Key take-aways :

- Central banks are moving beyond hostile stances on crypto, beginning to formally recognise digital assets — especially stablecoins — as part of payment and settlement systems.

- The newly-enacted U.S. federal law (the GENIUS Act) provides the first comprehensive regulatory framework for payment stablecoins in the U.S., and signals a structural shift.

- Stablecoins are increasingly positioned not just as trading‐tools for crypto insiders but as potential infrastructure components for cross-border payments and global monetary systems.

- The reshaping of “banking services” (e.g., deposit, settlement, value transfer) via blockchain and stablecoins presents both opportunities and system-wide risks, which regulators are now actively tackling.

- For investors and practitioners in Japan (and globally), the regulatory “catalyst” emerging from central-bank dialogues and legislative clarity could trigger the next phase of institutional adoption — hence paying attention to the regulatory architecture is now as important as picking tokens.

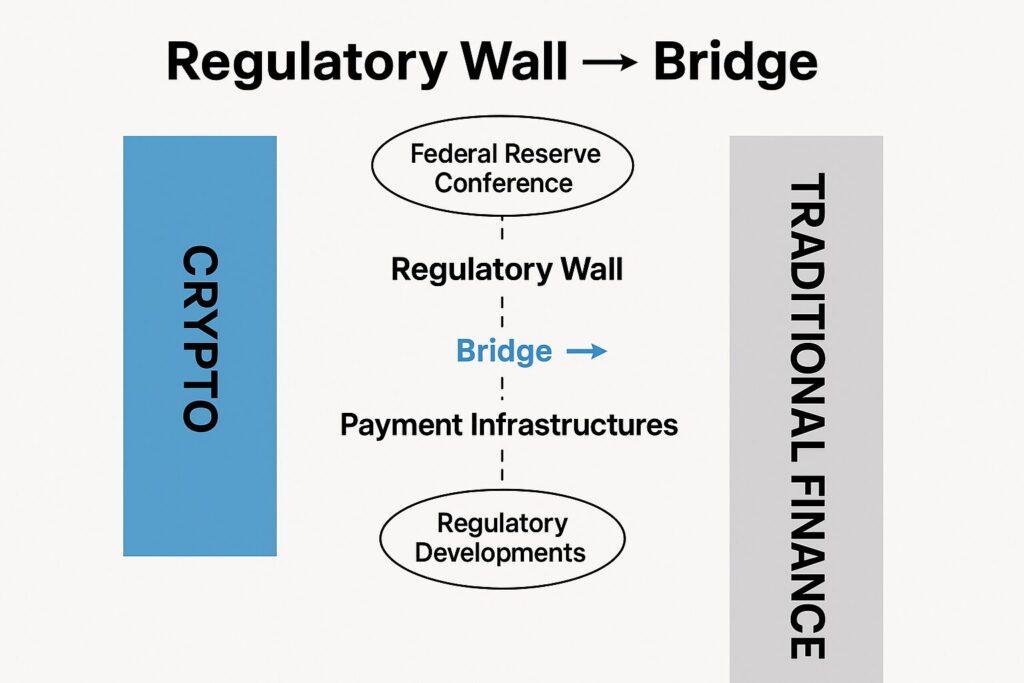

1. Public Recognition of Crypto by Central Banks: When the Regulatory Wall Becomes a Bridge

In recent months, forums organized by the Federal Reserve Board (FRB) and other central banks have signalled a landmark moment for the crypto sector: digital assets are no longer peripheral speculative instruments, but are beginning to be treated as legitimate subjects for debate in payment and settlement infrastructure.

For example, in a speech on October 16 2025, Fed Governor Michael Barr emphasised that the recently-enacted GENIUS Act empowers four federal agencies and state agencies to serve as primary regulators for stablecoin issuers. He cautioned, however, that unless carefully coordinated, diverse regulatory regimes could permit arbitrage and increased risk.

This shift of tone – from “crypto is wild west / speculative only” to “let’s discuss how crypto fits into financial infrastructure” – is meaningful. When a central-bank idiom frames digital assets as part of infrastructure rather than fringe, the regulatory wall starts to function as a bridge to mainstream finance. The practical consequence is that the mere existence of structured forums between regulators and industry players becomes itself a major catalyst for the market.

