Main Points:

- Recovery to Pandemic-Era Highs: Q2 2025 saw $10.03 billion in venture investment—the strongest quarter since Q1 2022.

- Record-Breaking June: The industry pulled in $5.14 billion in June alone, its best month since January 2022.

- Top Rounds Led by Strive Funds and TwentyOneCapital: Strive’s $750 million and TwentyOneCapital’s $585 million anchored the quarter.

- Coinbase Ventures Dominates Deal Count: The arm of the major U.S. exchange led with 25 deals, followed by a16z, Pantera, and Paradigm.

- Sector Focus: Blockchain infrastructure and DeFi projects drew the most funding, while CeFi, NFT, and GameFi also maintained interest; meme coins lagged.

- Early-Stage Rounds Continue Strong: Seed rounds accounted for 19.43 % of deals over the past year, with strategy rounds (14.23 %) and M&A (9.44 %) also notable.

1. A Powerful Q2 Rebound

In the three months spanning April through June 2025, the crypto sector attracted $10.03 billion in venture capital—the highest quarterly total since the $16.64 billion recorded in Q1 2022. This resurgence follows a prolonged period of subdued fundraising, reflecting a renewed sense of confidence among institutional and high-net-worth investors.

Analysts point to stabilizing macroeconomic indicators and clearer regulatory cues as key drivers for this rebound. For instance, decreasing U.S. inflation and the gradual maturation of spot Bitcoin ETFs have lessened the uncertainty that hampered capital deployment in 2023 and early 2024.

2. June’s Record-Breaking Surge

June 2025 stands out as a milestone, raising $5.14 billion—the largest single-month total since January 2022. Investors lined up behind high-profile rounds and emergent protocols aiming to bridge Web2 and Web3.

This late-quarter momentum suggests that capital dry-ups in Q1 and early Q2 may have been temporary pauses rather than a fundamental loss of faith in blockchain innovation.

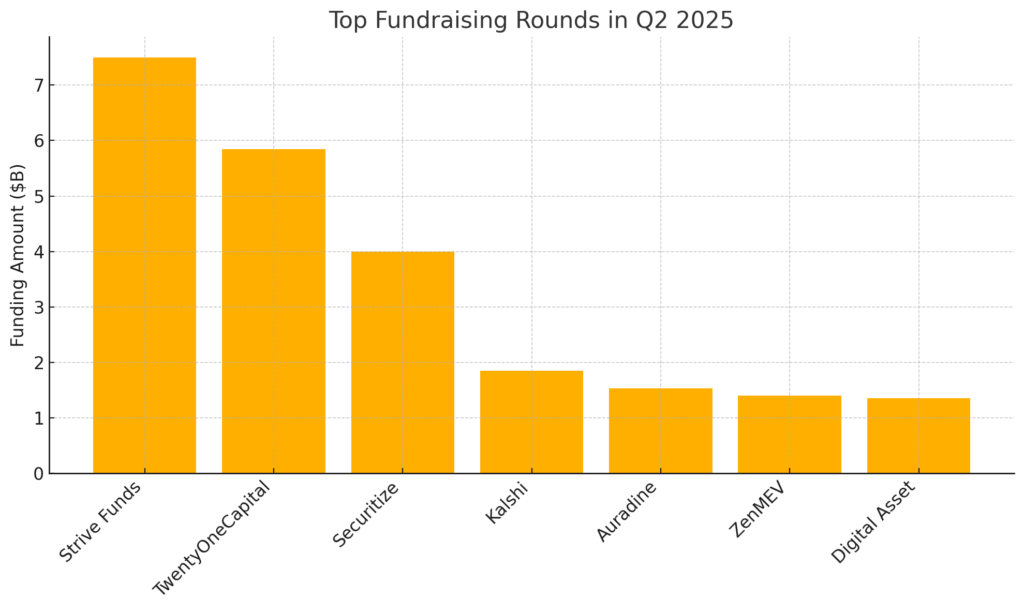

3. Leading the Pack: Top Fundraising Rounds

The quarter’s biggest headline-grabbing fundraises included:

- Strive Funds ($750 million in May, focusing on BTC alpha-generating strategies)

- TwentyOneCapital ($585 million in April, targeting diversified crypto assets)

- Securitize ($400 million in a tokenization-focused round)

- Kalshi ($185 million for derivatives on real-world events)

- Auradine ($153 million in DeFi lending)

- ZenMEV ($140 million in MEV-resistant infrastructure)

- Digital Asset ($135 million for DLT integration tools)

Figure 1 below visualizes these top rounds:

<div align=”center”> *Figure 1: Top Fundraising Rounds in Q2 2025* </div>

4. Deal-Makers: Most Active Investors

When it comes to deal count rather than dollars, Coinbase Ventures led all investors with 25 deals in Q2, underlining the strategic importance of in-house venture arms for major exchanges. They were followed by:

- a16z (Andreessen Horowitz)

- Pantera Capital

- Galaxy Digital

- Paradigm (4 flagship rounds)

This underscores a bifurcation in strategy: some firms chase fewer, larger “blockbuster” rounds, while others – led by exchange-affiliated VCs – spread capital across a wider range of early-stage projects.

5. Sectoral Breakdown: Where the Money Went

Infrastructure & DeFi remained dominant, accounting for the bulk of deployed capital. However, CeFi platforms, NFT marketplaces, and GameFi studios continued to attract meaningful investments. In contrast, meme-coin projects saw only sporadic spikes in financing, highlighting investors’ waning appetite for pure speculation.

6. Stage Analysis: Early vs. Growth Rounds

Over the past 12 months (ending Q2 2025), the distribution of 1,673 deals looked like this:

- Seed rounds: 19.43 %

- Strategy (growth) rounds: 14.23 %

- M&A: 9.44 %

- Pre-seed: 9.26 %

- Series A: 6.34 %

- Incubation: 3.35 %

The prominence of seed and strategy rounds suggests that investors are placing bets both on nascent teams and scaling protocols that have demonstrated product-market fit.

7. Notable Success: Galaxy Digital’s First External Fund

In June, Galaxy Digital closed its inaugural external venture fund at $175 million, surpassing its $150 million target. The fund aims to back stablecoins, tokenization platforms, and payment rails—areas poised for growth as blockchain interoperability advances.

Likewise, Theta Capital Management in Amsterdam raised >$175 million in May for a fund-of-funds dedicated to early-stage blockchain startups, underscoring Europe’s growing role in crypto venture capital.

8. Broader Market Context & Emerging Trends

Beyond VC, M&A activity hit all-time highs in May with Coinbase’s acquisition of Deribit contributing to a $2.9 billion tally. This suggests consolidation as a parallel avenue for growth and de-risking.

Security remains a concern: CertiK reported > $800 million lost to hacks and scams in Q2 2025, emphasizing the ongoing need for robust on-chain defenses.

Looking ahead to Q3, many analysts predict a continued recovery—bolstered by seasonal fundraising patterns and potential regulatory clarifications around token classifications.

Conclusion

Q2 2025 marks a pivotal moment: VC funding has rebounded to levels unseen since early 2022, driven by a combination of major growth rounds, record-setting monthly inflows, and active strategic participation by leading investors. As the sector pivots toward real-world asset tokenization, infrastructure scalability, and regulatory compliance, the prospects for the next wave of blockchain innovation appear brighter than they have in years.