Main Points :

- A group of 10 major European banks has formed a company (named Qivalis) to issue a euro-pegged stablecoin, targeting the second half of 2026 for launch.

- The move aims to counter U.S. dollar dominance in stablecoins and digital payments, offering a Europe-centric alternative and bolstering the region’s financial sovereignty.

- The stablecoin will be issued under the regulatory regime of MiCA, and the issuing entity (Qivalis) is applying for an electronic-money license from the Dutch central bank.

- The initiative reflects growing institutional adoption of crypto and tokenization in Europe, even as regulators such as European Central Bank (ECB) continue to evaluate risks of stablecoins — particularly their potential to disrupt bank deposits and financial stability.

Background and What Was Announced

In early December 2025, a consortium of ten prominent European banks — including ING, UniCredit and BNP Paribas — publicly confirmed they have formed a new company, Qivalis, headquartered in Amsterdam, to launch a euro-denominated stablecoin.

The company’s leadership will include former executives from major crypto firms: the CEO will be Jan‑Oliver Sell, previously the CEO of the German arm of Coinbase and with prior experience at Binance.

Qivalis plans to hire around 45–50 employees within the next 18–24 months — about one third of which are reportedly already on board.

The consortium aims to obtain an electronic-money institution (EMI) license from the Dutch central bank in the coming 6–9 months, with stablecoin issuance targeted for the second half of 2026.

Why Europe Is Doing This: Strategic Autonomy and Market Gaps

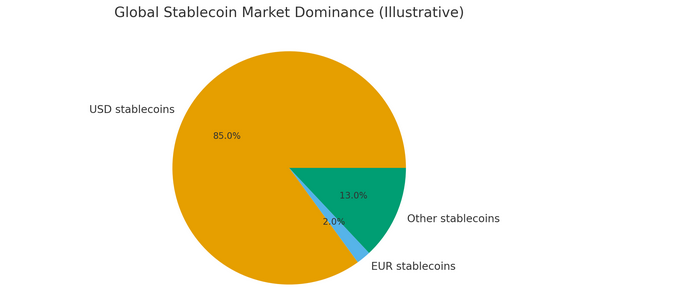

Countering Dollar Dominance

Globally, the stablecoin market remains overwhelmingly skewed toward U.S. dollar–pegged tokens. This dominance gives U.S.-based payment and crypto infrastructure providers disproportionate influence over global digital payments. The euro-stablecoin initiative is clearly positioned as a move to rebalance that dominance: by offering a euro-linked alternative backed by established European banks, the consortium hopes to preserve and strengthen Europe’s financial and payments sovereignty.

Exploiting Regulatory Opportunity: MiCA

The initiative comes at a moment when the regulatory environment in Europe has matured. The Markets in Crypto-Assets Regulation (MiCA), adopted by the European Union, became applicable to asset-referenced tokens and e-money tokens on June 30, 2024. This provides a clearer and more stable legal framework for fiat-backed stablecoins in Europe.

By building under MiCA and seeking an EMI license, Qivalis aims to deliver a compliant, institutional-grade stablecoin — likely improving trust among banks, enterprises, and large users who may be wary of unregulated tokens.

Institutional Adoption of Blockchain & Tokenization

The formation of Qivalis is more than just launching a new stablecoin — it signals a broader shift of traditional European banking institutions toward blockchain-based finance and tokenization. For users and firms interested in practical blockchain use cases, this could open the door to “real world” adoption: euro-denominated token settlements, cross-border payments within Europe, and on-chain settlement of tokenized assets or securities — all tied to regulated, legally compliant institutions.

Regulatory Risks and the Skepticism from Central Authorities

While the bank consortium’s move reflects growing confidence among banks, regulators remain cautious. The ECB has warned that privately issued stablecoins — especially if widely adopted — could siphon away retail deposits from banks, weakening their funding base and threatening financial stability.

There is also concern that in the event of a “run” on a stablecoin (mass redemption), the backers’ holdings of reserve assets — often short-term government securities — might be liquidated en masse, creating stress in global fixed-income markets, particularly in U.S. Treasuries.

Moreover, the region’s central bank digital currency (CBDC) project — the Digital Euro — continues to advance under the supervision of the ECB. The digital euro is designed not to replace cash or bank deposits, but to act as a publicly issued digital currency, complementing existing money and offering a pan-European payments infrastructure under public control.

This raises complex questions about how a private euro stablecoin will coexist with a public CBDC, especially in light of concerns over financial disintermediation, privacy, and systemic stability.

What This Means for Crypto Investors, Blockchain Developers, and Payment Innovators

For your audience — people hunting for new crypto assets, new revenue sources, or practical blockchain use cases — this development in Europe is potentially a major inflection point:

- Euro-denominated stablecoins may become investable and usable: A stablecoin issued by a consortium of large European banks under MiCA is likely to carry higher credibility, making it more attractive for institutional and retail users alike. For those interested in building or using blockchains, having a euro-backed stablecoin gives more options — beyond USD-backed tokens — for diversifying geographic risk and currency exposure.

- Use cases beyond trading — real payments & settlements: Because the project emphasizes instant, low-cost payments and settlement, the euro stablecoin could be used for cross-border payments in Europe, remittances, payrolls, and settlement of tokenized assets. For a blockchain wallet developer (as you are), this may present opportunities to support euro stablecoin transfers, integrate euro-wallets, or build services tailored to European users or businesses.

- Tokenization & financial infrastructure evolution: The involvement of traditional banks and compliance under MiCA suggest that tokenized assets, securities, or real-world assets could leverage euro stablecoin rails — potentially enabling efficient on-chain settlement, asset issuance, or DeFi-like services under regulatory compliance.

