Main points :

- The FDIC has proposed a formal application-and-approval process for FDIC-supervised banks that want to issue payment stablecoins via subsidiaries, implementing the new GENIUS Act framework.

- The proposal bakes in clear statutory timelines (including 30-day completeness review and a 120-day decision clock), and includes an appeal path if denied.

- This is positioned as a “first step,” with FDIC leadership signaling additional standards for stablecoin-issuing subsidiaries may follow.

- Stablecoins are now a $280B+ market, heavily dominated by USDT and USDC, creating pressure for regulated “bank-grade” entrants to differentiate on compliance, distribution, and settlement integrations.

- In parallel, major payment rails are moving: Visa has announced stablecoin settlement availability for U.S. banks using USDC, reinforcing the “payments first” narrative.

1) What the FDIC proposed and why it matters now

In mid-December 2025, the U.S. Federal Deposit Insurance Corporation (FDIC) approved and published a notice of proposed rulemaking to implement the application provisions of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act). The stated purpose is practical: if an FDIC-supervised insured depository institution wants to issue a payment stablecoin, the GENIUS Act contemplates doing so through a subsidiary, and the FDIC is proposing the procedural “how” for that approval pathway.

Why this matters is less about a single rulemaking and more about institutionalizing a repeatable process. Over the past several years, stablecoins have moved from crypto-native settlement chips to key infrastructure for exchanges, on-chain trading, cross-border transfer corridors, and now—more visibly—merchant and bank payment experiments. Yet “stablecoin issuance” has often been associated with nonbank entities and a patchwork of state and federal touchpoints. The FDIC proposal is aimed at making stablecoin issuance by FDIC-supervised institutions legible as a regulated banking activity, with prescribed filings, review standards, and timelines.

Importantly, the proposal described in your source is not an abstract policy memo; it is framed as the first official rule proposal flowing from the GENIUS Act’s new stablecoin regime, and it is built around a subsidiary model that attempts to separate stablecoin activities from the bank’s core balance sheet and operations through organizational structure and supervisory approval.

2) The core mechanism: “issue via a subsidiary, but only with FDIC approval”

The proposal centers on a simple gate: if an FDIC-supervised institution wants to issue payment stablecoins through a subsidiary, it must apply to the FDIC and receive approval for that subsidiary to be treated as a permitted payment stablecoin issuer under the GENIUS Act framework.

The filing is expected to be detailed. While the exact content requirements can be extensive (and will be refined through the public-comment process), the direction is consistent: the regulator wants enough information to evaluate safety and soundness, governance, customer arrangements, and how the stablecoin activity is controlled within the corporate group—especially because stablecoins combine payments, custody-like functions, reserve management, and technology/operational risk in one product surface.

This matters to builders and investors because “bank-issued payment stablecoin” is not just a new issuer type—it can reshape distribution. Banks already have customer bases, compliance programs, deposit funding, and integration points into payment ecosystems. If they can issue stablecoins in a way that passes supervisory scrutiny, you can see second-order effects: wallet providers integrate “regulated bank stablecoins,” payment processors prefer them for certain flows, and on-chain liquidity venues list them as a premium collateral type.

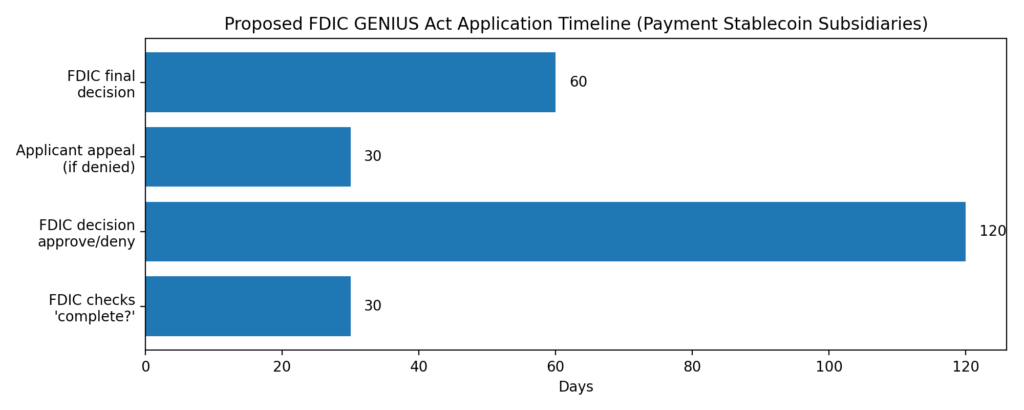

3) The timelines: predictable clocks and an appeals path

A central feature of the FDIC proposal is the timeline discipline, which mirrors statutory requirements.

FDIC GENIUS Act application timeline

- Within 30 days, FDIC notifies the applicant whether the application is “substantially complete” (i.e., whether it contains the required information to start the formal decision clock).

- Within 120 days after the application is deemed substantially complete, FDIC must approve or deny.

- If denied, the proposal includes a written explanation and a 30-day window for the applicant to appeal, followed by a 60-day window for a final determination.

Why should crypto-market readers care about bureaucratic clocks? Because time-to-market is a competitive weapon. For a bank (or a consortium backing one), a clear maximum pathway reduces uncertainty. For stablecoin infrastructure providers (wallets, risk tools, compliance services, custody tech, oracle feeds), predictable timelines help plan enterprise sales cycles and integration roadmaps. In a market where stablecoin velocity and network effects matter, procedural clarity can be as important as capital.

