Main Points :

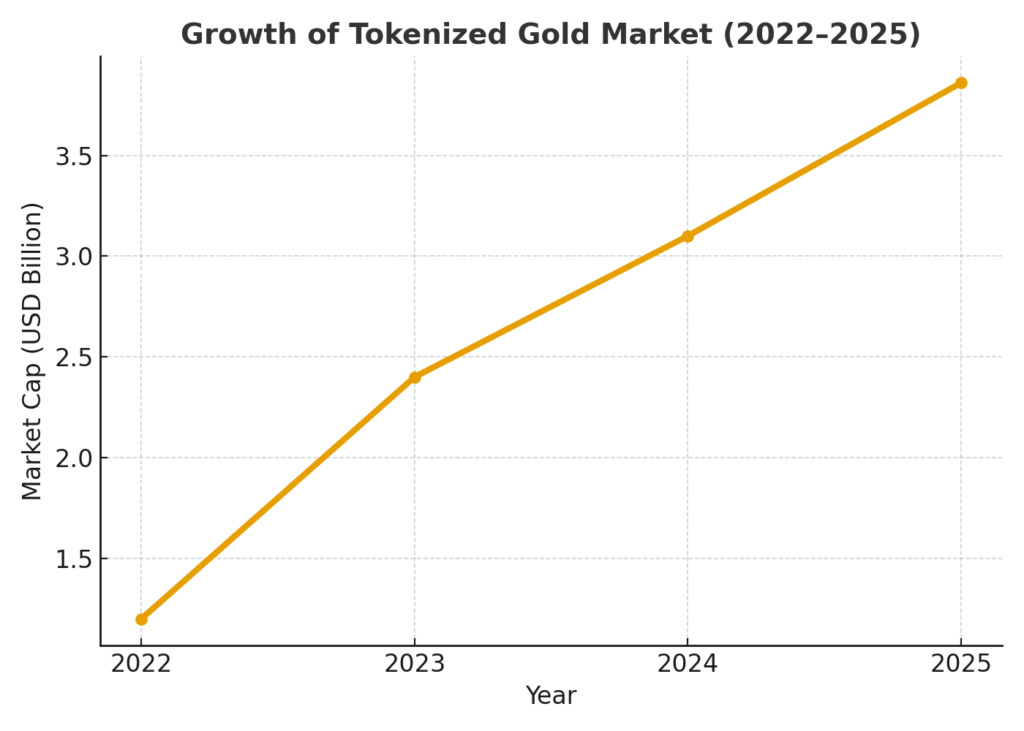

- The market for tokenised gold assets has swollen to around US $3.86 billion, led by tokens such as Tether Gold (XAUT) and PAX Gold (PAXG).

- Changpeng Zhao (CZ), co-founder of Binance, criticises them as fundamentally dependent on third-party trust — calling them “trust-me-bro” tokens rather than true on-chain assets.

- The comparison with stablecoins is drawn: gold-tokenised assets face similar risks around redemption, custody, audit and peg solidity.

- Despite the metal price rally (gold near ~US $4,100/oz) supporting interest, tokenised gold assets remain a small niche compared to much larger stablecoin markets.

- Broader context: the real-world asset (RWA) tokenisation trend is growing, but liquidity and custodial infrastructure remain major bottlenecks.

1: Market expansion of gold-tokenised assets

In recent months the tokenised-gold segment of the crypto ecosystem has drawn notable attention. Data from CoinGecko show the aggregate market capitalisation of tokens pegged to the underlying metal climbing to approximately US $3.86 billion. Leading the segment are Tether Gold (XAUT) and PAX Gold (PAXG), with XAUT alone accounting for billions in market cap.

The logic driving this growth: gold has once more entered a bullish phase, with spot prices hovering around US $4,100 per ounce. For crypto practitioners seeking new asset vectors, gold-backed tokens appear to offer a kind of hybrid: traditional real-world commodity value plus blockchain transferability.

