Main Points:

- Legislative Initiative: Senator Cynthia Lummis’s 21st Century Mortgage Act would codify an FHFA order requiring Fannie Mae and Freddie Mac to treat unconverted cryptocurrency as eligible assets in mortgage applications.

- Political Debate: While Republicans highlight innovation and wealth-building for younger, digitally savvy Americans, Senate Democrats urge a comprehensive risk assessment of crypto’s volatility and liquidity challenges.

- Impact on Millennials and Gen Z: With only 36.6 % of Americans under 35 owning homes in Q1 2025, the bill aims to broaden access by allowing crypto collateral without forced conversion to dollars.

- Comparative Developments: A parallel proposal in the House (the “Modernizing American Homeownership through Cryptocurrency Act”) and Australia’s Block Earner pilot illustrate growing global momentum for crypto-backed lending.

- Market Context & Future Outlook: Amid low homeownership and high interest rates, integrating crypto could reshape underwriting—but requires robust guardrails to balance innovation with consumer protection.

Introduction

In late July 2025, Wyoming Senator Cynthia Lummis introduced the 21st Century Mortgage Act, seeking to embed digital assets into U.S. mortgage underwriting standards. This legislation would transform a June 2025 Federal Housing Finance Agency (FHFA) directive—mandating that Fannie Mae and Freddie Mac consider cryptocurrency as assets—into binding law. Proponents argue the move modernizes lending by recognizing how younger Americans build wealth, while critics warn that crypto’s pronounced price swings and limited liquidity could imperil loan repayment.

Legislative Background

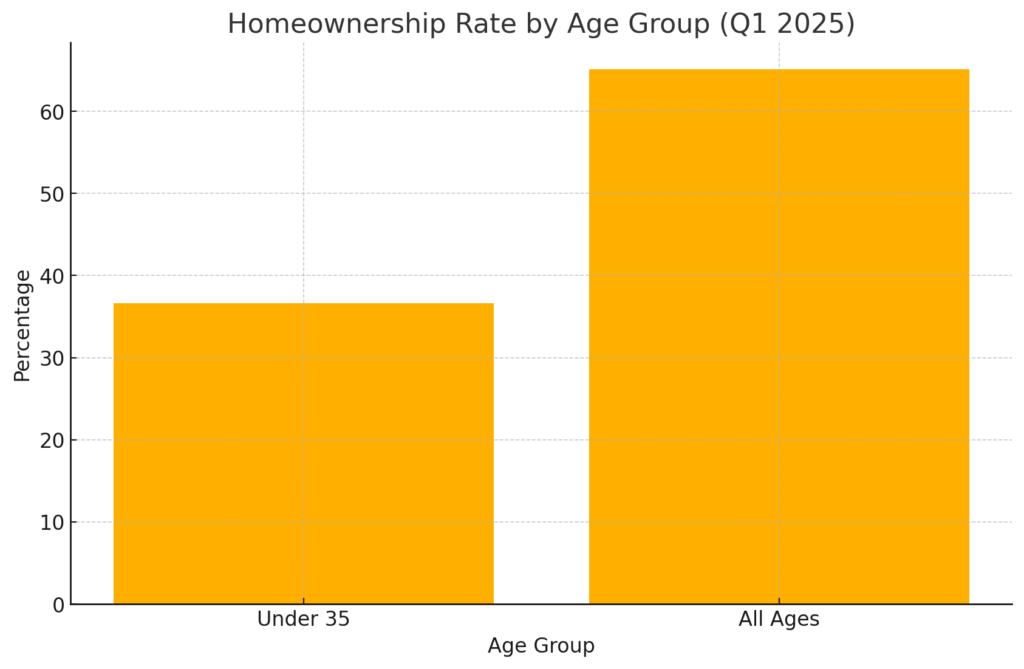

Following FHFA Director William Pulte’s June 2025 order, which instructed Fannie Mae and Freddie Mac to allow crypto holdings in single-family mortgage calculations, Senator Lummis formalized the rule through her bill. The order responded to a surge of digital asset adoption among younger cohorts; a Federal Census Bureau report showed just 36.6 % homeownership among Americans under 35 in Q1 2025, compared to 65.1 % overall (see Figure 1).

