Main Points :

- PNC has partnered with Coinbase to let wealth and asset‑management clients trade crypto directly from their bank relationship, while also providing banking services to Coinbase.

- Demand to view and manage crypto alongside traditional assets is now explicit at major brokerages like Charles Schwab, which is preparing Bitcoin/Ether trading.

- Wall Street banks, including JPMorgan, Goldman Sachs, Citi, BofA, and Morgan Stanley, are openly discussing stablecoins and deposit tokens on earnings calls—reflecting a shift from skepticism to cautious engagement.

- Standard Chartered just launched BTC/ETH spot trading for institutions, underscoring a global race to serve crypto order flow.

- For builders and yield seekers: opportunities lie in bank-grade custody rails (MPC/TEE), stablecoin settlement layers, tokenized cash equivalents, and treasury-integration APIs.

1. The Deal That Says “Crypto Is Just Another Asset Class”

PNC Financial Services Group’s tie-up with Coinbase is not a marketing one-off—it’s an operational handshake. The Pittsburgh-based bank will start by enabling its wealth and asset‑management clients to buy, sell, and hold crypto through PNC, while PNC simultaneously extends select treasury and settlement services to Coinbase. Emma Loftus, PNC’s head of treasury management, framed it as an early‑stage rollout shaped by client demand to see crypto and fiat side by side.

This dual flow—clients accessing crypto, Coinbase accessing banking—is significant. It shows that large U.S. banks will not only tolerate crypto exchanges; they’ll bank them, provided compliance boxes are ticked. That sets a template for other regional and super‑regional banks seeking fee growth without building a crypto stack from scratch.

2. Why Now? The Interface Problem and a Regulatory Turn

Clients have been vocal: they want a single pane of glass for portfolios. Charles Schwab’s CEO Rick Wurster said clients want crypto “next to their stocks and bonds,” and Schwab plans to “absolutely” compete with Coinbase.

Regulation also tilted. Deutsche Bank analysts recently called out five structural shifts supporting Bitcoin’s institutionalization—legislation (GENIUS Act, Clarity Act), ETF inflows, corporate treasuries adding BTC, and infrastructure by State Street/BNY Mellon. Major banks now discuss stablecoins in earnings calls instead of dodging the topic—JPMorgan’s Jamie Dimon admitted work on both deposit tokens and stablecoins.

3. Stablecoins Move From Threat to Tool

Bank CEOs once dismissed stablecoins as “wild west” products. Today they are positioning to issue or integrate them. Business Insider reported that five of the six largest U.S. banks mentioned stablecoins this quarter. Dimon sees them as a potential threat to bank payment dominance—hence the need to build alternatives.

PNC’s CEO William Demchak expects large-scale stablecoin initiatives to be consortium-led; PNC wants a seat at that table. That aligns with how banks historically de-risk novel rails—via shared utilities (think Zelle, The Clearing House RTP).

4. The Global Context: Standard Chartered, Zodia, and Asia’s Retail Pipes

Standard Chartered just launched spot BTC/ETH trading for institutions, augmenting its Zodia Markets/Custody stack. In Asia, UP Fintech (“Tiger Brokers”) already lets retail deposit/withdraw BTC/ETH and professionals move USDT. The gap between “crypto-native” and “bank-native” rails is narrowing on every continent.

5. Infrastructure: Custody and MPC as the Hidden Moat

Banks care about operational risk. Safeheron notes that MPC and Trusted Execution Environments are becoming standard in custody stacks. Builders offering white-labeled MPC wallets, policy engines, and auditor-friendly key ceremonies can sell into both banks and fintechs. For readers hunting revenue: packaging compliance-ready MPC + travel-rule integrations is a high-value niche.

6. Tokenized Cash Equivalents and On-Chain Treasuries

If you manage treasury for a Web3 business, your “cash” increasingly lives as USDC/USDT or bank-issued tokens. Banks are studying how to wrap short-term treasuries or insured deposits into programmable tokens that settle 24/7. Citi Token Services is live for cross-border B2B. That opens a play for yield platforms to ladder T‑bills on-chain, or for fintechs to embed sweep accounts that auto-migrate idle balances into tokenized MMFs.

