Main Points:

- What changed today: A new Executive Order directs regulators to make it easier for 401(k) plans to include crypto, private equity, and real estate, reversing the prior stance that discouraged crypto in retirement menus.

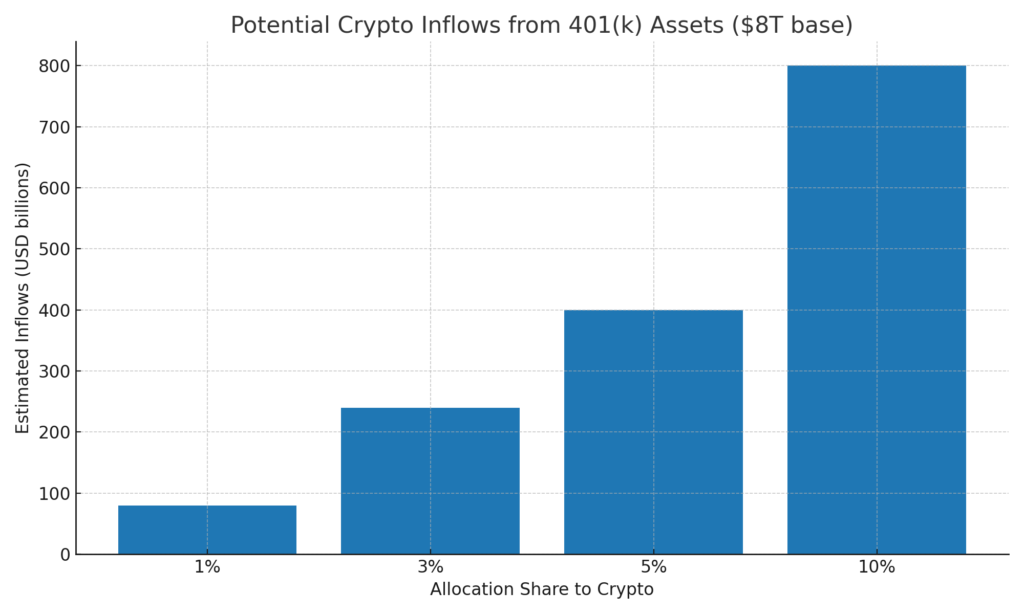

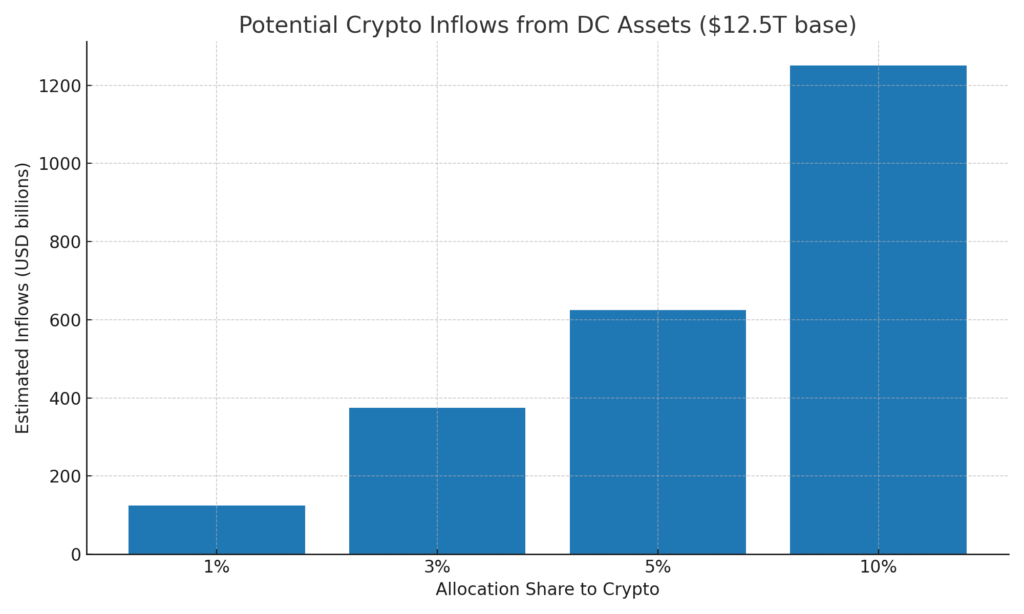

- Why this matters for crypto liquidity: Even a 1% allocation from the $8T–$12.5T U.S. defined-contribution base implies tens to hundreds of billions in potential inflows to digital assets over time.

- What regulators must still clarify: The Labor Department (DOL) and SEC must produce follow-on guidance on fiduciary duty, plan design, disclosures, valuation, custody, and participant protections before large plans move.

- Who stands to gain: Alternative-asset heavyweights (e.g., Blackstone, Apollo), multi-asset managers (e.g., BlackRock), and crypto firms positioned for qualified custody, indexing, and low-cost plan wrappers.

- Risk lens for fiduciaries: Crypto’s volatility, fees, and operational risk still demand ERISA-grade process, despite DOL’s shift back to a “neutral” posture after rescinding its 2022 “extreme care” warning in May 2025.

