Main Points :

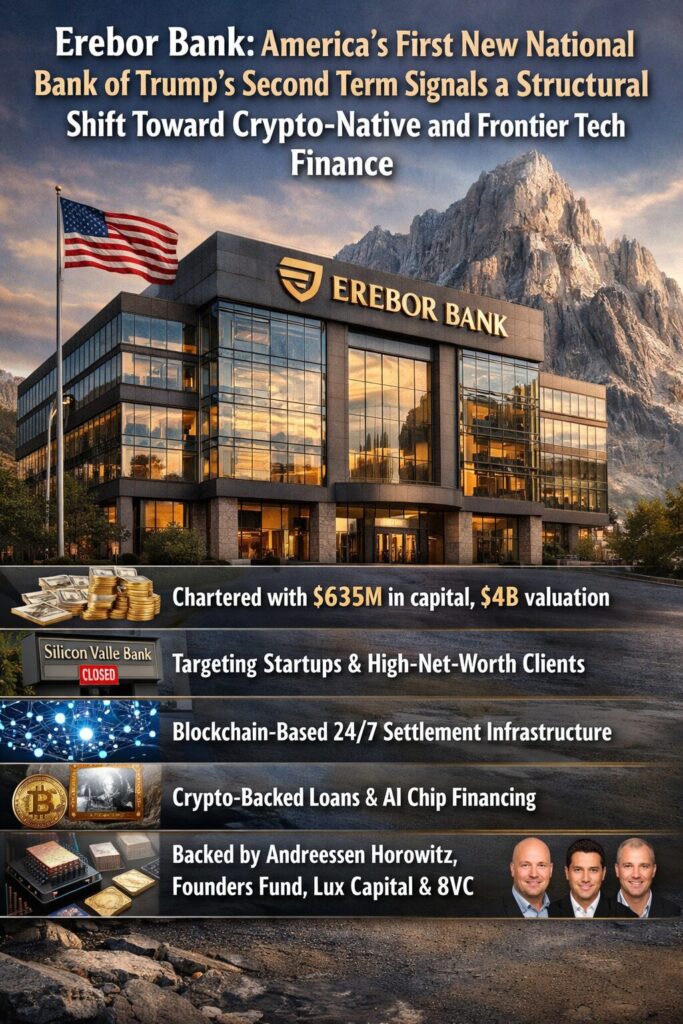

- The U.S. has granted its first new national bank charter of Trump’s second administration to Erebor Bank, a crypto- and frontier-tech-focused institution.

- Erebor launches with approximately $635 million in capital and a valuation that has reached $4 billion.

- The bank targets startups, venture-backed firms, and high-net-worth individuals underserved since the collapse of Silicon Valley Bank.

- Erebor plans to integrate blockchain-based 24/7 settlement infrastructure—an unusual move for a U.S. national bank.

- Strategic lending includes loans collateralized by crypto holdings, private securities, and financing for advanced AI chips.

- Backed by prominent investors including Andreessen Horowitz, Founders Fund, Lux Capital, 8VC, and Elad Gil.

1. The First New National Bank of Trump’s Second Term

In February 2026, the United States Office of the Comptroller of the Currency (OCC) granted a national bank charter to Erebor Bank, marking the first newly chartered national bank under President Donald Trump’s second administration. The development signals a potential policy recalibration toward innovation-oriented banking, particularly in sectors such as cryptocurrency, artificial intelligence, robotics, and advanced manufacturing.

Erebor Bank received authorization to operate nationwide. In parallel, the Federal Deposit Insurance Corporation (FDIC) approved deposit insurance, clearing one of the most critical regulatory hurdles for new banking entrants.

The bank begins operations with approximately $635 million in capital. Its investor base includes some of the most influential venture capital firms in Silicon Valley, such as Andreessen Horowitz and Founders Fund, as well as Lux Capital, 8VC, and Elad Gil. Founder Palmer Luckey, co-founder of Oculus, is involved as a visionary backer, though not in day-to-day operations.

