Main Points :

- The European Central Bank (ECB) plans to begin selecting Payment Service Providers (PSPs) in Q1 2026 for a digital euro pilot.

- A 12-month pilot is targeted for the second half of 2027, ahead of a potential 2029 launch.

- The digital euro is designed to reinforce European payment sovereignty and reduce reliance on international card networks.

- EU-licensed PSPs will gain early-mover advantages in onboarding, liquidity management, and compliance preparation.

- The initiative aims to balance competition between domestic schemes and global players such as Visa and Mastercard.

- The move occurs amid global acceleration of CBDC and stablecoin initiatives, including projects by the Federal Reserve and the People’s Bank of China.

- For crypto investors and blockchain operators, the digital euro represents both competitive pressure and infrastructure opportunity.

1. Europe’s Digital Euro Enters a Decisive Phase

The European Central Bank has taken a concrete step toward operationalizing the digital euro, announcing that it will begin selecting Payment Service Providers (PSPs) in the first quarter of 2026. According to ECB Executive Board member Piero Cipollone, the 12-month pilot is expected to begin in the second half of 2027, assuming the legal framework is finalized in 2026.

This timeline aligns with the ECB’s broader roadmap, which foresees a potential full-scale launch around 2029. The digital euro would function as a central bank digital currency (CBDC), complementing physical cash and existing electronic payment methods across the eurozone.

Unlike decentralized cryptocurrencies such as Bitcoin or Ethereum, the digital euro would be issued and backed directly by the Eurosystem — the ECB and national central banks. However, its distribution and customer interface would largely be handled by private-sector PSPs.

From a strategic perspective, this marks a transition from conceptual exploration to operational preparation. The selection of PSPs is not merely administrative; it is foundational to shaping how the digital euro integrates into Europe’s banking and payments ecosystem.

2. Why 2027 Matters: A Strategic Timeline

The planned 2027 pilot reflects both urgency and caution. On one hand, Europe faces mounting competitive pressure from:

- U.S. dollar-denominated stablecoins (e.g., USDC, USDT),

- Large tech payment ecosystems,

- China’s digital yuan expansion,

- Private payment innovations in emerging markets.

On the other hand, the ECB must carefully balance financial stability, privacy, banking sector health, and technological reliability.

The legal prerequisite is crucial. The European Union must complete legislation defining the digital euro’s mandate, limits, and operational framework. If the law is passed in 2026 as anticipated, the pilot can proceed in 2027.

This staged approach demonstrates Europe’s institutional style: slower than private crypto innovation, but structurally durable once implemented.

3. PSP Selection: Early Advantage for Licensed Operators

Only EU-licensed Payment Service Providers will play a central role in distributing the digital euro. For participating PSPs, the pilot offers multiple strategic advantages:

- Customer onboarding experience in CBDC environments.

- Liquidity management practices between commercial bank reserves and digital euro holdings.

- Compliance alignment with future reporting standards.

- Infrastructure readiness forecasting for staffing and system upgrades.

The pilot will involve a limited number of payment firms, merchants, and Eurosystem staff. This controlled environment allows operational testing without systemic risk.

For fintech firms and regulated crypto exchanges, this phase represents a first-mover opportunity. Operators who gain direct exposure to CBDC workflows could shape technical standards and influence the final system design.

For institutions building EMI/VASP infrastructure — particularly those already operating under central bank supervision — this resembles a regulatory sandbox at continental scale.

4. Protecting Europe’s Payment Sovereignty

A central objective of the digital euro is strategic autonomy.

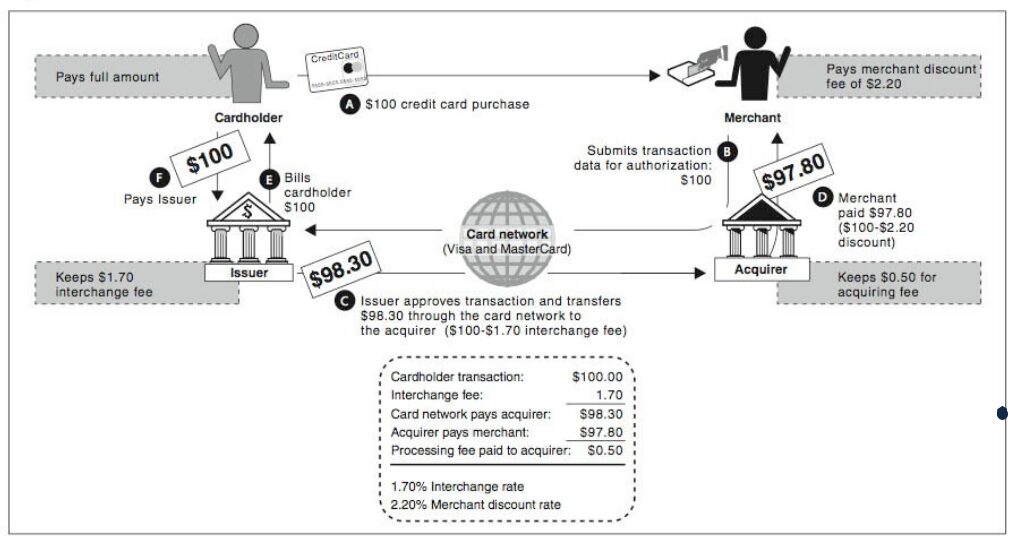

Europe currently relies heavily on international card networks, especially Visa and Mastercard. Domestic systems such as Italy’s Bancomat and Spain’s Bizum exist, but cross-border card dominance remains strong.

