Main Points :

- In 2025, cryptocurrencies—especially stablecoins—completed their transition from speculative assets to practical payment infrastructure.

- Regulatory clarity in the US, EU, and Asia enabled banks, asset managers, and payment networks to adopt digital assets at scale.

- Stablecoin circulation backed by the US dollar grew by approximately 50% year-on-year, driven by real economic use cases.

- Integrations between traditional payment giants and Web3 infrastructure providers, such as Mastercard and MoonPay, lowered friction for everyday crypto payments.

- Stablecoins are now central to cross-border settlements, gig economy payouts, B2B transactions, and programmable finance.

1. 2025: The Year Crypto Payments Became “Normal”

For more than a decade, cryptocurrencies were primarily associated with volatility, speculation, and short-term trading strategies. Bitcoin and Ethereum dominated headlines for their price swings rather than their practical utility. However, 2025 marked a decisive shift.

According to an analysis by Mastercard, digital assets achieved a new level of trust and reliability, allowing them to solve long-standing challenges in the financial industry. What changed was not only technology, but the surrounding ecosystem: regulation, institutional participation, and user experience matured simultaneously.

Comprehensive regulatory frameworks introduced across the United States, the European Union, and major Asian economies reduced uncertainty. This clarity gave banks, asset managers, and payment processors the confidence to integrate blockchain-based value transfer into their existing systems. As a result, crypto assets began to function less as speculative instruments and more as financial infrastructure—handling remittances, merchant payments, and corporate settlements.

2. Why Stablecoins Became the Core of Crypto Payments

Among all digital assets, stablecoins emerged as the most important bridge between traditional finance and blockchain networks. Pegged to fiat currencies—primarily the US dollar—stablecoins eliminated the price volatility that made earlier crypto payment experiments impractical.

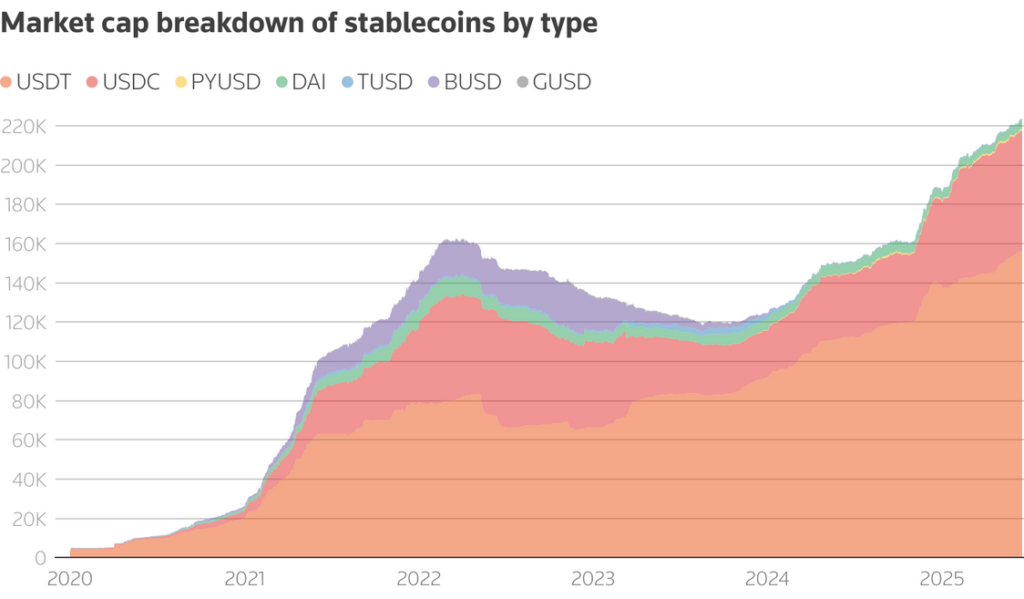

In 2025 alone, the total circulation of US dollar–backed stablecoins increased by roughly 50%, reflecting growing confidence from both users and institutions. This growth was not driven by speculative trading, but by real demand:

- Merchants seeking instant settlement without chargeback risk

- Companies optimizing cross-border treasury flows

- Freelancers and gig workers receiving faster, lower-cost payments

Stablecoins enabled predictable accounting, transparent pricing, and immediate finality—features essential for real economic activity.

[Stablecoin Market Growth]

Suggested chart: A line graph showing total stablecoin supply (USD) from 2021–2025, highlighting the sharp increase in 2024–2025.

3. Mastercard × MoonPay: Bridging Crypto and Daily Life

One of the most symbolic developments in 2025 was the collaboration between Mastercard and MoonPay, a major provider of Web3 on- and off-ramp infrastructure.

Together, they introduced wallet-linked payment cards that allow users to spend stablecoins seamlessly at everyday merchants. From the consumer’s perspective, the experience feels identical to using a traditional debit or credit card. Behind the scenes, however, stablecoins are converted and settled through blockchain networks, while leveraging Mastercard’s global acceptance and fraud protection systems.

This integration effectively erased the boundary between crypto assets and fiat money. Users no longer need to “cash out” manually or navigate complex exchanges. Their digital assets simply work—at supermarkets, online stores, and subscription services.

Mastercard’s analysis emphasized that user experience, not ideology, is the key to mass adoption. When blockchain complexity disappears behind familiar interfaces, crypto payments can finally scale.