7. Opportunities for Builders & Yield Hunters

a. API Layers for Treasury & Compliance

Banks will need clean interfaces: FX conversion, tax lots, statements, and AML checks for crypto. Vendors who can plug Coinbase’s order flow into bank cores (FIS, Fiserv, Jack Henry) and spit out GAAP-compliant reports win.

b. Stablecoin Settlement Hubs

If bank consortia launch “regulated stablecoins,” merchants and corporates will need routers that choose the cheapest, fastest rail (USDC vs. JPM coin vs. PNC consortium coin). Smart order routing for payments is a greenfield.

c. Cross-Chain Custody & Yield

Institutions want Bitcoin yield without CeFi blowups. That points to delta‑neutral basis trades, tokenized T‑bills, and staking governance tokens from “bank-grade” validators. Your product should surface real-time risk metrics and on/off-ramp tools.

d. Data & Analytics: One Pane of Glass

Schwab’s and PNC’s moves show UX is king. Dashboards that aggregate CeFi, DeFi, RWAs, and bank data—plus automate tax treatment—have strong PMF. Tie in alerts (e.g., when BTC volatility spikes or stablecoin yields drop) and you become indispensable middleware.

8. Risks and Constraints

- Regulatory Drift: GENIUS/Clarity Acts may evolve; state-level regimes (NYDFS vs. Texas) still diverge. Builders must design flexible compliance modules.

- Liquidity Fragmentation: Multiple bank stablecoins could fragment liquidity unless interoperability standards (e.g., ISO 20022 on-chain variants) emerge.

- Custody Liability: MPC reduces single-point failure but complicates audit trails; insurers will demand strict SLAs.

9. What This Means for You (Action Steps)

- Integrate Bank Rails Early: If you’re building a wallet/exchange, prepare for bank APIs (KYC, AML, statements). The PNC–Coinbase model may replicate across second-tier banks.

- Offer Stablecoin Optionality: Support multiple tokens and auto-route to the best fee/latency profile; log compliance data for each hop.

- Tokenize Treasury Ops: Package short-term yield (T-bills, repos) into on-chain wrappers with transparent NAV, daily attestations, and redemptions.

- Build UX for Consolidation: Provide APIs/widgets for RIAs and banks to embed crypto next to tradfi statements.

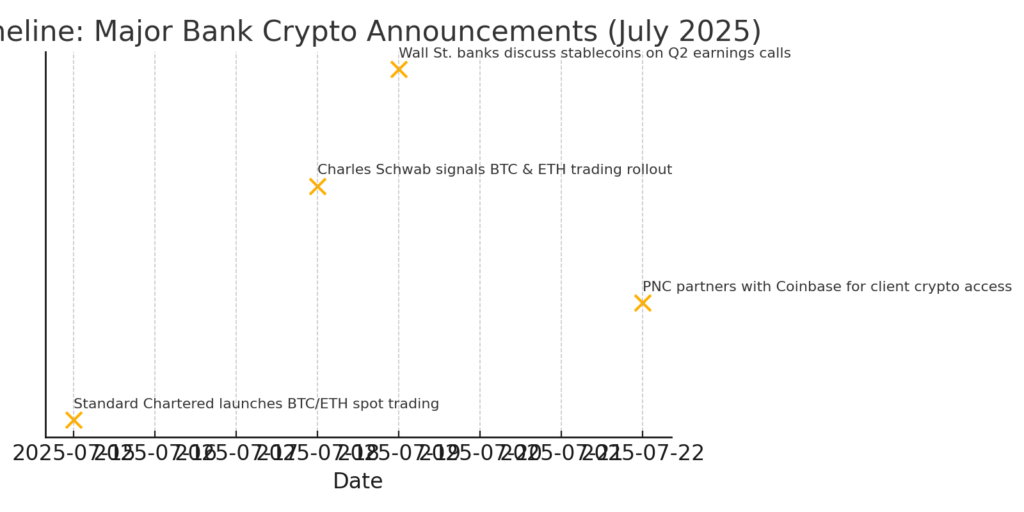

10. Visualizing the Shift

“Timeline: Major Bank Crypto Announcements (July 2025)”

The July cluster—Standard Chartered (July 15), Schwab (July 18), Wall Street stablecoin chatter (July 19), PNC–Coinbase (July 22)—maps an inflection.

Conclusion

PNC’s partnership with Coinbase crystallizes a new normal: banks no longer treat crypto as an external curiosity but as a product vertical to be integrated, risk‑managed, and monetized. Demand for unified dashboards drove this; regulatory clarity and ETF flows enabled it; competition (Schwab, Standard Chartered, JPMorgan) accelerates it. For entrepreneurs and investors, the next wave isn’t just “buy Bitcoin”—it’s building the pipes, dashboards, and tokenized cash instruments that make crypto feel like checking your bank balance. Those who provide compliant, bank-grade infrastructure—while still delivering yield and composability—stand to capture the fattest margins in this convergence.