Cipollone explicitly noted that the threat to banks’ role in payments does not stem only from stablecoins but also from private payment platforms. In this sense, the digital euro is not anti-crypto per se — it is anti-dependency.

The ECB intends to structure merchant fees within the digital euro network so that:

- They are lower than the highest-cost international networks,

- But higher than the cheapest domestic schemes.

This calibrated pricing model aims to maintain competitive balance without destabilizing domestic systems.

[Payment Fee Comparison Model]

Explanation:

This diagram should illustrate a tiered fee structure:

- International Networks: approx. $2.00 per $100 transaction (example illustration)

- Digital Euro: approx. $1.20 per $100 transaction

- Domestic Schemes: approx. $0.80 per $100 transaction

(All figures converted to dollar equivalents for standardization.)

5. The Global Context: CBDCs and Stablecoin Competition

The digital euro cannot be evaluated in isolation.

Globally:

- The People’s Bank of China has already piloted the e-CNY.

- The Federal Reserve continues to research digital dollar frameworks.

- Emerging economies are testing retail CBDCs at scale.

- Private stablecoins dominate cross-border crypto settlement.

Stablecoins have become essential liquidity rails in crypto markets, particularly in decentralized finance (DeFi), derivatives settlement, and OTC trading.

For European policymakers, dollar-backed stablecoins represent both monetary influence and systemic risk. If eurozone users increasingly transact in $-denominated stablecoins, monetary sovereignty weakens.

Thus, the digital euro can be interpreted as a defensive and strategic instrument — not merely technological modernization.

6. Implications for Crypto Investors and Builders

For readers seeking new crypto assets and revenue streams, several implications emerge:

A. Infrastructure Plays

Companies providing:

- CBDC-compatible wallets,

- Identity verification layers,

- Regulatory reporting tools,

- Liquidity bridge solutions between CBDCs and stablecoins,

may see increased demand.

B. Competitive Pressure on Stablecoins

If the digital euro achieves broad retail adoption, euro-denominated stablecoins could face reduced utility in domestic transactions. However, in DeFi and cross-border crypto markets, decentralized liquidity will likely persist.

C. Banking System Reinforcement

Unlike decentralized cryptocurrencies, the digital euro reinforces the role of regulated banks. Therefore, hybrid models — where regulated custodians bridge traditional banking and crypto liquidity — may become dominant.

D. Arbitrage and FX Dynamics

If CBDC-based settlement reduces euro transaction costs, cross-border settlement efficiency improves. FX spreads, currently influenced by correspondent banking chains, may compress.

For fintech operators managing treasury across $ and € exposures, this matters materially.

7. Operational Considerations for Fintech and VASP Institutions

For regulated EMI/VASP institutions, the digital euro introduces operational questions:

- How will CBDC balances be segregated?

- Will wallet caps apply (e.g., $3,000 equivalent holding limits)?

- How will AML monitoring integrate with CBDC flows?

- Will in-app transfers count toward monthly AML thresholds?

Institutions already building compliance matrices, liquidity dashboards, and reporting frameworks should consider CBDC compatibility early.

The digital euro may not replace crypto rails — but it will coexist. Institutions prepared for interoperability will benefit.

8. Risks and Structural Challenges

Despite strategic ambition, risks remain:

- Privacy concerns among citizens.

- Banking disintermediation if deposit shifts occur.

- Cybersecurity attack vectors.

- Cross-border usability constraints.

- Political delays in EU legislation.

Moreover, adoption depends on user convenience. If the digital euro offers no clear UX improvement over existing apps, inertia may dominate.

9. Long-Term Outlook Toward 2029

The 2027 pilot is a stress test for Europe’s monetary digitization.

If successful, by 2029 the eurozone could operate a fully integrated public digital currency layer — interoperable with banks, merchants, and fintechs.

This would reshape payment architecture across a $15+ trillion economy (eurozone GDP converted to dollar terms).

For blockchain practitioners, the lesson is clear: CBDCs are not a replacement for crypto — they are parallel rails that will redefine regulatory, liquidity, and settlement landscapes.

Conclusion

The ECB’s decision to begin PSP selection in Q1 2026 marks a turning point. The digital euro is no longer a theoretical discussion — it is entering operational structuring.

For Europe, it is a sovereignty play.

For banks, it is a defensive reinforcement.

For fintechs, it is an early-mover opportunity.

For crypto investors, it is both competitive pressure and infrastructure expansion.

The 2027 pilot will determine whether Europe can modernize its payment system without surrendering autonomy to either global card networks or dollar-based stablecoins.

The outcome will not merely influence European payments — it may define the next phase of global digital currency architecture.