Main Points:

- Former SEC official likens liquid staking to risky rehypothecation practices, sparking industry pushback.

- Liquid staking market has surged to nearly $67 billion TVL by mid-2025, led by Ethereum-based protocols.

- Regulators have provided limited but clarifying guidance, enabling passive staking while restricting leverage.

- Institutional demand and emergent financial products (e.g., LST ETFs) are driving mainstream adoption.

- Investors should assess protocol risk profiles, governance transparency, and yield mechanics.

- Technological innovations, cross-chain staking, and self-custody solutions will shape the next phase.

1. SEC Warning and Industry Response

In early August 2025, Amanda Fisher, former chief counsel at the U.S. Securities and Exchange Commission (SEC), ignited a heated debate by warning that liquid staking closely mirrors the rehypothecation practices that precipitated the 2008 Lehman Brothers collapse. Fisher argued that by enabling repeated reuse of staked assets without robust oversight, liquid staking could pose systemic risks to the broader financial ecosystem. She noted that liquid staking tokens effectively allow multiple parties to claim the same underlying collateral, a scenario strikingly similar to the over-leveraging and opacity that sank Lehman.

Industry leaders quickly rebuffed Fisher’s comparison. They highlighted that liquid staking operates under transparent, code-governed protocols that publish collateral ratios and issuance metrics on-chain. Unlike traditional financial rehypothecation, where assets can be rehypothecated multiple times off-ledger, liquid staking smart contracts enforce strict accounting: each staked token is fully collateralized by the underlying crypto asset locked in the protocol. Experts also emphasized that the SEC’s guidance applies exclusively to passive, non-leveraged staking services, a nuance Fisher’s critique overlooked.

2. The State of Liquid Staking: Market Growth and Protocol Comparison

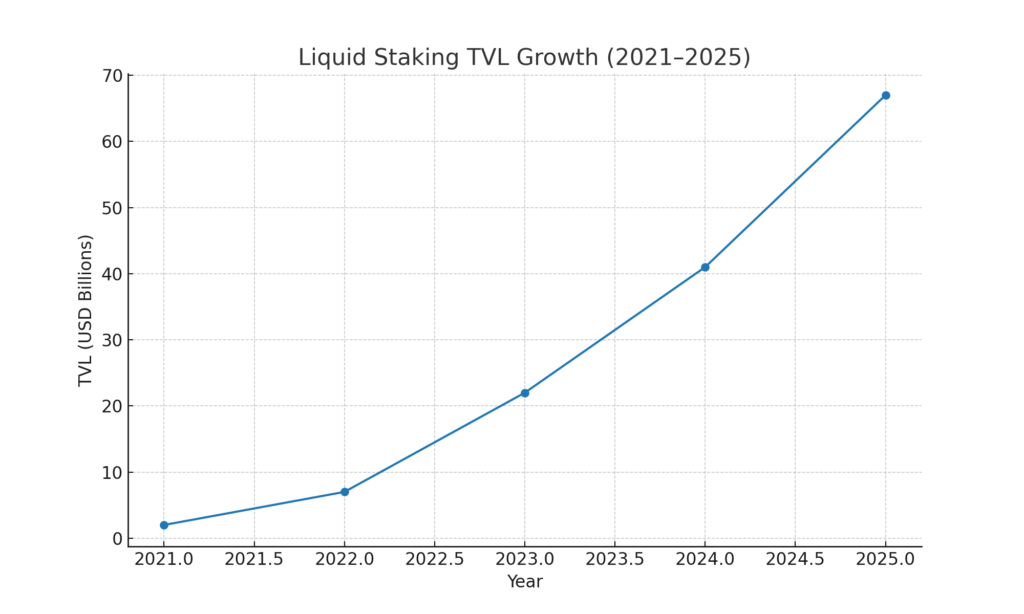

Liquid staking has transitioned from a niche DeFi experiment to a cornerstone of the proof-of-stake ecosystem. As of mid-2025, Total Value Locked (TVL) in liquid staking protocols has surged to approximately $67 billion, up from just $2 billion in 2021. Ethereum-based solutions account for roughly $51 billion of this sum, reflecting both the network’s dominance and the compelling yield opportunities staking provides.

Figure 1: Liquid Staking TVL Growth (2021–2025)