- Actionable takeaways: Builders should prioritize retirement-grade products (index funds, target-date sleeves, and SMA rails) with compliant custody and reporting; allocators should prepare policy statements and guardrails before the first dollar goes in.

1) What changed today

The United States has formally pivoted from “discourage” to “enable” on alternative assets in participant-directed retirement plans. On August 7, 2025 (U.S. time), President Donald Trump signed an Executive Order instructing federal agencies to make it easier for 401(k) plans to offer alternative assets—including cryptocurrencies, private equity, private credit, and real estate—within ERISA-governed menus. Reuters and Bloomberg reported the signing, and the White House published a fact sheet outlining the policy goals.

Crucially, the order tasks the Labor Secretary with reviewing guidance and collaborating with Treasury, the SEC, and other regulators to align rules on plan design and fiduciary obligations. The text also signals that the SEC should consider adjustments to how “accredited investor” or “qualified purchaser” concepts apply when participants access alternatives inside regulated retirement wrappers—an important nod to practical access.

This is a rapid follow-through on groundwork laid in late spring: on May 28, 2025, the DOL formally rescinded the Biden-era Compliance Assistance Release (CAR 2022-01) that had warned fiduciaries to exercise “extreme care” before adding crypto to 401(k) menus, calling that phrasing a departure from ERISA’s historically neutral, principles-based approach.

2) Why this matters for crypto liquidity

The potential capital base is large. Depending on the definition, U.S. 401(k) assets are roughly $8 trillion, while the broader defined-contribution universe can be framed closer to $12–$12.5 trillion. If crypto captures just 1% of the $8T 401(k) market, that implies on the order of $80 billion in cumulative inflows; scale the allocation to 10% and you are talking about around $800 billion. Using a $12.5T base pushes those figures to roughly $125 billion and $1.25 trillion, respectively. Research commentary frequently cites the 1% ≈ $80B figure as a conservative “first stop,” with higher allocations over time as products mature.

These are not one-time lump sums; retirement plans channel fresh contributions each pay cycle. That transforms crypto exposure—especially diversified sleeves or index strategies—into a steady dollar-cost-averaging bid that could dampen cyclicality and support market depth across Bitcoin, Ether, and, eventually, broader digital-asset baskets.

3) What regulators must still clarify before large plans move

Fiduciary process and prudence. The DOL has returned to a neutral, principle-based view, but neutral is not permissive. ERISA prudence requires documented process: investment policy statements that articulate objectives, benchmarks, rebalancing rules, and risk controls; manager due diligence; and fee reasonableness analysis. Expect supplemental DOL FAQs and bulletins to refine what “prudence” looks like for digital assets inside pooled funds or target-date structures.

SEC alignment for practical access. The order explicitly invites the SEC to explore ways to facilitate access to alternatives in participant-directed plans, including re-examining how accredited/qualified purchaser concepts interact with plan menus. That could unlock structures where a registered ’40 Act fund, CIT (collective investment trust), or separate account embeds a measured crypto sleeve without each participant having to qualify individually.

Valuation, liquidity, and disclosure. Plan fiduciaries will need confidence that the NAV-calculation, liquidity management, and fair-valuation policies of any crypto-inclusive fund meet retirement-plan standards. Expect model-portfolio designs (e.g., target-date funds) to begin with small crypto allocations inside diversified sleeves that publish clear methodologies and risk metrics.

Custody and operations. Retirement-grade custody (cold storage, SOC 2/ISO controls, segregation, insurance, dual-control workflows) remains non-negotiable. The order doesn’t change custody risk; it changes the policy backdrop that allows fiduciaries to evaluate it within ERISA principles.

4) Who stands to gain

Alternative-asset platforms. Large alt managers and multi-asset giants have positioned themselves as retirement partners. Analysts immediately flagged Blackstone, Apollo, and BlackRock as likely beneficiaries, given their distribution into plan menus and experience building semi-liquid vehicles and model portfolios. The order widens their addressable market.

Crypto product issuers and indexers. Expect demand for retirement-grade wrappers—registered funds, CITs, and SMAs—that offer Bitcoin-only, Bitcoin-plus-Ether, or diversified digital-asset indices. Low-tracking-error, low-fee exposures with robust creation/redemption plumbing will be favored.

Qualified custodians and administrators. The back-office layer—custody, fund admin, valuations, attestations, audit—becomes the moat. Providers that already service spot crypto ETFs or institutional funds have an advantage in meeting ERISA-level RFPs.

Advisory platforms and recordkeepers. Target-date providers, managed-account platforms, and major recordkeepers will be gatekeepers. Early movers will pilot sleeves in professionally managed options before opening any self-directed windows.

5) The risk lens for fiduciaries

Even with the policy shift, crypto remains volatile and operationally distinct. ERISA fiduciaries will likely stage adoption through capped allocations, glidepath-aware exposures for target-date funds, and robust participant education.

