Key Points :

- 72% of global financial leaders believe digital asset adoption is essential for competitiveness

- Stablecoins are emerging as the dominant use case, with 74% citing improved cash flow efficiency

- Institutions are shifting from “whether” to adopt digital assets to “how” to implement them

- Tokenization and custody infrastructure are becoming top strategic priorities

- Fintech firms lead innovation, while traditional firms prefer partnerships

- Security, compliance, and trusted infrastructure providers are critical decision factors

1. A Structural Shift: From Debate to Execution

The global financial industry has reached a turning point. According to a recent survey conducted by Ripple, involving over 1,000 financial leaders worldwide, 72% of respondents now believe that offering digital asset solutions is no longer optional—it is essential for maintaining competitiveness in the evolving financial landscape.

This finding marks a profound shift in mindset. For years, digital assets were treated as speculative instruments or fringe innovations. However, the survey reveals that the conversation has fundamentally changed. Financial institutions are no longer asking whether they should engage with digital assets; instead, they are focused on execution—how to build, integrate, and scale the necessary infrastructure.

This transition reflects broader macro trends. Regulatory clarity is gradually improving in key jurisdictions, major banks are increasing their exposure to blockchain technologies, and fintech adoption continues to accelerate globally. Together, these forces are creating a structural push toward digital asset integration.

From a strategic perspective, this shift mirrors earlier technological transitions in finance, such as the adoption of online banking and mobile payments. Institutions that failed to adapt in those eras lost market share. Today, digital assets represent a similar inflection point.

2. Stablecoins: The Core Use Case Driving Adoption

“Stablecoin Utility in Financial Operations”

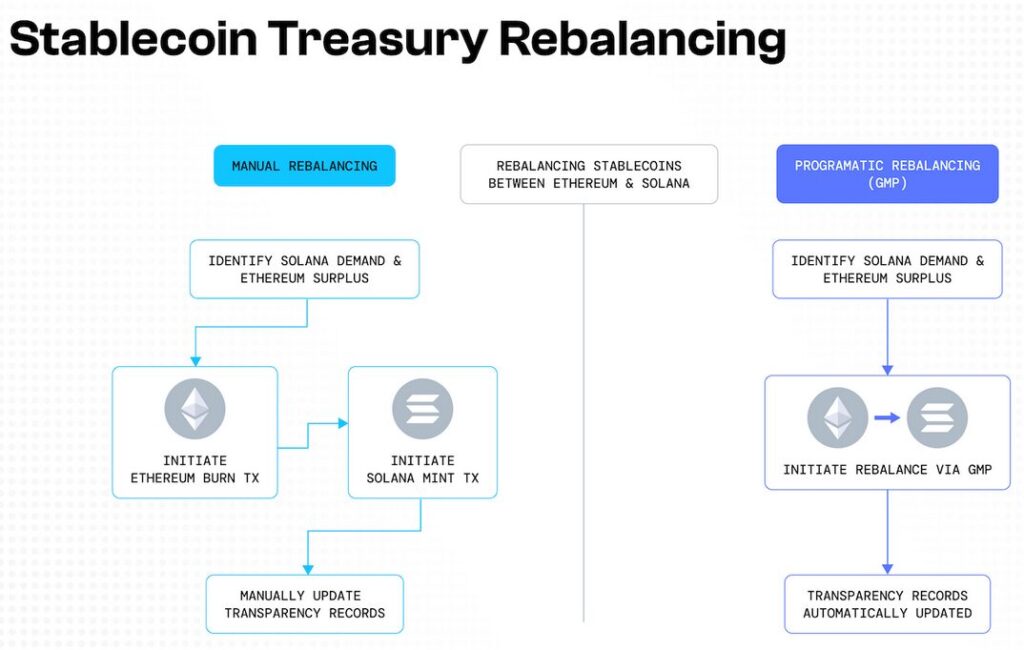

Among all digital asset use cases, stablecoins have emerged as the clear leader. According to the survey, 74% of respondents believe that stablecoins can enhance cash flow and unlock idle capital.

This is not merely a theoretical benefit. Stablecoins address several long-standing inefficiencies in traditional finance:

- Settlement Speed: Transactions settle in near real-time, compared to the multi-day delays of legacy systems

- Capital Efficiency: Reduced need for pre-funded accounts and nostro/vostro balances

- Global Accessibility: Seamless cross-border transactions without reliance on correspondent banking networks

For treasury operations, this represents a paradigm shift. Corporations and financial institutions can manage liquidity dynamically, reducing trapped capital and improving operational efficiency.

Institutional perception of stablecoins is also evolving. Rather than viewing them solely as payment instruments, many now see them as programmable liquidity tools. This opens new possibilities, such as automated settlements, conditional payments, and integrated financial workflows.

Recent industry developments reinforce this trend. Major financial institutions are actively exploring or launching their own stablecoin initiatives, while regulators are increasingly focusing on frameworks to govern their issuance and use. In markets like the United States, Europe, and parts of Asia, stablecoins are becoming central to discussions on the future of money.