This charter approval is not merely administrative. It reflects a broader shift in U.S. financial policy following years of regulatory tension between crypto firms and traditional banking institutions.

2. Filling the Post-Silicon Valley Bank Vacuum

In 2023, the collapse of Silicon Valley Bank (SVB) disrupted financial services for technology startups and venture-backed firms. While large commercial banks absorbed some clients, many early-stage, high-risk, or crypto-adjacent companies struggled to secure adequate banking relationships.

Erebor Bank positions itself as a direct response to that vacuum. Palmer Luckey described the institution as “an agricultural bank for technology,” implying that just as agricultural banks understand farmland and crop cycles, Erebor understands intangible assets such as intellectual property, private equity stakes, crypto holdings, and AI infrastructure.

Traditional banks often struggle to assess:

- Private, illiquid equity in startups

- Tokenized digital assets

- Revenue models dependent on decentralized protocols

- Hardware-heavy AI infrastructure requiring upfront chip procurement

By specializing in these asset classes, Erebor aims to institutionalize financing for frontier technologies.

For readers seeking the next revenue source in crypto or blockchain applications, this is a structural signal: capital markets are building regulated infrastructure around digital-native assets rather than suppressing them.

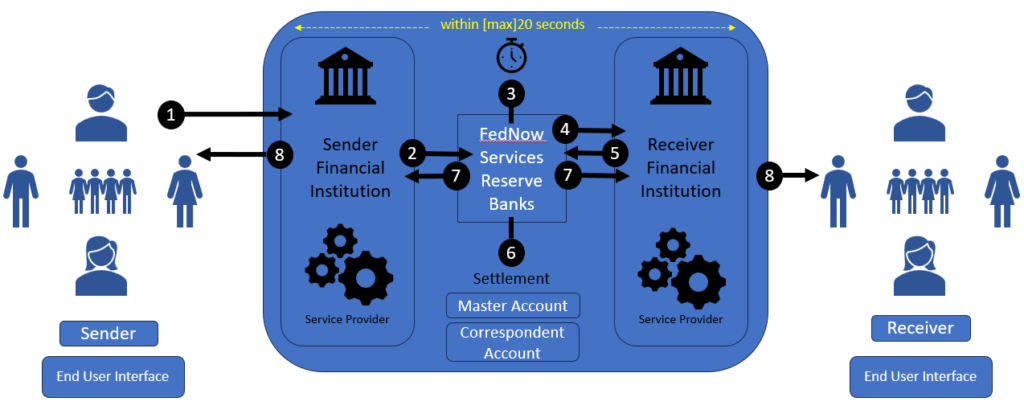

3. Blockchain-Based 24/7 Settlement Infrastructure

One of Erebor’s most ambitious initiatives is the integration of blockchain-powered settlement systems enabling 24/7 payments.

Unlike most U.S. banks, which operate on limited settlement windows and rely on legacy clearing systems, Erebor intends to integrate distributed ledger technology to enable near-instant transactions. While specific technical details have not been disclosed, such systems could involve:

- Tokenized deposit representations

- On-chain settlement rails for internal transfers

- Stablecoin-compatible liquidity layers

- Real-time reconciliation

[Traditional Banking Settlement vs. Blockchain 24/7 Settlement]

This structural shift mirrors broader industry movements. Over the past two years, major financial institutions have explored tokenized deposits and real-time blockchain settlement systems. Stablecoins such as USDC and tokenized treasury products have demonstrated that capital can move continuously without being constrained by banking hours.

For crypto-native entrepreneurs, the implication is clear: regulated banks are increasingly adapting to blockchain timing rather than forcing blockchain into legacy timeframes.

