Main Points :

- Mastercard launched a global crypto partnership program bringing together 85+ digital asset companies.

- The initiative aims to integrate blockchain infrastructure with traditional payment networks.

- Key partners include Binance, Circle, Gemini, Paxos, Ripple, PayPal, Polygon, Solana, Crypto.com, MoonPay, and Fireblocks.

- Focus areas include international remittances, payment processing, and commercial payments.

- The program reflects a wider trend where major payment networks like Mastercard and Visa are embracing stablecoins and tokenized assets.

- Nearly 30% of Mastercard’s transactions were tokenized in 2024, signaling rapid adoption of digital asset infrastructure.

Introduction

The global payments industry is entering a transformative period. For decades, international financial infrastructure has been dominated by card networks, correspondent banking systems, and centralized payment processors. However, the rapid rise of blockchain technology and digital assets is reshaping how money moves across borders.

Recognizing this shift, Mastercard has launched a global cryptocurrency partner program involving more than 85 companies across the digital asset ecosystem. The initiative aims to bridge the gap between traditional financial infrastructure and blockchain-based payment systems.

Participants include major cryptocurrency exchanges, blockchain networks, stablecoin issuers, and infrastructure providers. Among the most notable partners are Binance, Circle, Gemini, Paxos, Ripple, PayPal, Polygon, Solana, Crypto.com, MoonPay, and Fireblocks—companies representing virtually every layer of the digital asset stack.

This collaboration is not simply a technology experiment. Instead, it represents a strategic push to develop real-world payment applications powered by blockchain, including international remittances, corporate payments, and merchant settlement.

For investors and entrepreneurs seeking the next revenue opportunities in crypto, the move signals something important: the era of speculative crypto markets is gradually evolving into an era of infrastructure-driven blockchain finance.

1. The Mastercard Crypto Partner Program

Mastercard’s newly announced partnership initiative is designed to bring together a broad coalition of blockchain companies and financial service providers to build next-generation payment systems.

Unlike earlier crypto experiments that focused mainly on consumer wallets or speculative trading, this program targets core financial infrastructure.

The participating companies span multiple segments of the digital asset ecosystem:

Crypto Exchanges

- Binance

- Gemini

- Crypto.com

Stablecoin Issuers

- Circle

- Paxos

Blockchain Networks

- Polygon

- Solana

Infrastructure Providers

- Fireblocks

- MoonPay

Financial Platforms

- PayPal

The goal is to combine these technologies with Mastercard’s existing payment network, which processes billions of transactions annually in more than 210 countries and territories.

According to Mastercard, the program will focus on developing solutions for:

- International remittances

- Payment processing

- Business-to-business (B2B) payments

- Merchant settlement

- Digital asset settlement layers

This reflects a growing realization that blockchain technology is no longer just an experimental tool but a practical financial infrastructure capable of supporting large-scale payment systems.

Image Insertion Location

Insert the following diagram after this section.

2. Why Blockchain Payments Are Becoming Critical

One of the main drivers behind Mastercard’s initiative is the growing demand for faster and cheaper cross-border payments.

Traditional international transfers often rely on correspondent banking networks such as SWIFT, which can take several days to settle transactions and involve multiple intermediary banks.

Blockchain networks, by contrast, can enable:

- Near-instant settlement

- Lower transaction costs

- 24/7 payment availability

- Programmable financial logic

For example, stablecoins—digital tokens pegged to fiat currencies—have become a particularly important tool in this transformation.

Stablecoins allow users to send digital dollars across the world in seconds while maintaining price stability. The total market value of stablecoins has exceeded $150 billion, and daily settlement volumes often rival major payment networks.

Companies like Circle (issuer of USDC) and Paxos are central to this ecosystem, which explains their participation in Mastercard’s program.

For payment networks, stablecoins offer a powerful opportunity: combine blockchain settlement speed with existing global payment acceptance infrastructure.

3. The Rise of Tokenized Payment Infrastructure

Mastercard has already been experimenting with tokenization across its network.

According to the company, approximately 30% of its transactions in 2024 were tokenized, meaning sensitive card information was replaced with secure digital tokens.

Tokenization improves both security and efficiency by ensuring that payment credentials cannot be easily stolen or reused.

Blockchain technology represents a natural extension of this concept.

Instead of tokenizing only payment credentials, blockchain systems can tokenize:

- currencies

- securities

- real-world assets

- payment obligations

This broader form of tokenization is often referred to as tokenized finance.

Under such systems, payments could eventually settle directly on blockchain networks while still leveraging traditional financial institutions.

This hybrid architecture—traditional payment rails combined with blockchain settlement layers—is increasingly seen as the likely future of global finance.