3. Tokenization and Custody: Building the Next Financial Layer

“Tokenization Lifecycle and Custody Architecture”

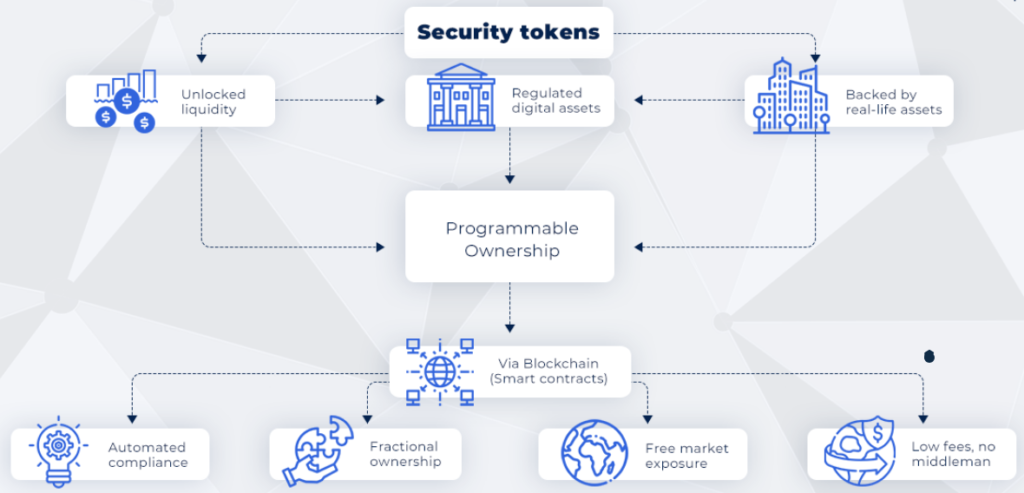

Beyond payments, tokenization is rapidly gaining traction as a transformative force in financial markets. The survey highlights strong institutional interest in tokenizing real-world assets (RWAs), including securities, real estate, and funds.

However, with this opportunity comes complexity. Institutions are prioritizing several key components:

- Custody Solutions: 89% of respondents identified secure storage as a top priority

- Lifecycle Management: 82% emphasized the importance of managing tokens throughout their lifecycle

- Primary Distribution: 80% highlighted the need for efficient issuance mechanisms

Custody, in particular, is emerging as a foundational pillar. Unlike traditional assets, digital assets require specialized infrastructure for secure storage, including multi-signature wallets, hardware security modules, and institutional-grade cold storage solutions.

Banks and asset managers are especially focused on custody capabilities. This reflects both regulatory requirements and the need to safeguard client assets. At the same time, there is growing demand for advisory services, particularly in structuring tokenized offerings before issuance. Notably, 85% of bank respondents emphasized the importance of pre-issuance structuring, compared to 76% of asset managers.

This indicates that institutions are not only adopting new technologies but also seeking experienced partners to guide implementation.

4. Build, Buy, or Partner: Strategic Infrastructure Decisions

One of the most important insights from the survey is the shift toward infrastructure strategy. Financial institutions are now actively deciding whether to:

- Build proprietary digital asset solutions

- Purchase existing platforms

- Partner with specialized providers

Fintech companies are leading in internal development, with 47% planning to build their own solutions. In contrast, only 14% of non-financial corporations intend to do the same. Instead, 74% of these companies prefer to collaborate with external providers.

This divergence reflects differences in core competencies. Fintech firms often have the technical expertise to develop in-house solutions, while traditional enterprises prioritize speed, cost efficiency, and risk mitigation through partnerships.

From a strategic standpoint, partnerships are becoming a dominant model. Institutions are increasingly working with blockchain infrastructure providers, custody specialists, and compliance-focused platforms to accelerate deployment.

This trend aligns with broader developments in the blockchain ecosystem, where modular infrastructure and API-driven services enable rapid integration without the need for full-stack development.

5. Security, Compliance, and Trust: The Non-Negotiables

“Digital Asset Infrastructure Trust Stack”

As institutions move toward implementation, security and compliance have become critical decision factors. The survey reveals that 97% of respondents consider certifications such as ISO standards and SOC 2 compliance essential when selecting infrastructure providers.

This reflects the high-stakes nature of digital asset operations. Unlike traditional systems, blockchain transactions are irreversible, and security breaches can result in immediate and significant losses.

Key considerations include:

- Regulatory Compliance: Adherence to local and international regulations

- Operational Security: Protection against cyber threats and internal risks

- Auditability: Transparent and verifiable transaction records

- Scalability: Infrastructure capable of handling institutional volumes

For regulated entities such as banks and VASPs, these factors are not optional—they are mandatory. This is particularly relevant in jurisdictions like the Philippines, where regulatory frameworks are evolving rapidly, and compliance expectations are increasing.

6. Market Implications: The Race to Digital Asset Integration

The implications of this survey extend far beyond individual institutions. They signal a broader transformation of the financial system.

Digital assets are no longer a niche market. They are becoming a core component of financial infrastructure. Institutions that fail to adapt risk being left behind, while those that successfully integrate digital asset solutions stand to gain significant competitive advantages.

This transition is also reshaping revenue models. New opportunities are emerging in areas such as:

- Custody services

- Token issuance platforms

- Cross-border payment solutions

- Digital asset lending and liquidity provision

For readers seeking new crypto assets or income opportunities, this institutional shift is particularly important. As financial giants enter the space, they bring liquidity, credibility, and infrastructure—factors that can drive long-term market growth.

Conclusion: From Optional Innovation to Strategic Imperative

The findings from Ripple’s survey make one thing clear: digital assets have crossed the threshold from experimentation to necessity.

Financial institutions are no longer debating their relevance. Instead, they are actively building the infrastructure required to support them. Stablecoins, tokenization, and custody are at the forefront of this transformation, supported by a growing ecosystem of technology providers and regulatory frameworks.

For businesses, investors, and developers, the message is unequivocal. The future of finance is being built on digital asset infrastructure, and the time to engage is now.