Main Points :

- The crypto industry is projected to transition from speculative trading toward becoming a core infrastructure layer of the internet by 2026.

- Stablecoins are expected to function as a global settlement layer, effectively turning the internet into a programmable banking system.

- AI agents may emerge as autonomous economic actors, requiring new identity frameworks such as “Know Your Agent (KYA).”

- Privacy, security, and trust will be redefined through cryptographic design, zero-knowledge technologies, and economic incentives.

- Regulatory clarity, particularly in the United States, could unlock long-term capital formation and sustainable network growth.

Introduction: Why 2026 Matters for Crypto

In early 2026, the crypto industry stands at a decisive crossroads. After more than a decade of rapid innovation, speculative booms, and painful market corrections, the question is no longer whether blockchain technology will survive, but what role it will ultimately play in the global digital economy.

According to a newly published industry outlook by Andreessen Horowitz (a16z), the coming years will mark a structural transformation. Crypto, in this vision, is no longer primarily about tokens, price charts, or short-term yield opportunities. Instead, it is evolving into the core infrastructure of the internet, tightly interwoven with artificial intelligence, finance, identity, and media.

This article expands on a16z’s projections for 2026, contextualizing them within recent market trends and practical blockchain use cases. The goal is not merely to summarize the report, but to translate its implications into insights that matter for investors, builders, and institutions searching for the next sustainable source of value creation.

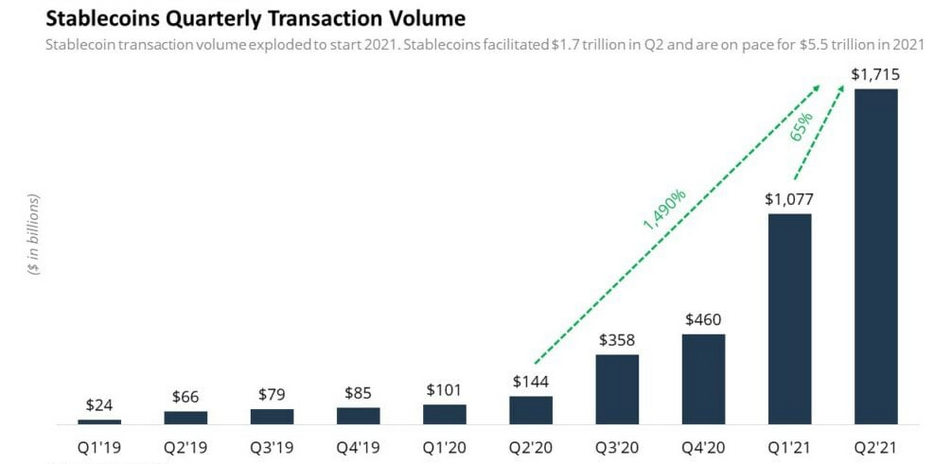

1. Stablecoins and the “Banking of the Internet”

One of the most striking data points highlighted by a16z is the scale of stablecoin usage. In the past year alone, stablecoin transaction volumes are estimated to have reached approximately $46 trillion, a figure comparable to or exceeding the annual transaction volumes of traditional payment giants such as Visa or PayPal.

[Comparison of Annual Transaction Volumes – Stablecoins vs Traditional Payment Networks]

This scale forces a reconsideration of what stablecoins represent. Initially designed as a hedge against crypto volatility, stablecoins are increasingly functioning as a global settlement layer. They enable near-instant, low-cost value transfer across borders without relying on correspondent banking networks or local clearing systems.

a16z argues that this trend points toward a radical outcome: the internet itself becomes a banking system. Rather than routing payments through proprietary bank ledgers, value transfer occurs directly through open protocols. In this model, wallets replace accounts, smart contracts replace clearinghouses, and APIs replace back-office reconciliation.

For emerging markets, this shift carries geopolitical significance. Dollar-denominated stablecoins allow individuals and businesses to access a de facto global reserve currency without a U.S. bank account. For fintech operators and VASPs, stablecoins open the door to programmable finance—automated payroll, escrow, trade settlement, and liquidity management embedded directly into software.