4. Regulation as an Enabler, Not an Obstacle

Contrary to early crypto narratives, regulation did not suppress innovation in 2025—it accelerated it. Clear rules regarding custody, reserve backing, consumer protection, and anti-money laundering transformed stablecoins into compliant financial instruments.

In the US, Europe, and Asia, regulators converged on a shared principle: stablecoins must be transparent, fully backed, and interoperable with existing financial systems. This approach encouraged large institutions to enter the market without reputational or legal risk.

Banks began offering stablecoin-based settlement accounts. Asset managers integrated tokenized cash equivalents into portfolios. Payment processors embedded blockchain rails beneath traditional interfaces. Rather than replacing the financial system, stablecoins extended it.

5. Real-World Use Cases Driving Stablecoin Demand

The strongest evidence that crypto payments have matured lies in their use cases:

Cross-Border Payments

Traditional international transfers often take days and incur high fees. Stablecoins reduced settlement times to minutes and costs to a fraction of legacy systems, making them ideal for global commerce.

Gig Economy and Freelance Payments

Global freelancers increasingly prefer stablecoins for predictable, near-instant compensation without intermediaries. Payments denominated in USD-backed tokens protect earnings from local currency volatility.

B2B and Treasury Operations

Corporations use stablecoins for intercompany transfers, liquidity management, and automated settlements through smart contracts—reducing operational friction and reconciliation costs.

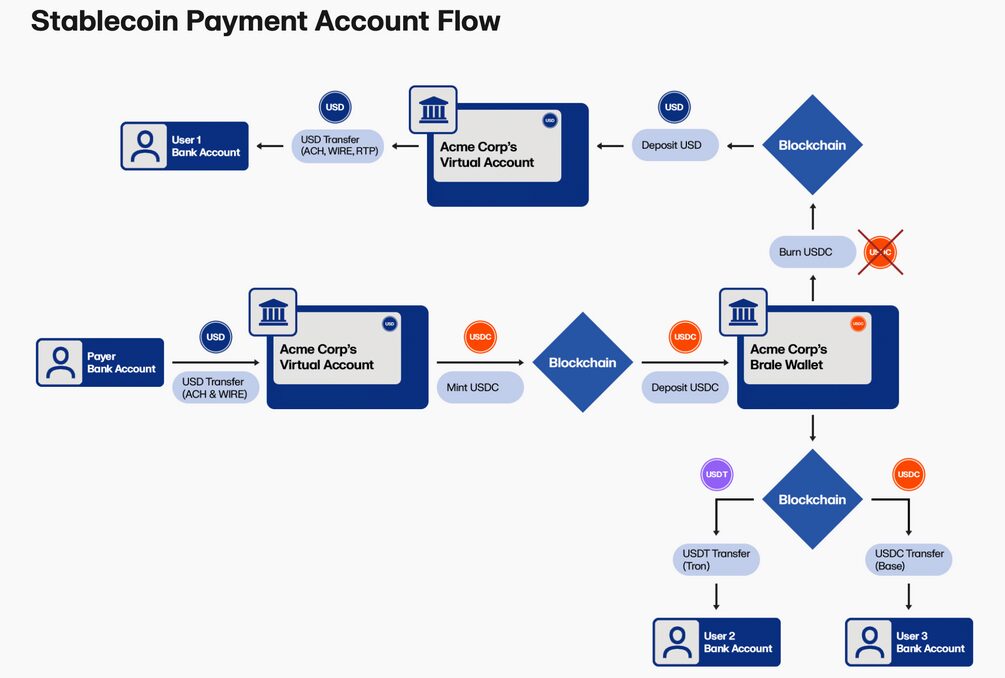

[Stablecoin Payment Use Cases]

Suggested diagram: Flowchart showing stablecoins used in cross-border payments, gig payouts, and B2B settlements.

6. Programmable Money and Smart Contracts

Beyond payments, stablecoins unlocked the concept of programmable money. Through smart contracts, funds can be released automatically when predefined conditions are met—delivery confirmation, service completion, or regulatory approval.

This capability transformed stablecoins into more than digital cash. They became financial building blocks for decentralized applications, automated compliance, and real-time financial reporting. For businesses, this meant lower overhead and higher transparency.

7. From “Crypto Economy” to Digital Financial Infrastructure

By the end of 2025, the narrative around crypto fundamentally changed. The industry stopped asking whether cryptocurrencies would replace traditional finance. Instead, the question became how blockchain-based assets could integrate and enhance existing systems.

Stablecoins emerged as the decisive answer. They preserved the familiarity of fiat currencies while delivering the efficiency of blockchain networks. As Mastercard concluded, when stablecoins are embedded within trusted payment rails and protection systems, they move from niche innovation to global infrastructure.

Conclusion: Stablecoins as the Foundation of the Next Financial Era

The transition from speculation to real-world utility did not happen overnight, but 2025 marked its completion. Stablecoins proved that digital assets can function as reliable, scalable, and compliant tools for everyday economic activity.

For investors, operators, and developers seeking the next growth phase of blockchain adoption, the message is clear: the future lies not in volatility, but in infrastructure. Stablecoins are no longer just part of the crypto ecosystem—they are becoming the connective tissue of global finance.