In that sense, this moment marks the turning point: central banks are implicitly acknowledging that crypto-assets (especially stablecoins) may play a functional role as value-transfer rails, liquidity providers, or even settlement layers — not just speculative tokens. As the Brookings Institution notes, the GENIUS Act “clarifies much, but financial regulators must now write rules that will determine if stablecoins can gain trust and contribute to a more efficient, lower-cost payments system, or if they will continue to be used mainly for crypto trading.”

For investors and practitioners in the blockchain space, this means regulatory clarity is less a distant dream and more an emergent reality — a structural shift rather than a cyclical “crypto hype” move.

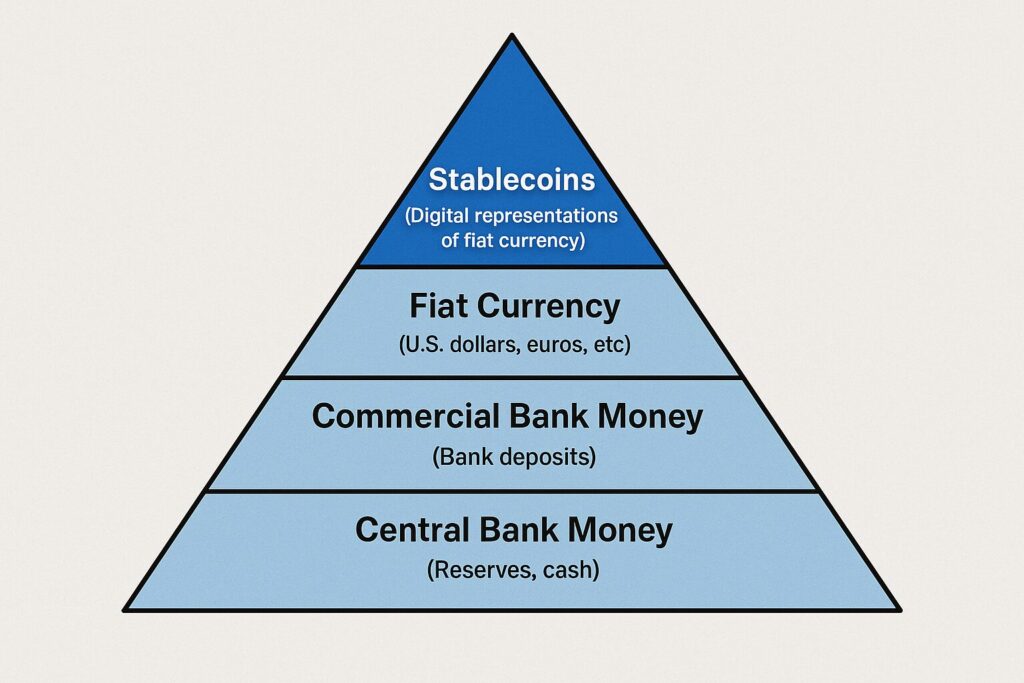

2. Stablecoins as the Main Player in Financial Stability

One of the standout themes in recent regulatory dialogues is the focus on stablecoins: digital tokens pegged to fiat or near-fiat assets that offer minimal volatility and high interoperability. The fact that stablecoins are appearing front-and-centre in central-bank discussions signals a larger shift: crypto is not just about speculation, but about payments, liquidity, and financial-infrastructure risk.

Stablecoins can replicate many of the functions of fiat currency — especially for cross-border payments or rapid settlements — and this is precisely the reason regulators are giving them heightened attention.

Why stablecoins are now viewed as a “system-level” concern

- Since stablecoins can (in principle) offer near-instant transfers, low friction, and global reach, they pose different risks (liquidity, redemption-run risk, reserve-transparency) than traditional crypto.

- The aforementioned paper “Hybrid Monetary Ecosystems” shows that as of early 2025 stablecoins had become so large (USD 200 billion+ market cap) that they may operate alongside fiat in a hybrid monetary architecture — something central banks cannot ignore.

- In everyday regulatory language, this means stablecoins may affect the “singleness of money”, payment‐settlement safety, and even the channels by which credit flows or deposits are held — all core banking concerns.

Regulatory contours around stablecoins

In the U.S., the GENIUS Act sets key rules for payment stablecoins:

- They are neither securities nor national currencies, nor do they have deposit insurance or automatic access to Fed payment services.