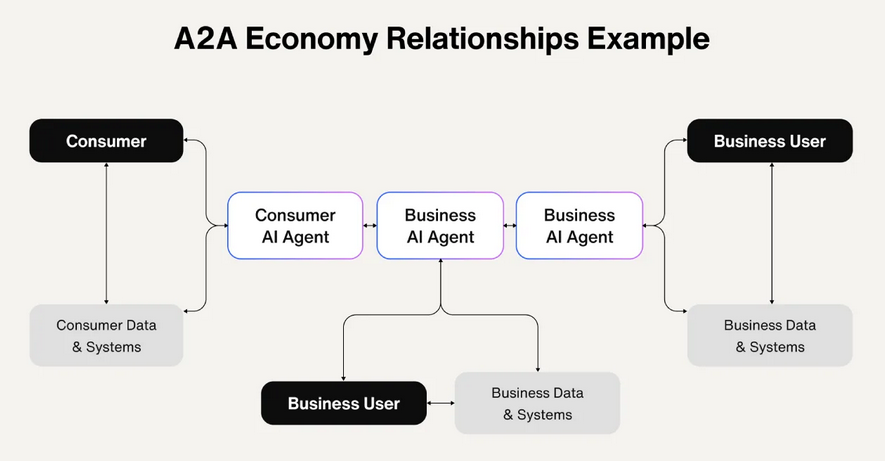

2. AI Agents as Economic Actors: The Rise of KYA

While stablecoins provide the payment rails, a16z identifies AI agents as the next major economic participants to run on top of them. As AI systems become increasingly autonomous—able to negotiate contracts, procure data, allocate compute resources, and execute strategies—the question of identity becomes unavoidable.

To address this, the report introduces the concept of “Know Your Agent (KYA)”, an identity framework for non-human economic actors. Just as KYC establishes trust in human counterparties, KYA would establish cryptographic identity, reputation, and accountability for AI agents.

[AI Agents Operating as Autonomous Economic Participants]

Blockchain plays a central role in this vision. By anchoring agent identities on-chain, AI systems can authenticate themselves, hold assets, sign transactions, and interact with other agents without human intervention. Payments between agents could occur automatically via stablecoins, eliminating invoices, manual approvals, and reconciliation delays.

From a business perspective, this opens new markets. Data marketplaces, compute leasing platforms, and automated service providers could all be transacted machine-to-machine. For crypto investors, protocols that successfully enable KYA-compliant agent economies may represent an entirely new asset class.

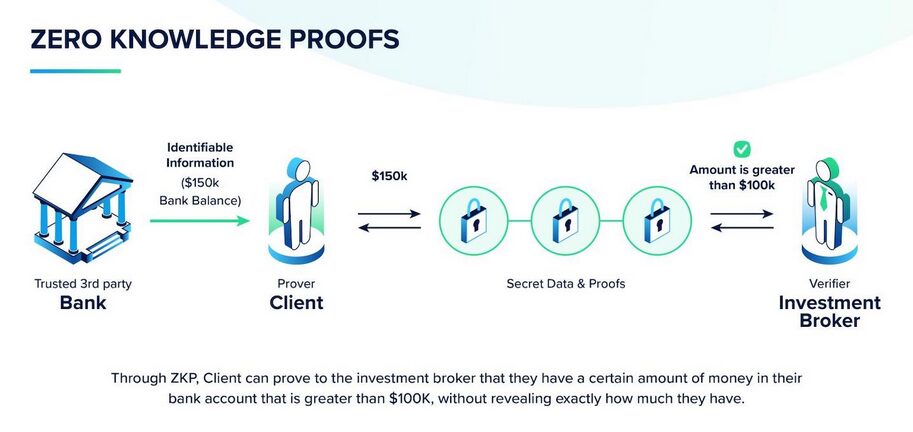

3. Redefining Trust: Privacy as a Competitive Advantage

Trust, in the a16z framework, is no longer a vague social concept but a design property of systems. One of the clearest examples is privacy.