<Insertion Point: Figure 1 – Homeownership Rate by Age Group (Q1 2025) {image file: homeownership_rate_q1_2025.png}>

Key Provisions of the 21st Century Mortgage Act

- Asset Recognition: Mortgage lenders and GSEs (Fannie Mae, Freddie Mac) must include unconverted crypto holdings as part of a borrower’s asset portfolio.

- Valuation Standards: Digital assets would be valued using market prices on U.S.-regulated exchanges at the time of application.

- Disclosure Requirements: Borrowers must demonstrate the origin, storage, and ownership of crypto assets via exchange statements or wallet proofs.

- Risk Reserve Buffers: Lenders would apply conservative “haircuts” to crypto valuations—e.g., valuing Bitcoin at 70 % of its market value—to offset potential volatility.

By codifying these details, the bill seeks to ensure clarity for originators, servicers, and regulators, reducing uncertainty in underwriting procedures.

Opposition and Concerns

Senate Democrats, including Senators Merkley, Warren, Sanders, Van Hollen, and Hirono, pushed back via a July 24 letter to Director Pulte, urging a full-cost analysis of crypto integration. They cautioned that:

- Volatility Risks: Historic swings—e.g., Bitcoin’s ±30 % price moves in weeks—could leave borrowers unable to liquidate in downturns, heightening default risk.

- Liquidity Constraints: Unlike cash or securities, large crypto positions may not be saleable instantly without market impact.

- Systemic Stability: Rapid adoption without proper guardrails could destabilize mortgage markets, echoing asset-backed securities excesses of 2008.

This opposition highlights the tension between fostering innovation and safeguarding financial stability.

Impact on Young Homebuyers

For many Millennials and Gen Zers—who tend to hold a larger portion of wealth in digital form—this legislation could unlock new mortgage pathways. According to a survey, 21 % of U.S. adults own crypto, with nearly two-thirds under age 45. By allowing collateralization of assets without forced conversion, borrowers can:

- Retain upside potential if crypto appreciates after closing

- Avoid transaction fees and settlement delays from large sell-offs

- Demonstrate broader net-worth measures beyond traditional cash savings

Critics counter that younger buyers may over-leverage on volatile holdings, exposing them to jagged payment shocks if prices tumble.

Comparative Initiatives

House Proposal

On July 14, 2025, Representative Nancy Mace sponsored the “Modernizing American Homeownership through Cryptocurrency Act,” which similarly mandates mortgage lenders to factor crypto account values (e.g., exchange-linked securities accounts) into credit decisions. While aligned in intent, Mace’s bill emphasizes borrower disclosures and education programs.

Australian Pilot

Meanwhile, Australia’s Block Earner received Federal Court approval in July 2025 to launch a Bitcoin-backed mortgage, allowing borrowers to maintain crypto ownership as collateral. The product offers starting rates around 9.50 % with a 40 % loan-to-value ratio, scaling upward with higher LTVs. Proponents claim it boosts housing affordability by leveraging Bitcoin’s long-term growth; skeptics warn of borrower over-exposure to a single asset class.

Market Context and Future Outlook

As homeownership rates slip to multi-decade lows (65.1 % overall in Q1 2025) amid elevated mortgage rates (~7 %) and supply constraints, lenders and regulators seek methods to expand credit responsibly. Cryptocurrency integration is one of many strategies—others include flexible debt-to-income calculations and alternative income verifications (gig economy earnings, etc.).

The path forward hinges on developing robust valuation models, stress-testing scenarios, and clear disclosure regimes. Should Congress pass the bill—and FHFA and GSE boards adopt conforming operational guidelines—the U.S. could join a small cohort of jurisdictions recognizing crypto collateral in real estate finance.

Conclusion

The 21st Century Mortgage Act represents a landmark effort to modernize U.S. mortgage underwriting by acknowledging the growing role of digital assets in household wealth. Its success will depend on striking the right balance between innovation—broadening access for younger, crypto-rich borrowers—and prudence—ensuring market stability and consumer protection. Comparative lessons from legislative counterparts and pilots abroad will inform implementation, potentially ushering in a new era of asset-backed lending.