Main Points :

- The Financial Action Task Force (FATF) warns that peer-to-peer (P2P) transactions involving stablecoins are increasingly used to evade VASP monitoring.

- Stablecoins’ high liquidity and cross-border mobility make them attractive for illicit financial flows.

- FATF is urging stablecoin issuers to implement safeguards such as asset freezing mechanisms and deny lists.

- Differences in regulatory enforcement across jurisdictions create global loopholes in AML enforcement.

- The report may influence future stablecoin regulation, including Travel Rule expansion and stronger oversight of issuers.

1. FATF Raises Alarm Over Stablecoin P2P Transactions

The Financial Action Task Force (FATF), the international body responsible for setting global standards to combat money laundering and terrorist financing, recently released a new report highlighting emerging risks in the cryptocurrency ecosystem. The report focuses particularly on stablecoins and unhosted wallets, warning that peer-to-peer (P2P) transactions are increasingly being used to bypass regulatory monitoring.

Stablecoins—digital assets pegged to fiat currencies such as the U.S. dollar—have become one of the fastest-growing segments of the crypto economy. Their stability and liquidity make them ideal for payments, trading, and decentralized finance (DeFi). However, these same attributes also make them attractive tools for illicit finance.

According to the FATF report, P2P transactions conducted without centralized intermediaries may allow individuals to move funds outside the oversight of Virtual Asset Service Providers (VASPs). Since many regulatory frameworks rely on VASPs to enforce compliance measures such as Know-Your-Customer (KYC) and Anti-Money Laundering (AML) monitoring, direct wallet-to-wallet transfers can undermine these controls.

In particular, the report notes that stablecoins are increasingly used as a settlement layer in cross-border transactions, making them especially appealing for actors seeking to move funds rapidly and discreetly across jurisdictions.

2. Stablecoins: Liquidity and Risk in Equal Measure

The rapid growth of stablecoins over the past five years has fundamentally reshaped the cryptocurrency market. As of early 2026, the total market capitalization of stablecoins has surpassed $180 billion, with major issuers such as USDT, USDC, and newer algorithmic models dominating trading pairs across centralized and decentralized exchanges.

Because stablecoins maintain a relatively stable value, they have become essential infrastructure for:

- Cryptocurrency trading liquidity

- Cross-border payments

- DeFi lending and liquidity pools

- On-chain settlements for institutions

However, FATF notes that the same characteristics—high liquidity, near-instant transferability, and global accessibility—also create systemic AML risks.

For example, stablecoins allow funds to move across multiple blockchains and decentralized platforms within minutes, often without traditional financial intermediaries. In cases where users transact directly between self-custody wallets, regulators have limited visibility into the origin or destination of funds.

This has raised concerns among policymakers that stablecoins could become parallel payment rails outside the regulated financial system if proper safeguards are not implemented.

3. FATF Calls for Asset Freezing and Deny Lists

To mitigate these risks, FATF recommends that stablecoin issuers actively implement technical safeguards, including:

- Asset freezing mechanisms to block suspicious accounts

- Deny lists that prevent transactions involving sanctioned addresses

- Compliance systems capable of responding to law enforcement requests

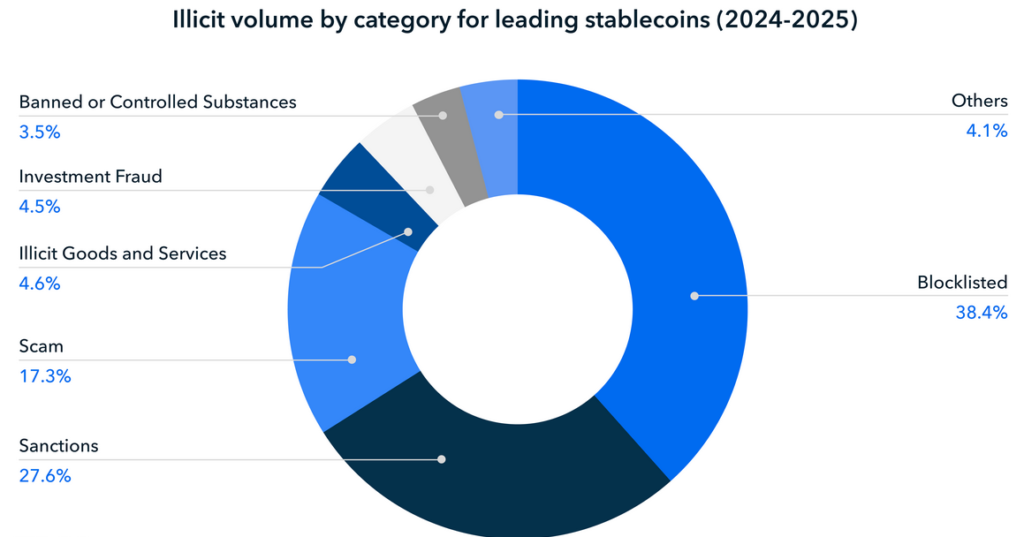

Several major stablecoin issuers have already adopted such tools. For example, some issuers maintain the ability to freeze tokens held in specific wallet addresses if they are linked to criminal activity.

