Key Points :

- U.S. lawmakers released a bipartisan Digital Asset PARITY Act discussion draft to modernize crypto tax treatment.

- The draft includes stablecoin capital gain exemptions and $200 de minimis tax exemptions for small transactions.

- Passive staking and mining rewards may be deferred for up to five tax years and taxed as long‑term capital gains.

- Wash sale rules are proposed to prevent artificial loss harvesting.

- The draft excludes Bitcoin from stablecoin exemptions, generating controversy.

- The proposal remains a discussion draft and has not yet been formally introduced as legislation.

Introduction: A Turning Point for U.S. Crypto Tax Policy

The United States is on the verge of a significant shift in how cryptocurrencies are taxed. On March 26, 2026, Representatives Max Miller (Republican) and Steven Horsford (Democrat) released a bipartisan discussion draft of the Digital Asset Protection, Accountability, Regulation, Innovation, Taxation, and Yields Act—widely referred to as the Digital Asset PARITY Act. This draft aims to modernize the federal tax code’s treatment of digital assets and resolve longstanding confusion over how everyday users, investors, and institutions should account for gains, losses, and crypto‑derived income.

In the current U.S. tax framework, even tiny cryptocurrency transactions can trigger taxable events, causing a recordkeeping and compliance burden for ordinary users. Critics have long called for simplification and de minimis exemptions to allow crypto to function more like traditional payment methods. The PARITY Act discussion draft attempts to address this by providing specific rules for stablecoins, staking rewards, and wash sales—while leaving some contentious issues, such as the tax treatment of Bitcoin payments, unresolved.

Stablecoins: De Minimis Exemption and Zero Gain Recognition

One of the most ground‑breaking provisions in the PARITY Act draft is the treatment of stablecoins—cryptocurrencies pegged to a fiat currency like the U.S. dollar. Under the draft proposal:

- If a regulated stablecoin’s trading price remains within ±1% of $1.00, gains and losses on disposals of that asset would not be recognized for tax purposes.

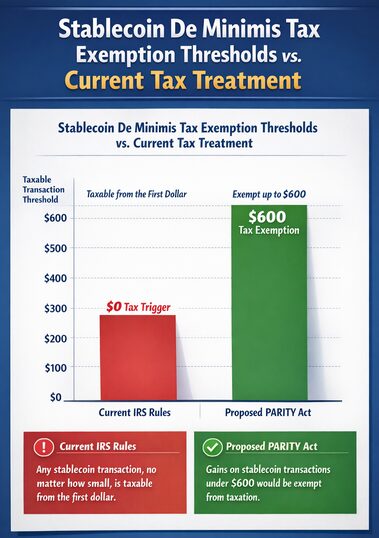

- Moreover, stablecoin transactions under $200 would qualify for a de minimis exemption, meaning neither tax nor reporting requirements would apply to such small transactions.

This approach aims to mirror the way foreign currency transactions are treated under U.S. tax law and substantially reduce the compliance burden for everyday crypto users making low‑value payments. For merchants and consumers alike, this could transform the utility of stablecoins in retail and digital commerce by eliminating tax friction for routine transfers.

“Stablecoin De Minimis Tax Exemption Thresholds vs. Current Tax Treatment”

(Bar chart comparing tax triggers under current IRS rules vs. proposed PARITY Act exemptions)

Stablecoins have become a core infrastructure in digital finance, used for payments, remittances, and yield products around the world. Their integration into the U.S. tax code represents one of the most pragmatic steps toward broader crypto adoption.

Passive Staking and Mining Rewards: Deferred Taxation

Another major element of the PARITY Act draft is the tax treatment of staking rewards and other passive crypto income. According to the proposal:

- Taxpayers may choose to defer taxation on passive staking rewards received from verifying blockchain transactions for up to five tax years.

- After the deferral period, the eventual sale of the staking rewards would be taxed as long‑term capital gains rather than ordinary income.

This provision directly responds to the controversial 2024 IRS guidance that treated staking and mining rewards as ordinary income upon receipt—a policy that many in the industry called “taxation of unrealized gains.” The PARITY draft’s deferral option is a compromise between immediate taxation and the complete deferral until asset disposition.

Wash Sale Rules and Broader Crypto Tax Modernization

The PARITY Act draft also proposes extending wash sale rules—currently applied to the stock market—to digital assets. Wash sale rules prevent investors from claiming tax losses if they quickly repurchase substantially the same asset after selling at a loss. This aims to close a longstanding loophole around opportunistic tax loss harvesting in crypto markets.

Moreover, the draft includes provisions to align crypto lending and collateralized loan tax treatment with existing securities and commodities tax rules, offering more legal certainty for institutional market participants.

Bitcoin Exclusion: A Source of Controversy

While the stablecoin exemptions and staking changes have been welcomed by many in the industry, one major criticism is the exclusion of Bitcoin from tax relief provisions. The stablecoin exemptions in the PARITY draft apply only to coins pegged to the dollar within a narrow price band, effectively leaving Bitcoin and other non‑stable assets subject to current tax rules.

Policy groups such as the Bitcoin Policy Institute have publicly urged lawmakers to broaden the de minimis exemption to include Bitcoin and other major cryptocurrencies, arguing that fair treatment should not be limited to stable assets.

Legislative Status and Industry Reactions

It is important to note that the PARITY Act is currently a discussion draft, not formal legislation introduced to Congress. Its release is meant to spark debate among lawmakers, industry stakeholders, and tax experts before any official bill is introduced.

The crypto industry has largely welcomed attempts to modernize tax rules, with groups like the Digital Chamber describing the draft as essential for U.S. innovation. However, some advocates argue that the exclusion of Bitcoin and certain yield‑generating products may hinder broader adoption.

The PARITY Act is being considered in parallel with other regulatory efforts such as the Digital Asset Market Clarity Act (CLARITY Act), which seeks to clarify regulatory oversight and enforceability across different digital asset classes.

Conclusion: What This Means for Crypto Users and Investors

The Digital Asset PARITY Act discussion draft represents a significant step forward for U.S. crypto tax policy, offering much‑needed clarity and practical reforms. If enacted, the stablecoin exemptions and staking tax deferral could lower barriers to everyday crypto use and investment, potentially accelerating adoption and innovation. However, the draft’s limitations—particularly its exclusion of Bitcoin from key benefits—highlight the unresolved challenges in balancing tax fairness, innovation incentives, and regulatory oversight.

For investors, developers, and blockchain practitioners, the evolving tax landscape in the U.S. underscores the importance of tracking legislative developments and planning tax strategies accordingly. The PARITY Act is not just a tax bill; it is part of a broader narrative about the future of digital assets in mainstream finance.