Key Points :

- KuCoin Pay has partnered with DFX.swiss to enable stablecoin and cryptocurrency payments at over 100 SPAR supermarket stores across Switzerland, using DFX’s OpenCryptoQR system.

- The deal features zero gas (transaction) fees for the users; merchants receive immediate fiat settlement; payments via QR codes through the KuCoin app.

- The move is part of a growing trend: stablecoins and crypto payments are shifting from pilot projects to practical, everyday payments infrastructure. Real adoption in retail, cross-border, regulatory clarity, and better payment rails are pushing things forward.

- Regulations like the U.S. GENIUS Act, Europe’s MiCA, and local fintech innovations are increasingly shaping the environment, reducing risk and enabling merchants and users to use stablecoins with more trust.

- Despite momentum, challenges remain (e.g., user awareness, volatility, infrastructure, regulatory complexity) which must be addressed for stablecoins to become as ubiquitous as credit cards or mobile wallets.

Introduction: Beyond Speculation — Crypto in the Checkout Line

In recent years, cryptocurrencies have largely been viewed as investment assets or speculative tools. However, a new wave of developments is pushing them into everyday commerce. The recent announcement that KuCoin Pay, in partnership with DFX.swiss, is enabling stablecoin and cryptocurrency payments at over 100 SPAR supermarket outlets across Switzerland, marks a significant turning point. With zero gas fees for shoppers and instant fiat settlements for merchants, this initiative exemplifies how crypto is being integrated into regular retail settings. This article dissects that development, places it in the context of broader trends, examines regulatory and infrastructure shifts, and explores what this means for people scouting for the next big crypto use case or revenue stream.

1. KuCoin Pay & SPAR: What’s New in Switzerland

KuCoin Pay, the payments arm of the crypto exchange KuCoin (which has over 41 million users globally), has teamed up with Swiss fintech DFX.swiss to bring stablecoin and crypto payments to SPAR supermarkets across Switzerland. Through DFX’s OpenCryptoQR system integrated into the KuCoin app, shoppers simply scan a QR code at the store, select a supported cryptocurrency or stablecoin (e.g. USDT, USDC, KCS, etc.), and make payment. Importantly, while customers enjoy zero gas fees, merchants receive payments instantly in fiat (Swiss francs), avoiding exposure to crypto volatility.

This service expands what SPAR has already begun with Binance Pay + DFX.swiss. SPAR’s footprint for crypto-capable outlets is expected to grow further—reports suggest the number may rise to over 300 stores in the coming months. 2. Why It Matters: From Pilot to Practical

This development is not happening in isolation. Over the past year or more there has been a marked shift:

- According to recent reports (e.g. from Fireblocks and others), nearly 90% of institutions involved in payments are now taking action on stablecoins—either exploring, piloting, or launching real use cases.

- One of the strongest use cases for stablecoins has been cross-border payments, due to the potential for lower cost, faster settlement, and 24/7 availability. Traditional systems (SWIFT, correspondent banking) are increasingly seen as slow, opaque, and expensive.

- That said, even as usage increases, stablecoins account for only a very small fraction of global money flows. For example, the total volume of daily stablecoin transactions (≈ US$30 billion) is still less than 1% of global payments traffic.

So what SPAR + KuCoin Pay represent is a transition point—where stablecoin payments are moving from being theoretical or niche into being part of everyday retail infrastructure.

3. Regulatory & Infrastructure Catalysts

Several factors are combining to make this kind of retail crypto payment viable:

- Regulation catching up: In the U.S., the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) provides a framework requiring full reserve backing, audits, state/federal compliance.

- In Europe, MiCA (Markets in Crypto-Assets Regulation) has imposed rules for asset-referenced tokens and stablecoins, creating a clearer legal environment.

- Infrastructure readiness: Non-custodial (self-managed) wallets, better QR payment standards (like OpenCryptoQR), fiat-on ramps/off ramps (banking / credit card tied) are becoming more robust.

- Merchant incentives: Lower fees, faster settlement, and attractiveness to customers who favor crypto are pushing retailers to adopt. If merchants are protected from volatility and regulatory risk, the case becomes stronger. The SPAR setup shields merchants via instant fiat settlement.

4. Global Movement: Other Examples & Trends

To see whether Switzerland is part of something bigger, here are other relevant trends and regional developments:

- In the U.S., large retailers like Amazon and Walmart are reported to be exploring either their own stablecoins or integrating stablecoin payment options to reduce credit card fees.

- Infrastructure players (banks, payment processors, fintechs) are increasingly seeing stablecoins as strategic, not speculative.

- Emerging markets, especially Latin America, are among the most active in real-world stablecoin usage, particularly for cross-border remittances and where traditional banking is weak.

5. Risks, Frictions, and What Still Needs Fixing

Despite promising signs, there are still considerable hurdles before stablecoin and crypto payments become as ubiquitous as credit cards or digital wallets:

- Volatility risk: Even stablecoins can depeg; exposure to price swings or reserve mismatch remains a concern. Regulatory clarity helps, but the risk is non-zero.

- User experience & complexity: Crypto wallets, private keys, fees (gas on certain chains), and not all consumers are familiar or comfortable. Also, converting crypto to fiat (for merchants) needs to be seamless.