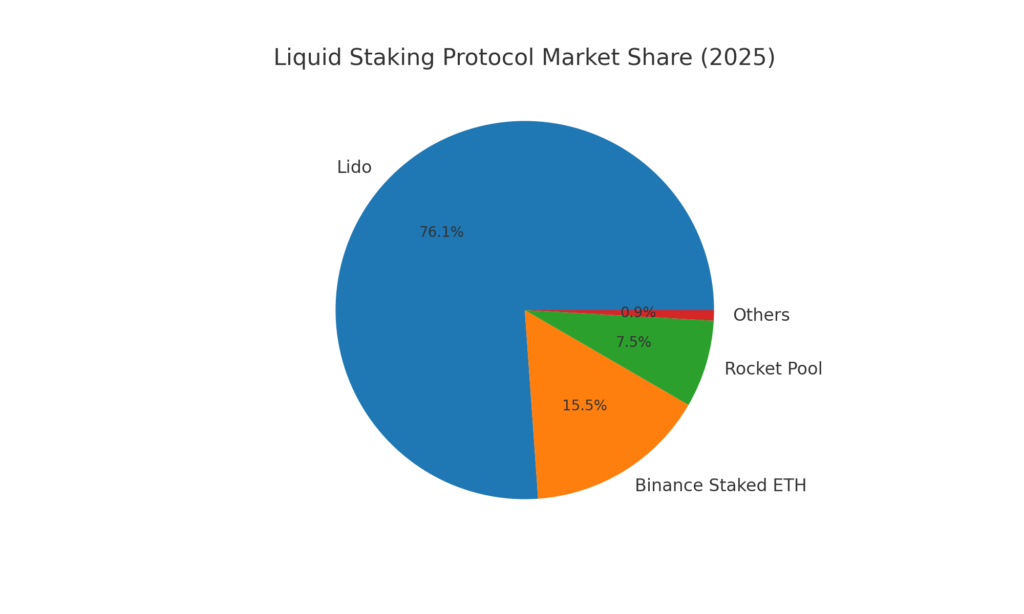

Within this booming market, several protocols have emerged as leaders:

Protocol Comparison

- Lido Finance commands the lion’s share with $31 billion stETH TVL (≈46 % of the liquid staking market).

- Binance Staked ETH follows with $10.4 billion, leveraging Binance’s on-exchange liquidity and staking infrastructure.

- Rocket Pool has carved out a niche among decentralization purists, managing $5 billion in rETH assets, thanks to its node-minimum 16 ETH participation model.

- Other players (including Stakewise, Ankr, and upcoming EigenLayer derivatives) fill out the remaining $0.6 billion.

Figure 2: Liquid Staking Protocol Market Share (2025)

These platforms differ in fee structures, governance mechanisms, and collateral models. For example, Lido charges a 10 % protocol fee on staking rewards, while Rocket Pool’s fee sits closer to 15 %. Binance offers near-zero fees for institutional clients in high-volume tiers, reflecting its exchange-based custody advantage.

3. Regulatory Developments and Market Implications

The SEC’s updated stance, part of Chairperson Lisa Atkins’s “Project Crypto” initiative, issued in July 2025, clarified that purely administrative liquid staking tokens—provided they represent direct claims on staked assets without leverage—are unlikely to be deemed securities. This limited carve-out aims to foster innovation while guarding against excessive risk layering.

However, regulators continue to scrutinize liquid restaking products that layer additional collateral reuse. While simple liquid staking (e.g., stETH) is in the clear, restaking solutions that permit trampoline-like reuse of validator shares could face securities classification or custodial licensing requirements. Consequently, protocol developers are emphasizing on-chain transparency, standardized smart contract audits, and insurance integrations to address potential counterparty concerns.

4. Practical Insights for Investors

For readers seeking new crypto assets or passive income streams, liquid staking presents an attractive blend of yield, liquidity, and protocol-driven governance. Here are actionable considerations:

- Collateral Transparency: Prioritize protocols that publish real-time collateral ratios and maintain independent reserve audits.

- Governance Participation: Assess on-chain governance models and token holder rights; protocols with decentralized DAO structures may react more swiftly to market disruptions.

- Yield Mechanics: Compare APR versus APY after fees and take into account slashing risks—smarter protocols distribute slashing insurance or rebates to mitigate validator misbehavior.

- Custody Options: Decide between native wallet staking (e.g., Lido via MetaMask) and custodial staking (Binance Earn, Coinbase) based on your security tolerance and withdrawal flexibility.

- Tax Implications: Understand how your jurisdiction treats staking rewards and token swaps, as converting stETH back to ETH may trigger taxable events.

5. Future Outlook and Innovations

Looking ahead, several trends are poised to shape liquid staking’s next chapter:

- Cross-Chain Staking: Protocols like pSTAKE and Stader Finance are enabling ETH staking across Cosmos, Polkadot, and Layer-2 networks, expanding utility and yield aggregation.

- Liquid Staking ETFs: Financial institutions are filing proposals for exchange-traded products that bundle LSTs, promising regulated access for traditional investors.

- DeFi Integrations: Yield-optimizers and lending platforms are increasingly accepting stETH and rETH as collateral, unlocking composability.

- Insurance and Derivatives: On-chain insurance pools and derivative products (e.g., insured staking vaults) will offer more robust risk management.

These innovations reinforce the transition from peripheral DeFi use cases to mainstream financial applications, making liquid staking a critical component for both retail and institutional strategies.

Conclusion

Liquid staking has weathered skepticism and regulatory scrutiny to emerge as a resilient, rapidly growing pillar of the crypto ecosystem. With nearly $67 billion in TVL, a clear regulatory path for passive models, and a pipeline of institutional products on the horizon, the market offers compelling opportunities. Investors should conduct due diligence on collateral practices, governance frameworks, and protocol innovations to harness the full potential of liquid staking. Far from a Lehman-style ticking time bomb, properly structured liquid staking protocols may well become the bedrock of next-generation decentralized finance.