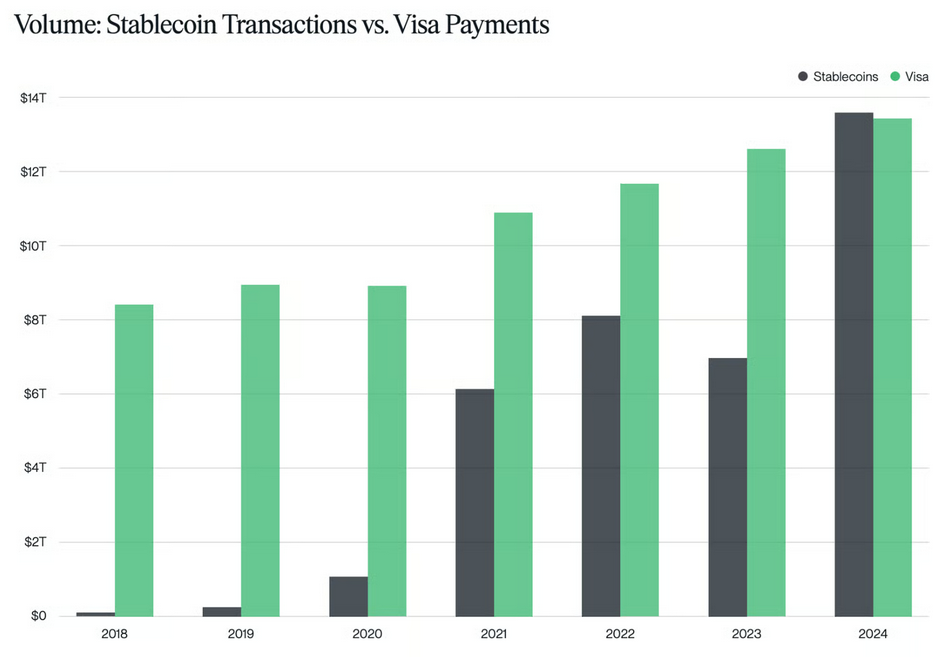

4. Visa and Mastercard Compete in the Stablecoin Race

Mastercard’s initiative also reflects intensifying competition with rival payment network Visa, which has been expanding its own blockchain strategy.

In September, Visa launched a pilot program enabling banks to pre-fund cross-border transfers using stablecoins via the Visa Direct platform.

The goal was to allow financial institutions to complete international transfers almost instantly instead of waiting days for settlement.

Shortly afterward, Visa expanded its digital asset services by supporting additional stablecoins across several blockchain networks, including:

- Ethereum

- Solana

- Stellar

- Avalanche

These developments highlight a growing industry consensus: stablecoins may become a core component of future payment systems.

For payment networks, integrating stablecoins is less about competing with crypto companies and more about adapting their infrastructure to a rapidly evolving financial landscape.

Image Insertion Location

Insert this chart after this section

5. Real-World Payment Applications

The Mastercard partnership program emphasizes practical financial use cases rather than speculative crypto trading.

Among the most promising applications are:

International Remittances

Remittances represent a $800+ billion global market. Traditional remittance services often charge fees of 5–10%.

Blockchain-based payment rails could significantly reduce those costs.

Merchant Payments

Cryptocurrency payment cards already allow users to spend digital assets at traditional merchants.

With deeper blockchain integration, merchants could eventually receive stablecoin settlements directly, eliminating currency conversion costs.

Corporate Payments

Large enterprises conducting cross-border trade face significant settlement delays.

Blockchain-based payment infrastructure could enable instant B2B settlement, improving liquidity management.

Programmable Payments

Smart contracts allow financial transactions to be automated based on predefined rules.

This could enable advanced financial products such as:

- escrow payments

- automated payroll

- supply chain financing

These applications illustrate how blockchain could evolve from a speculative asset class into a core financial infrastructure layer.

6. What This Means for the Crypto Industry

The Mastercard partnership signals a major shift in how traditional finance views digital assets.

In the early years of cryptocurrency, many financial institutions were skeptical or openly hostile toward blockchain technology.

Today, the conversation has changed.

Instead of debating whether crypto should exist, major financial companies are asking how blockchain can improve existing financial systems.

This shift creates new opportunities across the digital asset ecosystem.

Infrastructure providers, compliance platforms, custody providers, and stablecoin issuers may become critical components of the next generation of financial infrastructure.

For investors and entrepreneurs, the most important insight may be this:

The biggest opportunities in crypto may no longer come from speculation, but from building the infrastructure that powers global finance.

Conclusion

Mastercard’s global partnership with more than 85 crypto companies represents one of the most ambitious attempts yet to integrate blockchain technology into mainstream financial infrastructure.

By bringing together exchanges, stablecoin issuers, blockchain networks, and payment providers, the initiative aims to create a new generation of payment systems capable of operating alongside—and eventually enhancing—traditional financial networks.

At the same time, competing efforts by Visa and other payment giants demonstrate that the race to build the future of digital payments is accelerating.

As stablecoins, tokenization, and blockchain settlement continue to mature, the financial system may evolve into a hybrid architecture combining traditional institutions with decentralized technologies.

For the broader crypto ecosystem, this development marks a turning point. Blockchain is no longer merely an alternative financial experiment—it is increasingly becoming a foundational layer of the global payment economy.