Fee discipline. Retirement plans are sensitive to basis-point drag. Sponsors will negotiate hard on fees, favoring exposures that leverage existing ETF liquidity or CIT scale.

Operational and regulatory risk. Token events (forks, airdrops), exchange venue risk, and on-chain operational nuance require policies spelled out in offering docs and service-provider contracts. The DOL’s rescission of its 2022 “extreme care” bulletin doesn’t eliminate prudence obligations; it restores the standard ERISA lens—documented process, best interest, and monitoring.

6) Sizing the prize: scenario math

Let’s translate headline asset bases into order-of-magnitude flows:

- Scenario A (401(k) base ≈ $8T).

1% allocation ≈ $80B; 3% ≈ $240B; 5% ≈ $400B; 10% ≈ $800B over time. These are directional, not promises, and presume a gradual uptake as fiduciaries grow comfortable. - Scenario B (DC base ≈ $12.5T).

1% allocation ≈ $125B; 3% ≈ $375B; 5% ≈ $625B; 10% ≈ $1.25T. This aligns with reporting that framed the target market closer to $12T–$12.5T for alternative-asset access.

[Insert Figure 1 here]

[Insert Figure 2 here]

These flows won’t arrive all at once. Historically, plan adoption of new asset classes starts within professionally managed options (target-date funds, balanced funds) at low single-digit sleeves, then expands as track records and participant education solidify.

7) Near-term roadmap: what happens next

Regulatory follow-ups. Expect DOL to publish clarifications and FAQs within the six-month review window set by the order, in coordination with Treasury and the SEC. The SEC, for its part, was asked to consider rule and guidance adjustments to enable access for plan participants—potentially touching on fund structures, disclosures, and whether existing accredited/qualified purchaser concepts need tailored relief in the retirement context.

Plan-sponsor pilots. Large employers with sophisticated committees may pilot tiny crypto sleeves inside diversified options run by well-known target-date providers. Adoption is likely staggered: pilots, then broader menu additions based on participant feedback and observed outcomes.

Product build-out. Expect an arms race among fund issuers, custodians, and recordkeepers to deliver plug-and-play integrations with sponsor workflows (data feeds, fee billing, QDIA compatibility, participant education modules, and call-center scripts).

8) The broader policy turn: “debanking” and access

The same policy package includes a push against alleged “debanking” of lawful industries (crypto among them). Reports indicate a parallel order directing agencies to examine whether banks have discriminated against customers based on industry, politics, or religion—a response to claims associated with so-called “Operation Choke Point 2.0.” If enforced, this could reduce friction for crypto companies seeking basic banking, complementing the retirement-access initiative.

9) Practical playbook

For builders and issuers

- Design retirement-grade wrappers. Focus on registered funds, CITs, and SMA rails that can slot into model portfolios and target-date funds.

- Institutional custody and admin. Offer SOC-audited custody, proof-of-control, incident response, and insurance.

- Education-first materials. Provide plain-English guides on volatility, rebalancing, and long-horizon behavior.

- Fee compression. Assume fee-sensitive plan committees; compete on TER and tracking.

- Recordkeeper integration. Pre-build data pipes and participant-facing UX components (statements, risk meters, glidepath visuals).

For allocators and plan sponsors

- Update IPS and QDIA policy. Define allowable asset sleeves, ranges, rebalancing bands, and triggers.

- Start small. Pilot 0.5%–1% sleeves in professionally managed options; monitor tracking error and participant outcomes.

- Manager and custodian RFPs. Score on custody controls, liquidity, fair-value policies, and total cost.

- Participant education. Avoid hype; emphasize time horizons, diversification, and dollar-cost averaging.

- Governance cadence. Establish quarterly oversight, stress-testing, and exception reporting.

10) What to watch in the coming months

- DOL/SEC deliverables that translate the Executive Order into operational guidance for plan menus.

- First-wave target-date funds quietly embedding 0.5%–1% crypto sleeves under strict guardrails.

- Recordkeeper announcements offering integration toolkits and compliance modules.

- Pricing and spreads as retirement-grade vehicles scale and compete with ETF wrappers.

- Banking access for crypto firms if the “debanking” review yields supervisory changes, reducing operational bottlenecks.

Conclusion

The U.S. retirement market just opened a policy door that had been stuck for years. The Executive Order doesn’t force crypto into 401(k)s; it makes it realistically possible for prudent, diversified exposure to emerge under ERISA standards. Between DOL’s return to neutrality and the SEC’s marching orders to facilitate participant access, the regulatory vector has shifted from “no” to “how.”

For crypto, that means the prospect of persistent, programmatic demand from long-horizon savers—even if it starts small and grows slowly. For fiduciaries, it means more choice alongside more responsibility to implement disciplined process, education, and risk control. For builders, it’s the clearest signal yet to ship retirement-grade products with institutional custody, low fees, and seamless plan integration.

If participants can capture the upside of a new asset class while plan sponsors preserve the safeguards of ERISA, the outcome could be a milestone in mainstreaming digital assets—measured not in headlines, but in the steady cadence of paychecks invested on autopilot.