Main Points :

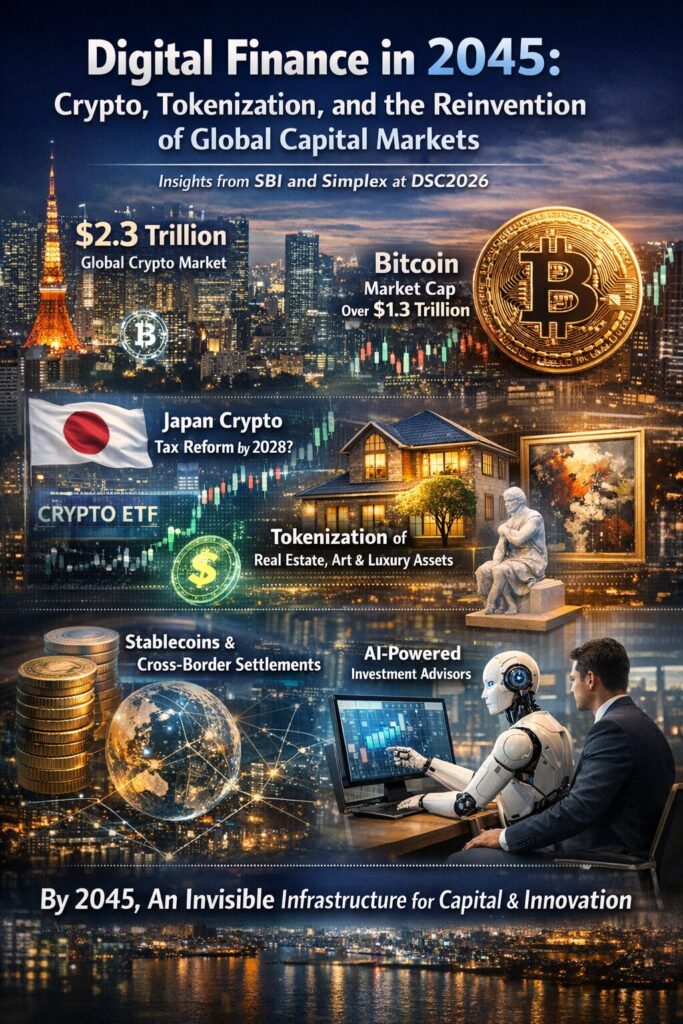

- The global crypto market has surpassed $2.3 trillion, rivaling the scale of the largest U.S. tech giants.

- Bitcoin alone exceeds $1.3 trillion in market capitalization, solidifying its role as a core portfolio asset.

- Japan is expected to reform crypto taxation by 2028, potentially paving the way for domestic crypto ETFs.

- Tokenization will extend beyond public equities into private assets such as real estate, art, music, film, and luxury goods.

- Stablecoins are emerging as the settlement layer for cross-border finance and tokenized securities.

- AI agents will optimize investment decisions, but human advisory roles will remain essential during regime shifts.

- By 2045, digital finance will become an invisible infrastructure enabling capital to flow toward creativity and innovation.

1. Crypto as a Mature Asset Class

At DSC2026, executives from SBI Global Asset Management and Simplex presented a clear message: crypto has crossed the threshold from speculation to structural integration within global finance.

The total cryptocurrency market capitalization has surpassed approximately $2.3 trillion, placing it in the same macro league as the combined valuation of major U.S. technology firms. Bitcoin alone accounts for roughly $1.3 trillion, a scale that fundamentally changes how institutional allocators perceive digital assets.

SBI’s leadership emphasized that Bitcoin can no longer be categorized as a fringe instrument. Instead, it should be evaluated alongside equities, bonds, and commodities within diversified portfolios. In the United States, spot Bitcoin ETFs approved by the SEC in early 2024 rapidly accumulated over $160 billion within two years. This pace of institutional adoption signals that digital assets are being normalized within retirement accounts and pension allocations.

Japan, by contrast, remains in transition. With approximately 14 million domestic crypto accounts—roughly half the number of NISA accounts—the retail foundation is already significant. Tax reform anticipated for 2028 could align Japan with global ETF structures, potentially catalyzing a structural reallocation of household savings into digital assets.

2. The Tokenization of Everything

One of the most transformative themes discussed was the tokenization of real-world assets (RWA). While public equities already trade electronically, blockchain enables a deeper evolution: fractional ownership, programmable rights, and global liquidity.