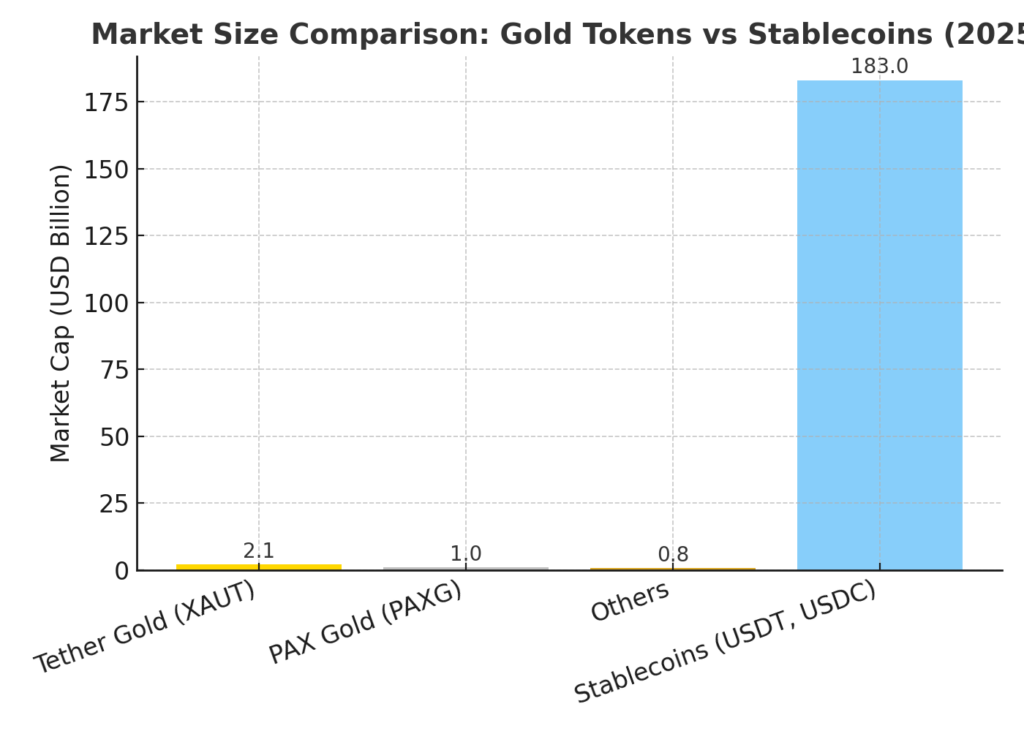

Consequently, these tokens are being pitched as alternative hedges, possibly more accessible than physical gold bullion for everyday crypto users. However, the relative size of the market remains tiny when contrasted with major stablecoins: for example, one article cites that even XAUT’s market cap is just US $2.1 billion versus USDT’s ~US $183 billion.

For someone interested in exploring new crypto assets or alternative revenue streams via blockchain/real-world asset bridges, this niche certainly merits attention. Yet the rapid growth also raises questions about where the value and risk lie.

2: CZ’s critique — why this isn’t “on-chain gold”

The most provocative voice in the debate is Changpeng Zhao (CZ), who argues that tokenised gold doesn’t achieve true on-chain ownership of gold — rather, it substitutes one layer of trust for another. On the social platform X, he wrote:

“Tokenizing gold is NOT ‘on chain’ gold. It’s tokenizing that you trust some third party will give you gold at some later date, even after their management changes, maybe decades later, during a war, etc.”

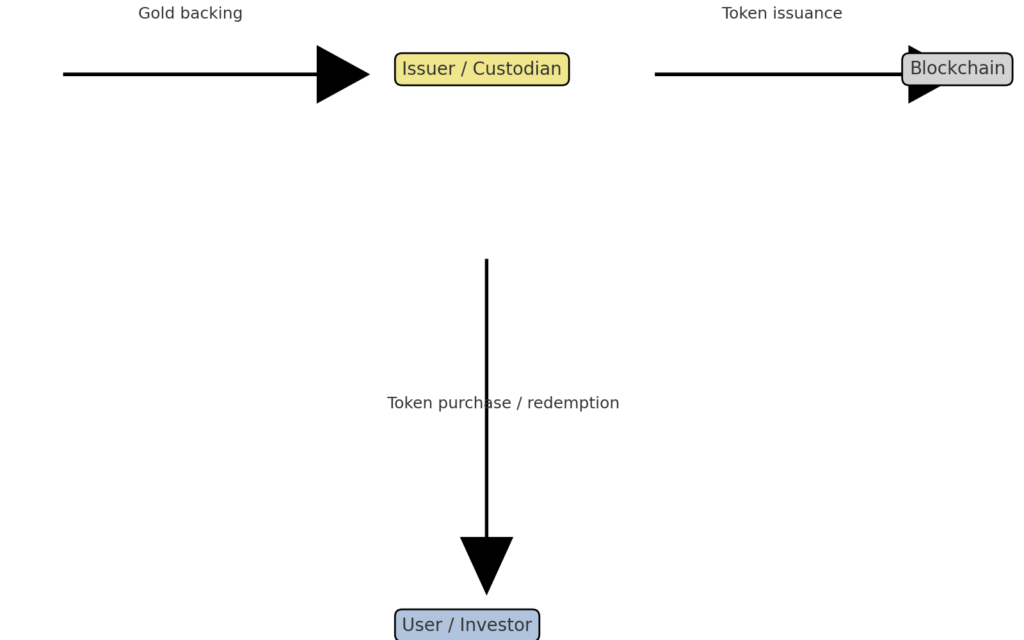

In his framing, the architecture of gold-tokenisation remains custodial: an issuer holds the vaulted metal, issues a token to the user, and (in principle) allows redemption. But at the end of the day, the user is trusting the issuer and custodian rather than engaging in fully decentralised self-custody of the physical asset. The key risk, CZ argues, lies in “will they deliver the gold when I ask for it — especially if the issuer’s governance changes, regulation shifts, or extreme macro events intervene?”