These mechanisms have already been used in real-world cases involving ransomware payments, sanctions violations, and stolen funds.

However, FATF emphasizes that implementation remains uneven across the industry. While some stablecoin projects maintain strict compliance controls, others—particularly decentralized or algorithmic stablecoins—may lack centralized authority capable of enforcing freezes or deny lists.

This disparity creates regulatory blind spots that could be exploited by malicious actors.

4. Regulatory Fragmentation Creates Global AML Gaps

Another key issue highlighted in the report is regulatory fragmentation across jurisdictions.

While some countries have introduced strict stablecoin frameworks, others remain in early stages of regulatory development. This creates an environment where illicit actors can exploit differences between national regulatory systems.

For example:

- The European Union has implemented the MiCA (Markets in Crypto-Assets) regulation, establishing rules for stablecoin issuers.

- The United States is still debating stablecoin legislation in Congress.

- Several Asian jurisdictions—including Japan and Singapore—have introduced regulatory frameworks but with differing requirements.

These differences create opportunities for regulatory arbitrage, where companies and users shift activity to jurisdictions with weaker oversight.

FATF therefore urges countries to adopt consistent regulatory standards, particularly regarding AML compliance for stablecoins and unhosted wallets.

5. Expanding the Travel Rule to Self-Custody Wallets

One of the most controversial aspects of the report concerns the Travel Rule.

The Travel Rule requires VASPs to collect and transmit identifying information about the sender and recipient of digital asset transactions. The rule is designed to mirror similar requirements in traditional banking.

However, applying the Travel Rule to self-custody wallets remains extremely challenging.

Unlike centralized exchanges, self-custody wallets are controlled directly by users and may not involve any regulated intermediary. This raises fundamental questions:

- How can regulators enforce identity requirements in purely peer-to-peer systems?

- Should stablecoin issuers be responsible for enforcing compliance?

- Can blockchain analytics provide sufficient monitoring?

Several jurisdictions have proposed requiring exchanges to collect information when users send funds to self-custody wallets. However, critics argue that overly restrictive rules could undermine the core innovation of decentralized finance.

6. Industry Response: Balancing Innovation and Compliance

The cryptocurrency industry has responded cautiously to FATF’s recommendations.

Many industry participants agree that AML compliance is essential for long-term adoption, especially if stablecoins are to integrate with the global financial system.

At the same time, developers and blockchain advocates warn that excessive restrictions could slow innovation.

Stablecoins play an increasingly important role in:

- International remittances

- On-chain financial markets

- Digital dollar access in emerging economies

Restricting P2P functionality too aggressively could reduce the utility of stablecoins in these applications.

Some industry experts propose hybrid regulatory models, where compliance tools operate alongside decentralized infrastructure rather than replacing it.

For example:

- Compliance layers built into wallets

- Permissioned liquidity pools

- Identity-verified DeFi platforms

These models aim to preserve decentralization while satisfying regulatory requirements.

7. What This Means for Crypto Investors and Builders

For crypto investors and entrepreneurs, the FATF report signals an important shift.

Stablecoins are no longer just trading tools—they are becoming critical infrastructure for global finance.

As a result, regulators are paying increasing attention to how these systems operate.

For market participants, several trends are likely:

- Increased compliance requirements for stablecoin issuers

- Stronger integration between blockchain analytics and regulatory systems

- Greater scrutiny of self-custody wallet interactions

- New opportunities for compliance-focused blockchain infrastructure

Projects that can successfully bridge regulation and decentralization may emerge as the next major sector of the crypto industry.

Conclusion: The Next Phase of Stablecoin Regulation

The FATF report marks a turning point in the global regulatory conversation around stablecoins.

While the technology has unlocked new possibilities for payments, finance, and digital commerce, it also introduces risks that regulators cannot ignore.

Peer-to-peer transactions and self-custody wallets represent both the core innovation of blockchain and one of its greatest regulatory challenges.

Going forward, policymakers, developers, and financial institutions must work together to design frameworks that preserve innovation while preventing illicit financial activity.

The coming years will likely see the emergence of a new regulatory architecture for digital assets, where stablecoins play a central role in both the crypto ecosystem and the broader financial system.

For entrepreneurs and investors searching for the next opportunity in blockchain, understanding this evolving regulatory landscape will be just as important as understanding the technology itself.