- Regulatory legitimacy and stability — but not risk-free: Because the stablecoin will be issued under MiCA and regulated by a central bank (through EMI licensing), it may achieve higher trust — but as regulators warn, stablecoins can still pose systemic risk if not designed or managed prudently. Users should stay attentive to reserve backing, transparency, and redemption mechanisms.

How This Fits Into Broader Trends (Including U.S. and Global Context)

- In the United States, regulatory clarity has also increased recently: new stablecoin legislation (e.g., under the GENIUS Act) enables banks and financial institutions to issue USD-backed stablecoins — contributing to the global dominance of dollar-pegged tokens.

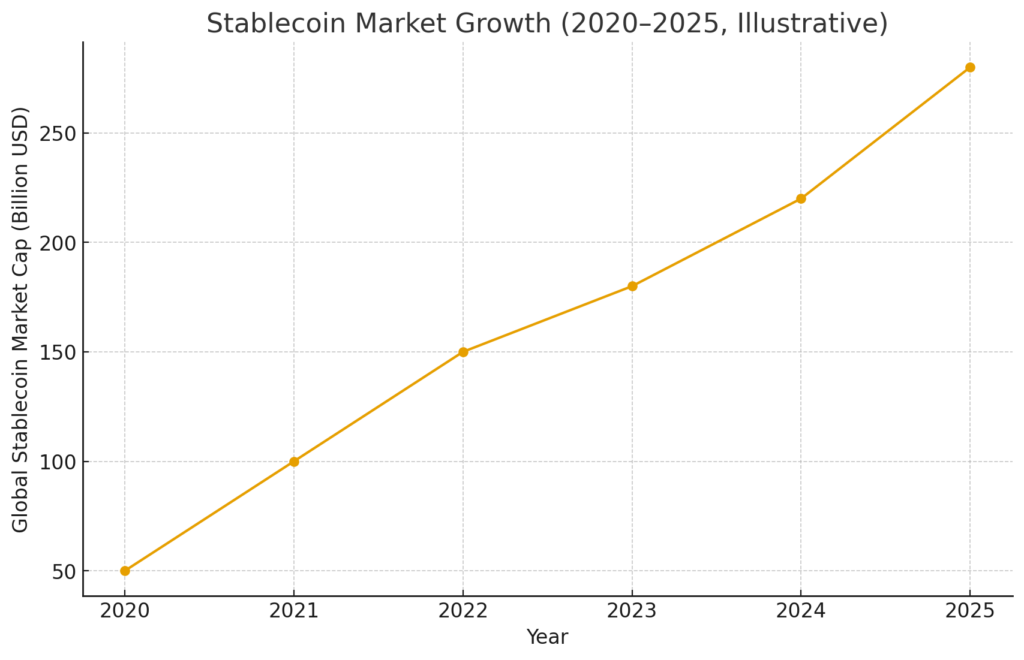

- Global stablecoin circulation has soared — as of late 2025, total market capitalization of stablecoins reportedly exceeds $280 billion.

- For Europe, the euro stablecoin initiative complements the push for a Digital Euro. The public CBDC is still expected no earlier than 2029 (pending legislative and technical work), so a privately issued euro stablecoin may sweet-spot the demand for euro-denominated, on-chain, digital payment solutions in the near-to-mid term.

Challenges and Key Uncertainties Ahead

- Regulatory Acceptance & Oversight: Getting the EMI license from the Dutch central bank is required before launch. Approval is not guaranteed, and regulatory scrutiny — especially over liquidity backing, reserve management, transparency, and systemic risk — may lead to delays or modifications in the plan.

- Competition or Conflict with Digital Euro: As the public CBDC of the Digital Euro progresses, regulatory bodies or policymakers may question whether a private euro stablecoin is needed or desirable. Potential overlap, regulatory friction, or even restrictions could arise.

- Adoption & Market Demand Risks: Historically, prior euro-denominated stablecoins have seen limited adoption. For example, a euro-stablecoin issued by a major French bank in 2023 reportedly had circulation of only about €64 million — a tiny fraction compared to dollar-based tokens.

- Systemic Risk and “Run” Danger: As highlighted by regulators like the ECB, stablecoins’ potential to draw deposits away from banks and to trigger redemptions en masse poses a risk not just to the issuer but to the broader financial system. If reserve assets are heavily weighted toward short-term securities (e.g., U.S. Treasury bills), liquidation pressure could ripple through global debt markets.

Conclusion: A Turning Point for European Crypto & Payments Infrastructure

The formation of Qivalis and the planned issuance of a euro-pegged stablecoin in 2026 by a group of major European banks marks a watershed moment — potentially the first time that mainstream financial institutions in Europe deploy blockchain-enabled digital money at scale. For the crypto ecosystem, this could open up a new frontier: euro-denominated stablecoins, regulated under MiCA, backed by established banks, and usable for real-world payments and tokenized asset settlement — offering a real alternative to USD-pegged tokens.

Yet the path forward is fraught with uncertainty. Regulatory hurdles, competition from public CBDC initiatives, adoption risk, and systemic financial stability concerns all remain open. For investors and builders, the key will be to watch how Qivalis designs its reserve, redemption, transparency, and compliance mechanism — and to evaluate whether the euro-stablecoin emerges as a trusted, liquid, and widely accepted medium, or remains a niche experiment.

For those of you exploring new crypto assets or blockchain-driven payment solutions, this development is one of the most significant moves in 2025–26. If euro-backed stablecoins take off, they could become a core building block for tokenized finance, cross-border business, and blockchain-based remittance or enterprise use — especially for Europe-linked markets or users who prefer euro-denominated assets.