He furthermore calls such assets “‘trust-me-bro’ tokens,” implicitly contrasting them with purely on-chain native assets (like Bitcoin) that require no centralised custodian.

From the perspective of crypto investors seeking autonomy, programmability, and trust-minimisation, this critique hits at the heart of what many consider the unique value of blockchain-based assets.

3: Parallels with stablecoins and redemption risk

One striking dimension is the analogy drawn between tokenised-gold assets and fiat-pegged stablecoins. A report from NYDIG (quoted in coverage) emphasises that even well-established dollar-pegged tokens such as USD Coin (USDC) or Tether (USDT) carry embedded redemption risk or “peg risk” under extreme market stress.

Similarly, tokenised gold depends on the issuer’s integrity, ability to redeem physical metal, and the logistical/external exposure of vaults and custodians. If redemption rights become illiquid, if auditing transparency falls short, or if the issuer faces insolvency, the token could diverge from its promised asset-backing.

For the typical crypto audience—those looking for new assets, yield-opportunities, or blockchain-based utilitarian use-cases—the implication is clear: adopting tokenised gold is not the same as owning physical bullion or a native crypto asset. The liquidity and redemption mechanics matter as much as the surface link to gold.

4: Real-world asset (RWA) tokenisation context & liquidity challenges

Zooming out, tokenised gold sits within the broader category of “real-world asset” (RWA) tokenisation: bringing physical, off-chain assets onto blockchains as digital tokens. Recent academic work (e.g., Rischan Mafrur’s August 2025 study) estimates over US $25 billion of RWAs on chain as of 2025—but emphasises that trading activity, liquidity, and investor participation remain limited.

In that study, structural barriers such as custodial concentration, whitelisting, valuation opacity, regulatory gating and lack of decentralised trading venues are flagged as key reasons why many tokenised assets haven’t yet achieved vibrant secondary markets.

Applying that to tokenised gold: though of decent size in absolute terms (~US $3.8–4 billion) the sector remains relatively small, fragmented, and subject to logistic/bespoke custody constraints. For investors or developers engaged in blockchain infrastructure (such as your interest in wallets, swaps, tokenisation, etc.), this means the terrain is still somewhat early stage — possibilities for innovation (e.g., better redemption mechanisms, decentralised vault transparency, programmable gold yields) exist, but so do considerable logistical/regulatory risks.

5: Implications for investors and blockchain practitioners

From the vantage point of someone seeking new crypto assets, revenue opportunities or practical blockchain uses, what are the takeaways?

- Opportunity for diversification – Tokenised gold offers a novel bridge between commodity value and digital token infrastructure. Investors seeking to hedge crypto risk or blend yield/inflation protection might consider it.

- Custody and redemption risk matter – Unlike native assets which rely purely on on-chain code/trustless settlement, tokenised gold introduces off-chain dependencies. If an issuer mismanages or an audit fails, token value could diverge from physical backing. CZ’s critique serves as a strong caution.

- Liquidity and secondary market depth are limited – As the RWA literature suggests, tokenised real-world assets often have low turnover, limited trading venues, and thus may carry illiquidity premiums or execution risk.

- Blockchain‐native innovations possible – For developers (like yourself) designing wallets, swap mechanisms or token flows, the tokenised gold class presents use-cases: e.g., integration of gold-token on-chain within DeFi pools, programmable dividends based on vault yields, swap rails between tokenised gold and stablecoins, even fractional ownership models. But these must be built with transparency (e.g., proof of reserves, auditability, redemption pathways) to address the trust critique.

- Regulatory and institutional considerations – Given custodial and asset-backed nature, tokenised gold may intersect with securities regulation, commodities law, vault regulation, anti-money-laundering (AML) rules and token redemption rights. For your interest in EMI/VASP frameworks, any project linking tokenised commodities must pay special attention to these layers.

Conclusion

The rise of tokenised gold assets—now approaching roughly US $3.8–4 billion in market cap—marks an interesting frontier in crypto: blending real-world commodity value with blockchain’s transferability. For investors and blockchain builders alike this offers both opportunity and caution. As you seek new crypto assets or practical blockchain uses, tokenised gold is worth watching—but it is not a transparent plug-and-play alternative to owning physical gold or fully on-chain native tokens.

Changpeng Zhao’s critique that these tokens remain “trust-me-bro” promises is a useful red flag: the essence of decentralised value lies not just in tokenising a commodity, but in removing custodial, counterparty and redemption risk. For builders, this suggests that successful innovation in this space may hinge on coupling tokenised assets with robust redemption processes, open audits, decentralised settlement and regulatory clarity.

In short: tokenised gold is not a simple “gold on chain” substitute. It’s a new hybrid asset class—one where blockchain and commodities meet—but also one where old-world trust remains embedded. If your goal is to uncover new crypto assets with upside and embrace blockchain’s utility, then consider tokenised gold as part of your palette—but treat it with the same governance, custody and liquidity scrutiny as any ambitious token project.