4) “First step” language: more standards likely coming

Acting FDIC Chairman Travis Hill has framed the proposal as an enabling step that still preserves a safety-and-soundness filter. In his public statement for the Board meeting, the framing emphasizes evaluation of proposed payment stablecoin activities while managing regulatory burden—suggesting the FDIC wants to avoid an unstructured rush but also wants a usable path for compliant entrants.

Your referenced Japanese write-up also notes the expectation of additional proposals addressing the management and control standards for subsidiaries issuing payment stablecoins. That direction matches how financial regulation typically matures: first define the process and jurisdiction, then progressively clarify the substantive expectations (controls, auditability, reserve governance, operational resilience, disclosures, and potentially interoperability and redemption standards).

For entrepreneurs hunting “new revenue sources,” this staging matters. Early movers might gain distribution advantages, but later clarifications can change compliance costs. Product strategy should assume that “minimum viable compliance” today may not be the terminal state—especially if stablecoin issuance becomes systemically important in payments.

5) Market context: stablecoins are already $280B+, and dominance is concentrated

Even before bank issuance scales, stablecoins have become one of the largest recurring cash-flow engines in crypto, mostly via reserve yield and payment/network distribution. The European Central Bank recently noted that combined stablecoin market capitalization has exceeded $280 billion, with USDT at about $184B (63%) and USDC at about $75B (26%), leaving a relatively small share for all others combined.

This concentration has two implications:

- Liquidity gravity is real. Most exchanges, OTC desks, and cross-chain bridges default to the dominant units because they minimize slippage and maximize counterparties.

- Regulated differentiation becomes the wedge. A bank-issued payment stablecoin will not win by being “just another dollar token.” It would need to win on trust, distribution, integration, and legal clarity—precisely the dimensions regulators and payment networks emphasize.

6) “Payments first” is getting reinforced by the rails: Visa’s USDC settlement move

Regulatory clarity matters most when it meets real distribution. One reason stablecoin narratives are shifting from “trading collateral” toward “payments infrastructure” is that large networks are testing and productizing settlement. Visa has announced stablecoin settlement availability for U.S. banks using USDC, with named early participants and a rollout trajectory.

For stablecoin builders, the deeper point is not “Visa likes a coin.” It’s that settlement utility is becoming an enterprise feature: 24/7 movement, reduced cut-off constraints, and potential operational resilience during weekends and holidays. That creates an environment where bank-issued payment stablecoins could become attractive as a compliance-aligned settlement medium—especially if their reserve and redemption models are regulated and exam-ready.

7) Practical opportunities for readers seeking new crypto assets and revenue models

If your audience is looking for “the next asset” or “the next yield,” a bank-issued payment stablecoin regime changes the opportunity map, but not always in the most obvious way.

A) Picks-and-shovels: compliance, risk, and operational infrastructure

If more banks pursue stablecoin issuance, they will need enterprise-grade tooling: transaction monitoring, sanctions screening, fraud analytics, key management, proof-of-reserves workflows, incident response, wallet allowlisting/denylisting controls, and on-chain/off-chain reconciliation. These vendors can generate sticky revenue without taking direct market risk.

B) Wallet UX: making stablecoins “feel like money” across chains and rails

Non-custodial wallet teams (especially those building transparent swap UX and settlement visibility) can benefit if banks introduce stablecoins that have clearer legal status and predictable redemption. The UX battle shifts toward: “Which wallet makes it easiest to use stablecoins across L1s, L2s, and payment network endpoints while keeping compliance signals intact?”

C) Tokenized deposits vs. payment stablecoins

The proposal’s mention of broader clarification for digital assets and tokenized deposits signals a likely competitive space: tokenized deposits may appeal to banks because they resemble existing liabilities, while payment stablecoins may appeal to open-network settlement use cases. Builders should watch which model gains more institutional support and what interoperability rules emerge.

8) What to watch next

The FDIC is soliciting public comment, and finalization will depend on that process and the federal register timeline, but a few watch items are immediate:

- How strict “substantially complete” becomes in practice. If completeness standards are too heavy, the 30-day check can become the real bottleneck.

- Whether additional subsidiary governance standards arrive quickly. FDIC leadership has indicated more is coming; the content will shape compliance cost curves.

- How payment networks and bank consortia choose settlement chains. Visa’s USDC move highlighted Solana in early usage; future bank-issued stablecoins may choose different rails depending on throughput, privacy, and integration requirements.

- How market structure reacts. Dominant stablecoins retain liquidity moats, but regulated bank-issued entrants could win specific corridors (payroll, B2B settlement, merchant acquiring) where compliance assurances are worth more than DeFi composability.

Conclusion

The FDIC’s proposed rule under the GENIUS Act is best understood as a “plumbing” milestone: it creates a procedural bridge between regulated banking and payment stablecoin issuance by requiring banks to operate through approved subsidiaries and by imposing explicit review timelines and an appeal mechanism.

For the broader crypto industry, the signal is that stablecoins are continuing their shift from a crypto-market convenience into a regulated payments instrument, at a time when stablecoins already exceed $280B in total market capitalization and are heavily concentrated in USDT and USDC. In that environment, the most durable opportunities may not be “another dollar token,” but the infrastructure, UX, compliance automation, and settlement integrations that make stablecoins usable at scale—especially when banks and payment networks start treating them as normal operational tools rather than experimental side projects.