common-mode risk; diversify where feasible.

9) Outlook: from one asset to a platform

The SEC is also soliciting applications that would list mixed spot bitcoin and spot ether ETPs, and it has moved toward a merit-neutral stance on crypto-based products—opening the door to a broader design space and continued instrumentation (options, FLEX). If this trend persists, the ETF wrapper becomes a durable bridge between crypto’s native rails and institutional allocators’ workflows.

For now, Harvard’s entry is best read as pragmatic optionality: a high-liquidity, regulated vehicle that can be sized up or down as the macro and policy mosaic shifts. Whether other endowments follow at scale will depend on price discovery, governance comfort, and how crypto ETFs compete for scarce risk budget against private equity, venture, and real-asset opportunities.

Conclusion

Harvard’s $116.7 million in IBIT doesn’t rewrite endowment playbooks overnight, but it normalizes Bitcoin exposure inside the most conservative corners of institutional portfolios. Paired with a renewed GLD stake, it frames a digital/physical store-of-value barbell inside a tech-heavy public sleeve. With IBIT at $86B+ AUM, GLD above $100B AUM, and the SEC improving ETF plumbing—liquidity, options limits, in-kind mechanics—the infrastructure is now robust enough for large pools of capital to engage on their own terms. For crypto builders and allocators alike, the message is simple: the ETF era is now the on-ramp, and its rails are getting stronger by the quarter.