- Issuers must hold at least USD 1 of “permitted reserves” for each USD 1 of stablecoin in circulation; reserves may include U.S. dollars, short‐dated Treasuries, certain repos, etc.

- The Act tasks regulators with defining capital, liquidity, risk-management, and incident liquidity back-stop frameworks for stablecoin issuers within 18 months.

- AML/KYC and sanctions regimes apply: stablecoin issuers are treated as financial institutions under the Bank Secrecy Act (BSA) and must ensure they have appropriate systems for blocking illicit flows.

What this means for the ecosystem is a maturation phase: stablecoins are transitioning from loosely regulated tokens to regulated infrastructure components with obligations akin to banks (in effect). For practitioners and blockchain projects, this implies that stablecoin-related design (reserve structure, transparency, redemption mechanism) will increasingly be scrutinised as much as tokenomics or yield models.

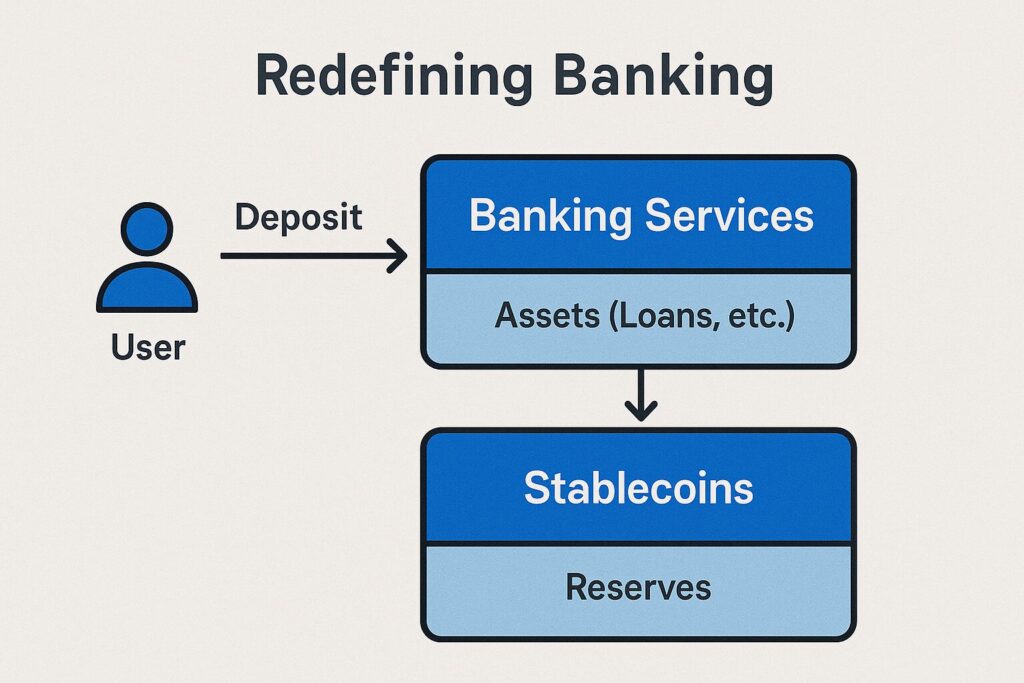

3. Redefining “Banking Services”: The Implication of Stablecoins & Crypto Infrastructure

Beyond stablecoins per se, the broader structural discussion centres on how crypto infrastructure (blockchain, tokens, rails) is redefining traditional banking services. In many regulatory statements, the questions being asked are: what constitutes “banking”? How do payment, deposit, credit, settlement, and money-intermediation functions get carved out in a blockchain-native world?

Stablecoins as “digital-banks”

Regulators are explicitly framing some stablecoin issuers as digital versions of banks. For example, compliance guidance notes that stablecoin issuers affiliated with banks may be exempted from certain consolidated capital requirements under the GENIUS Act, which raises concerns about risks being shifted into a lightly regulated corner. +1

This suggests two things: stablecoins may function like banks (taking deposits in effect), and innovation may create entities that straddle “banking” and “crypto” functions. The regulatory challenge is to define how supervision, capital buffers, liquidity standards apply in this new hybrid world.

Impact on banking revenue models and structure

One of the central-bank lamentations is how crypto rails threaten the traditional banking model — especially cross-border remittances, correspondent banking, and settlement services. The speed, cost-efficiency, and global reach of tokenised value transfers mean that banks face pressure to either adopt blockchain rails or risk being squeezed out of key payment flows.

