Main Points :

- A consortium of 10 major EU banks plans to issue a MiCA-compliant euro-backed stablecoin by late 2026, operationally scaling by 2027.

- The issuing organization, Qivalis, is licensed under the Dutch Central Bank (DNB) and aims to provide a native euro instrument for on-chain settlement.

- The initiative comes as the U.S. prepares its own federal stablecoin law (GENIUS Act, effective July 2025)—structurally positioning the EU and U.S. for parallel regulatory races.

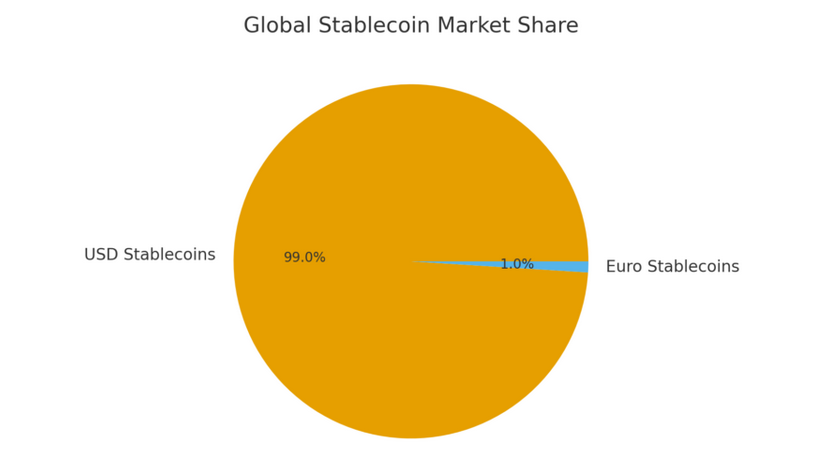

- The euro stablecoin market is currently tiny (<$407M) compared to USD stablecoins, accounting for <1% of global share.

- Tether (USDT issuer) has already halted EURt support in the EU due to MiCA compliance, leaving an open field for regulated banks.

- Risks remain: ECB and DNB warn of potential monetary policy impact as stablecoin adoption grows.

- For crypto investors and builders, this marks a major shift toward bank-issued tokenized money, expanding practical use cases for payments, DeFi, and real-world asset (RWA) rails.

1. Introduction: A Turning Point for Euro-Denominated Digital Money

Europe is accelerating toward a future where regulated banks—not crypto-native issuers—become the main producers of fiat-backed stablecoins. In a landmark announcement, BNP Paribas and nine other EU banks revealed that they aim to launch a euro-backed stablecoin by the second half of 2026, with operational scaling into 2027.

The issuing entity, Qivalis, headquartered in Amsterdam and licensed by the Dutch Central Bank (DNB), represents one of the most coordinated efforts yet to establish a MiCA-compliant, fully regulated stablecoin for the European Union.

This initiative is not simply about convenience; it is a strategic move to secure monetary sovereignty in the digital era, as global payment flows increasingly migrate to crypto, tokenized deposits, and distributed ledger technology (DLT).

2. Why Euro Stablecoins Matter Now

2.1 The Global Shift Toward Tokenized Money

The digital asset ecosystem is increasingly dependent on stablecoins, which serve as the settlement backbone for crypto markets, on-chain FX, cross-border payments, and emerging DeFi infrastructure.

However, nearly all major stablecoins are USD-denominated, including USDT, USDC, PYUSD, and GUSD.

In contrast:

- Euro stablecoin market cap: < €350M (~$407M)

- USD stablecoin market cap: > $150B

This structural imbalance means that European companies and consumers conducting on-chain transactions inevitably rely on a foreign currency, limiting monetary independence.

2.2 Growing Need for Local Currency Options

Qivalis CEO Jan-Oliver Sell describes the euro stablecoin initiative not as a convenience upgrade, but as:

“A matter of currency autonomy in a digital age.”

A MiCA-regulated euro stablecoin would allow:

- European companies to settle invoices on-chain in their domestic currency

- Consumers to interact with digital asset markets without USD exposure

- Banks to build tokenized deposits and programmable money rails

In many ways, this mirrors global trends toward CBDC-lite solutions, where private institutions issue digital money under strict regulatory supervision.

3. Regulatory Timing: EU and U.S. Are Now on Parallel Tracks

3.1 MiCA in the EU: The First Global Framework

MiCA (Markets in Crypto-Assets Regulation) became the world’s most comprehensive digital asset framework, requiring:

- Full reserve transparency

- Monthly reserve audits

- Strong governance and risk requirements

- Strict redemption obligations

This environment favors banks over crypto startups, since banks already meet capital, audit, and compliance requirements.

3.2 The United States: The GENIUS Act

In July 2025, the U.S. will activate its own federal stablecoin law, the GENIUS Act, signed by President Donald Trump.

Its purpose is to establish:

- Licensing for stablecoin issuers

- Reserve quality standards

- Federal oversight of payment stablecoins

The U.S. and EU are now moving in parallel, suggesting a global regulatory race that may reshape how stablecoins function across borders.

4. Market Implications: Opportunities and Risks

4.1 ECB and DNB Are Watching Carefully

Although euro stablecoins remain small today, central banks warn that stablecoins could:

- Fragment monetary policy transmission

- Create parallel money systems outside bank deposits

- Increase reliance on private issuers

The ECB’s November report concluded that existing risks are “limited,” but emphasized that rapid growth requires continued monitoring.

4.2 A Vacuum Left by Tether

Tether, the issuer of USDT, officially ceased redemption for its euro-backed EURt on November 25.

The company cited MiCA’s demanding compliance requirements.

This retreat leaves European banks with a clear open landscape, positioning Qivalis to dominate a market previously served mostly by crypto-native firms.

5. What This Means for Crypto Investors and Builders

5.1 New On-Chain Euro Liquidity Pools

A regulated euro stablecoin opens opportunities such as:

- EUR/USDC, EUR/USDT liquidity pools

- On-chain FX markets using automated market makers (AMMs)

- DeFi lending markets in EUR

- Arbitrage between traditional FX and DEX liquidity

Builders focused on multi-currency payment rails gain a new instrument to work with.

5.2 Real-World Asset (RWA) Settlements

European RWAs—such as tokenized bonds, invoices, or property—will benefit from:

- Euro-denominated settlement

- Lower FX exposure

- Regulated tokenized euro cash equivalents

This is critical for institutional adoption, especially for MiFID-regulated security token platforms.

5.3 Institutional DeFi and Enterprise Blockchain

Banks can integrate euro stablecoins into:

- On-chain treasury management

- Automated compliance frameworks

- Tokenized deposits

- Enterprise ERP integrations

This shift brings the EU closer to a hybrid financial system where DeFi, CeFi, and TradFi coexist.

6. Chart and Visualization

Below is a simple visualization comparing USD vs. EUR stablecoin dominance.

7. Conclusion: A New Era for Euro-Based Digital Assets

The EU’s coordinated move toward a fully regulated euro-backed stablecoin by 2026–2027 marks a potential turning point in global crypto finance. With MiCA setting strict standards and Tether exiting the euro market, European banks now have a unique opportunity to lead.

For investors and builders, this shift signals:

- New liquidity markets in EUR

- Faster institutional adoption

- Growing cross-border settlement options

- More diverse opportunities beyond USD-dominated ecosystems

If executed successfully, Qivalis may establish the euro as a major on-chain currency, reshaping how Europe participates in the next era of blockchain-based finance.