4. Strategic Lending: Crypto, AI Chips, and Private Securities

Erebor’s strategy includes lending collateralized by:

- Cryptocurrency holdings

- Private, pre-IPO equity

- High-performance AI chip inventory

This is significant. Traditional banks rarely accept crypto as collateral due to volatility and regulatory ambiguity. However, structured lending models using dynamic margin requirements, overcollateralization, and on-chain monitoring have matured within crypto-native platforms.

Similarly, AI infrastructure financing has become a bottleneck. Demand for high-performance GPUs—critical for machine learning—has surged dramatically. Startups often need millions of dollars upfront for hardware acquisition before generating revenue.

[AI Infrastructure Cost Structure vs. Traditional Startup Cost Model]

By financing chip acquisition, Erebor positions itself at the intersection of AI and capital markets. This hybridization of crypto collateral and hardware financing reflects a new asset-backed innovation economy.

5. Valuation Growth and Capital Backing

Erebor was conditionally approved by the OCC in October of the previous year. Shortly thereafter, it secured FDIC insurance approval. Its valuation trajectory is striking:

- Previous funding round: approximately $2 billion valuation

- Raised $350 million led by Lux Capital

- Current valuation: approximately $4 billion

For a newly chartered bank, this valuation suggests investor confidence not only in Erebor’s model but also in regulatory tailwinds.

The Trump administration’s second term appears to be taking a more permissive approach toward innovation-centric banking compared to previous periods characterized by aggressive scrutiny of crypto-related financial institutions.

6. Broader Industry Context: Crypto, Regulation, and Banking Convergence

In recent months, regulatory conversations in the United States have shifted toward clearer stablecoin frameworks and more structured crypto custody standards. Financial institutions are no longer debating whether digital assets belong in banking; instead, they are debating how to integrate them safely.

Key industry trends include:

- Expansion of tokenized real-world assets (RWAs)

- Institutional adoption of stablecoins for cross-border settlement

- Growing venture investment into AI-blockchain convergence projects

- Exploration of central bank digital currencies (CBDCs), though politically contentious

Erebor Bank’s launch aligns with these structural changes. It represents not merely a bank but a regulated gateway into high-volatility, high-growth sectors.

For investors and operators seeking the next crypto revenue opportunity, this signals that infrastructure-level plays—custody, lending, tokenized deposits, and AI-collateral financing—may offer more sustainable yield than speculative token cycles alone.

7. Implications for Crypto Investors and Blockchain Builders

For crypto-focused readers, several implications emerge:

- Regulatory Legitimization – A national bank charter integrating blockchain systems reduces systemic hostility toward digital assets.

- Collateral Evolution – Crypto holdings are increasingly treated as financeable assets rather than speculative anomalies.

- Infrastructure as Yield – The next revenue wave may lie in payment rails, settlement layers, and regulated crypto-backed credit.

- AI–Crypto Convergence – Capital allocation toward AI hardware intersects with tokenized asset financing.

This convergence suggests that future crypto projects should consider compliance-first design, stablecoin interoperability, and real-world asset integration.

Conclusion: A Structural Repricing of Frontier Finance

Erebor Bank’s national charter is more than a regulatory milestone. It represents a structural repricing of frontier technologies within the U.S. financial system.

After the shock of Silicon Valley Bank’s collapse, the ecosystem demanded specialized financial infrastructure. Erebor answers that demand by combining:

- Venture-capital DNA

- Crypto-native settlement technology

- AI and robotics sector expertise

- Regulatory legitimacy through OCC and FDIC approval

Its $4 billion valuation underscores market belief that the next era of banking will not reject blockchain—it will integrate it.

For readers searching for the next revenue stream, the message is strategic rather than speculative: value creation is migrating toward regulated digital-asset infrastructure, AI capital financing, and 24/7 programmable banking rails.

In the coming years, the dividing line may not be “crypto vs. banks,” but rather “legacy banks vs. crypto-integrated national banks.”

Erebor Bank may be the first visible prototype of that new category.