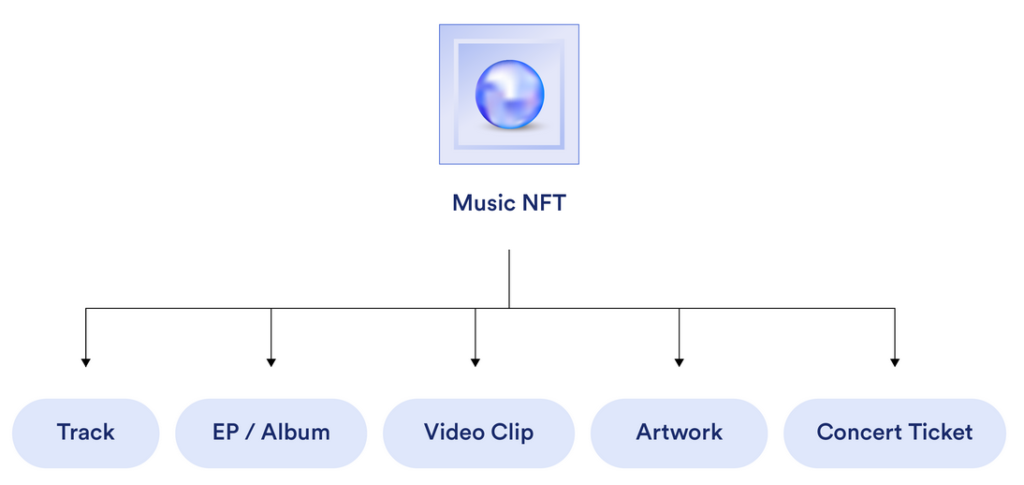

Tokenization will not be limited to listed stocks. Private equity, venture capital shares, real estate holdings, fine art, film revenue streams, and even collectible luxury goods can be securitized into blockchain-native tokens.

Imagine holding a token linked to a music album that grants early concert access. Or a token tied to a luxury handbag line that provides priority purchasing rights. Once investors experience programmable ownership—where financial exposure and experiential rights merge—the traditional paper-based market may feel obsolete.

Recent global developments support this trajectory. Major financial institutions such as BlackRock and JPMorgan are piloting tokenized funds and on-chain settlement networks. Real estate tokenization platforms in the U.S., Singapore, and the UAE are already enabling fractional participation in properties valued at tens of millions of dollars.

The economic implication is profound: liquidity premiums may compress, minimum investment thresholds may fall, and global capital may access opportunities previously restricted to institutional insiders.

3. Stablecoins: The Final Settlement Layer

Stablecoins were described as the “final piece” of digital financial infrastructure. While cryptocurrencies such as Bitcoin provide store-of-value characteristics, stablecoins provide transactional efficiency.

Dollar-pegged stablecoins already process trillions of dollars annually, rivaling traditional remittance corridors. Their utility lies in instant cross-border settlement, reduced intermediary friction, and programmable escrow logic.

By 2028 and beyond, tokenized securities and stablecoins may operate together seamlessly:

- Tokenized bonds settle instantly in stablecoins.

- Cross-border equity trades clear in minutes rather than days.

- Treasury operations shift toward on-chain liquidity pools.

Regulatory clarity remains crucial. The U.S., EU (MiCA framework), and parts of Asia are progressively defining reserve requirements and compliance standards. Once regulatory certainty solidifies, stablecoins may underpin wholesale banking operations rather than merely retail crypto exchanges.

4. Privacy and the Next Technical Frontier

Simplex’s Web3 leadership highlighted a critical tension: blockchain transparency versus financial privacy.

Public blockchains are verifiable by design, yet financial systems require selective disclosure. The future likely depends on zero-knowledge proofs, privacy-preserving computation, and permissioned verification layers that allow compliance without sacrificing confidentiality.

If blockchain systems evolve to reveal information only to authorized participants—regulators, counterparties, or auditors—they may become superior to legacy banking infrastructure in both resilience and compliance.

5. AI, Regime Changes, and Human Finance

AI-driven asset management is advancing rapidly. Algorithmic agents can rebalance portfolios, monitor volatility, and optimize yield strategies across decentralized and centralized platforms.

Under normal market conditions, AI may consistently outperform discretionary decision-making. However, during regime shifts—sharp liquidity crises, geopolitical shocks, systemic collapses—human psychology becomes central.

Executives emphasized that financial advisors will remain indispensable. When markets drop 30% in weeks, reassurance and behavioral discipline cannot be outsourced entirely to algorithms.

The likely future is hybrid:

- AI handles execution and optimization.

- Humans define strategic risk tolerance.

- Governance frameworks set decision boundaries for automated agents.

This division preserves accountability while leveraging computational precision.

6. Japan’s Household Assets and the 2045 Vision

Japan holds approximately $15 trillion in household financial assets, with nearly half allocated to cash and deposits. A gradual shift toward diversified investment vehicles could unlock enormous capital flows.

If tokenization lowers entry barriers and stablecoins streamline settlement, households may not need to be persuaded to invest. The infrastructure itself will make participation intuitive.

By 2045, digital finance may not be visible as a distinct sector. Instead, it will operate as background infrastructure—like electricity or the internet—powering capital allocation toward entrepreneurs, artists, developers, and innovators.

One executive described a future where aspiring filmmakers or creators can tokenize revenue streams directly, attracting global micro-investments. Finance becomes not merely efficient—but enabling.

Conclusion: From Speculation to Infrastructure

The conversation at DSC2026 revealed a consistent trajectory:

- Crypto has matured into a macro-relevant asset class.

- Tokenization is poised to redefine ownership and liquidity.

- Stablecoins may underpin global settlement.

- AI will optimize, but humans will contextualize.

- Digital finance will expand opportunity rather than merely digitize legacy systems.

For investors seeking new crypto assets, emerging revenue models, or practical blockchain applications, the shift is already underway. The next decade may not be about price volatility alone—but about structural transformation.

By 2045, we may look back at today’s crypto markets not as speculative frontiers, but as the early scaffolding of a fully tokenized financial ecosystem.