- Regulatory uncertainty in many jurisdictions: While regions like EU and U.S. are advancing rules, many countries remain ambiguous. Cross-border legal issues (AML, consumer protection, reserve requirements) are still being worked out.

- Competition with incumbents and alternate payment methods: Traditional payment providers (Visa, Mastercard), mobile payment systems, domestic digital payment apps often have entrenched usage, regulatory support, and consumer trust. In Switzerland for instance, apps like TWINT are major competitors.

6. What This Means for New Cryptos, Projects, and Revenue Streams

For those looking for the “next big thing” in crypto, payments, or blockchain-enabled businesses, here are some takeaways:

- Projects that focus on stablecoins (not just volatile tokens) and build payment use cases can have more traction, especially if they can integrate with POS (point-of-sale), retail, or everyday services.

- Infrastructure-as-a-service (wallets, QR code payment systems, fiat rails, regulation compliance layers) becomes a valuable space. Those who provide secure, compliant, low-fee rails may capture significant value.

- Partnerships between exchanges/payments platforms (like KuCoin) and local financial/fintech entities (like DFX.swiss) are effective models: combining crypto expertise with local regulatory and retail infrastructure knowledge.

- Regulatory alignment (issuing stablecoins that are fully backed, audited, compliant) is increasingly non-optional. It’s a competitive advantage.

7. Recent Figures & Market Scale (as of mid-2025)

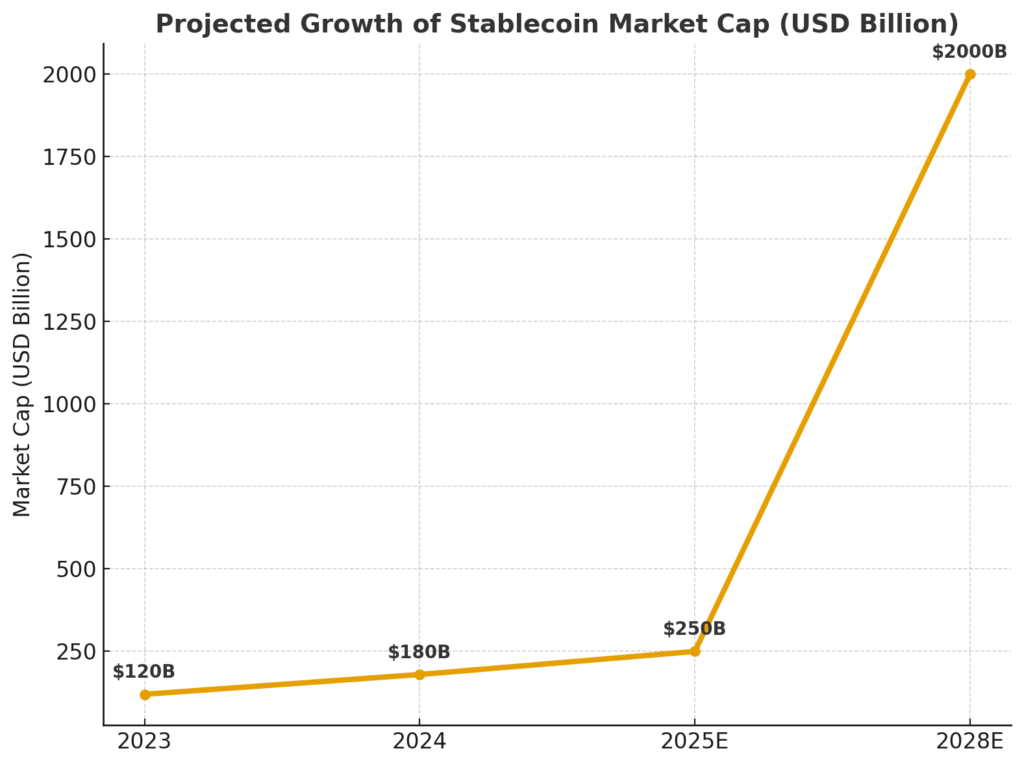

- The market capitalisation of stablecoins is around USD 200-250 billion, most denominated in U.S. dollars.

- Daily stablecoin transaction volume is in the order of USD 30 billion, still less than 1% of global daily money flows.

- Growth projections are strong: some estimates foresee stablecoin issuance exceeding USD 400 billion by end of 2025, and reaching USD 2 trillion by 2028.

Summary: Toward the Future of Everyday Payments

The examples of KuCoin Pay and SPAR are highly symbolic as a step toward making cryptocurrencies and stablecoins “usable.” Until now, “cryptocurrency payments” have been seen as experimental, limited to select cities in developed countries, or online. However, as their adoption in stores increases, trust and practicality among both users and stores will rapidly increase.

For those considering future revenue sources and projects, payment-conscious design and partnerships, regulatory compliance, and ease of use will be key. Success will depend on the stablecoin’s design (backing, transparency, reliability), infrastructure (QR code payments, on/off ramps), and user experience in the local market.

If this trend accelerates, it’s likely that paying with cryptocurrencies and stablecoins in much the same way as paying with a credit or debit card will become a common practice in many countries within the next few years.