Public blockchains have historically prioritized transparency, making every transaction visible by default. While this property is valuable for auditability, it becomes a liability when institutions, enterprises, and regulated financial actors enter the ecosystem. No major bank or corporate treasury can operate efficiently if all balances and counterparties are publicly exposed.

a16z predicts that privacy-preserving technologies—including zero-knowledge proofs and confidential transaction schemes—will become a primary differentiator among blockchains. Chains that fail to offer robust, verifiable privacy may struggle to attract institutional liquidity, regardless of throughput or fees.

[Privacy Layers Enabling Institutional Blockchain Adoption]

In practice, this suggests a bifurcation of the market. Some networks will remain optimized for radical transparency and retail experimentation, while others evolve into privacy-enabled financial infrastructure suitable for banks, asset managers, and large enterprises.

4. “Spec Is Law”: Security by Design, Not Afterthought

Security is another dimension where trust is being redefined. Traditional financial and software systems rely heavily on post-hoc audits, compliance checks, and manual oversight. a16z argues that this approach is fundamentally insufficient for autonomous, high-speed digital economies.

Instead, the report promotes the idea that “specification is law” (“Spec is law”). In this paradigm, systems are designed such that critical properties—such as solvency, access control, and transaction validity—are mathematically guaranteed by code and formal verification, rather than enforced through ex-post regulation.

This shift has profound implications. Smart contracts that are provably correct reduce the need for trusted intermediaries. Automated risk controls embedded at the protocol level can prevent entire classes of failures before they occur. Over time, this may lower operational costs while increasing systemic resilience.

5. Staked Media: Fighting AI-Driven Misinformation

Beyond finance, a16z extends its analysis to media and information integrity. As generative AI dramatically lowers the cost of content creation, distinguishing signal from noise becomes increasingly difficult. Deepfakes, automated propaganda, and low-quality spam threaten the credibility of online discourse.

The proposed solution is “staked media.” In this model, content publishers are required to stake economic value alongside their claims. If information is proven false or misleading, the stake can be slashed. If it proves accurate and valuable, the publisher is rewarded.

This approach transforms trust from a subjective judgment into an economic incentive system. Blockchain infrastructure enables transparent staking, dispute resolution, and payout mechanisms. While still experimental, staked media represents a concrete attempt to align truthfulness with financial incentives in an AI-saturated environment.

6. Regulation as a Catalyst, Not an Obstacle

Finally, a16z expresses cautious optimism regarding regulation, particularly in the United States. After years of ambiguity and enforcement-driven policy, clearer legal frameworks could unlock long-term investment and mainstream adoption.

Regulatory clarity does not imply deregulation. Rather, it provides predictable rules under which capital, talent, and institutions can commit to building durable networks. a16z argues that once legal uncertainty recedes, the industry’s focus will naturally shift from speculative cycles toward long-term infrastructure development.

For investors and operators, this means that value creation in the post-2026 era is likely to favor protocols with real utility, governance discipline, and regulatory alignment over short-lived hype narratives.

Conclusion: Crypto as the Invisible Backbone of the Digital Economy

The vision outlined by a16z suggests that by 2026, crypto may no longer feel revolutionary—precisely because it will be everywhere. Stablecoins quietly settling transactions, AI agents autonomously exchanging value, privacy layers protecting institutional flows, and cryptographic guarantees enforcing trust at scale.

For those searching for new crypto assets, the implication is clear: the most valuable opportunities may lie not in flashy tokens, but in infrastructure that enables others to build. For those seeking new revenue sources, programmable finance and machine-driven markets open avenues that traditional systems simply cannot support. And for practitioners interested in real-world blockchain applications, the coming years may finally deliver on the technology’s original promise.

Crypto’s next chapter is not about replacing the internet. It is about becoming the internet’s financial and trust layer.