From the viewpoint of investors and builders, this means the arena of competition moves: crypto projects are no longer competing only with other tokens—they are competing with banks, payment networks, and inter‐bank settlement channels. That elevates the stakes: infrastructure-scale adoption, regulatory alignment, interoperability, and settlement-layer robustness become key success factors.

Central bank balancing act

Central banks like the Fed face a dual mandate: foster innovation (so that their jurisdictions stay competitive) and maintain financial stability (so that no opaque “crypto bank” causes a systemic run). As Governor Barr pointed out, unless regulatory frameworks are coordinated, there is a risk of issuers choosing lenient jurisdictions (“regulatory arbitrage”) which could undermine systemic resilience.

Hence we may expect:

- More stablecoin issuers aligning with bank-like capital/liquidity standards.

- Increased regulatory scrutiny of “native crypto banking” models (lending, custodian services, tokenised deposits).

- Partnerships between banks and blockchain platforms as a way to leverage the tech while maintaining supervised status.

4. What It Means for Japanese Investors and Blockchain Practitioners

From the domestic Japanese perspective, the significance of these international developments should not be underestimated. The U.S. regulatory trajectory (via the GENIUS Act and Fed conferences) is acting as a major catalyst not just for U.S. markets but for the global crypto-asset ecosystem (including Japan).

Regulatory clarity as a market catalyst

For investors, one of the biggest uncertainties in crypto has been regulatory unpredictability. The establishment of a clear framework for stablecoins in a major jurisdiction like the U.S. reduces one layer of risk. As the Brookings article suggests, the GENIUS Act “clarifies much… but regulators must now write rules that will determine if stablecoins can gain trust.”

Reduced uncertainty tends to attract institutional capital. On the Japanese side, a clearer U.S. regulatory horizon helps local players benchmark global standards, evaluate cross-border stablecoin models, and participate in frameworks earlier.

Strategy for Japanese investors

- Focus on infrastructure plays: Projects that align with regulated stablecoins, payment rails, cross-border settlement or tokenised real-world assets may benefit from the structural tailwinds.

- Monitor regulatory mapping: Which jurisdictions adopt stablecoin frameworks, how issuers comply with reserve and transparency requirements, and how Japan’s regulators respond.

- Emphasise long-term core holdings: If stablecoins indeed become embedded infrastructure, the winners will be those with durable, compliant business models—not short-term speculative plays.

- Be mindful of risk: Even with clearer rules, cross-border token models carry legal, compliance and technology risk—portfolios should be structured accordingly.

5. Recent Developments & Market Signals

While much of the above relies on regulatory announcements, several recent signals reinforce the pace of change.

- The Financial Stability Board (FSB) published a report on October 16 2025 warning that regulatory gaps allow stablecoin issuers to engage in regulatory arbitrage—a vulnerability for global financial stability.

- In the UK, the Bank of England indicated it will only lift planned stablecoin-holding caps when confident there is no threat to financial stability – signaling discipline rather than laissez-faire.

- Fed Governor Michelle Bowman publicly urged regulators to adopt a less cautious mindset and engage with emerging technologies like blockchain and crypto, reflecting a cultural shift at the central bank level.

These signals suggest that the regulatory environment is moving from ad-hoc responses to proactive frameworks. For blockchain practitioners and investors seeking “the next move” in crypto, this sets the stage for infrastructure-driven themes: stablecoins, tokenised value, regulated rails, and interoperability.

Conclusion

The ongoing evolution in central-bank and regulatory engagement with crypto assets marks a structural shift: what was once peripheral and speculative is now gaining formal recognition as part of the financial-infrastructure debate. The U.S. GENIUS Act, the discussions by the Fed, and global signals from regulators collectively point to stablecoins and tokenised rails becoming integrated — under supervision — into mainstream finance.

For those exploring new crypto assets or seeking next-generation revenue sources in blockchain, the game is changing. It is no longer enough to launch a token with yield; success increasingly depends on infrastructure viability, regulatory alignment, reserve integrity, and interoperability. Japanese investors and builders are well-positioned to benefit by aligning with projects that anticipate these structural shifts rather than merely chasing the next rally.

In short: the regulatory wall is transforming into a bridge — and those ready to cross early, with clarity and strategic foresight, may find themselves ahead of the pack.