Main Points :

- Crypto payments remain one of the most underdeveloped yet strategically important areas of the blockchain industry.

- Binance founder Changpeng Zhao (CZ) believes widespread adoption could happen within a few years—if integration with traditional finance accelerates.

- Regulatory clarity and banking partnerships are the missing links in the long-standing “chicken-and-egg” problem of crypto payments.

- Bitcoin’s role is evolving from pure payment tool to strategic reserve asset, while stablecoins and infrastructure layers may drive everyday usage.

- Crypto payments are likely to become invisible infrastructure, much like TCP/IP for the internet—used by everyone but understood by few.

1. Why Crypto Payments Still Matter in 2025

Despite more than a decade of development, crypto payments remain a paradox. The industry has produced trillion-dollar assets, global exchanges, decentralized finance (DeFi), and institutional-grade custody—but paying for coffee or daily services with crypto is still rare.

In a recent Q&A session, Binance founder Changpeng Zhao (CZ) directly addressed this contradiction. According to CZ, payments are not a “solved problem” but rather the final frontier that determines whether crypto becomes true financial infrastructure or remains primarily a speculative asset class.

He emphasized that while trading, investing, and token issuance have matured rapidly, payments are where crypto meets everyday life, and therefore where friction, regulation, and trust issues become most visible.

CZ’s central claim is bold: crypto payments could see meaningful global adoption within a few years, provided the right integration pathways emerge between blockchain systems and traditional finance.

2. The “Chicken and Egg” Problem of Crypto Payments

Bitcoin was originally introduced as a “peer-to-peer electronic cash system.” However, extreme price volatility, limited merchant acceptance, and regulatory uncertainty have prevented it from functioning as a daily medium of exchange.

CZ described this as a classic chicken-and-egg problem:

- Merchants hesitate to accept crypto because few customers want to pay with it.

- Users hesitate to pay with crypto because few merchants accept it.

This stalemate cannot be resolved by technology alone. According to CZ, regulation and banking integration are the missing catalysts.

Without clear legal treatment—especially regarding custody, taxation, and settlement—banks cannot fully integrate crypto payment rails. And without banks, crypto struggles to reach mass-market users who rely on cards, accounts, and familiar interfaces.

3. Regulation as an Enabler, Not an Obstacle

Contrary to the industry’s early libertarian ethos, CZ argues that regulation is not the enemy of adoption—ambiguity is.

Over the past few years, regulatory clarity has improved significantly in major jurisdictions. Frameworks for stablecoins, licensing of exchanges, and AML/KYC standards are gradually aligning with traditional finance norms.

This shift enables:

- Banks to offer crypto-linked accounts and cards

- Payment processors to settle in stablecoins

- Enterprises to hold digital assets on balance sheets

As regulation matures, crypto payments move from legal gray zones into compliant, scalable infrastructure.

4. Stablecoins: The Unsung Heroes of Payment Adoption

While Bitcoin remains the ideological foundation of crypto, stablecoins are emerging as the practical payment layer.

Dollar-pegged stablecoins—valued and settled in USD terms—eliminate volatility risk for both merchants and consumers. They enable instant settlement, cross-border payments, and 24/7 liquidity.

Global stablecoin circulation now exceeds hundreds of billions of dollars, and their usage in remittances, B2B settlements, and fintech apps continues to grow.

From CZ’s perspective, stablecoins may serve as the bridge technology that allows crypto payments to scale before volatility-tolerant assets like Bitcoin can be used directly.

5. Integration with Traditional Finance: The Real Breakthrough

The next phase of crypto payments is not about replacing banks—but interfacing with them.

CZ highlighted that real adoption will come when users can:

- Spend crypto via cards without knowing the underlying blockchain

- Receive salaries or payouts in crypto-backed accounts

- Move seamlessly between fiat and digital assets

This mirrors how internet users interact with TCP/IP without understanding packet routing. In the future, people may use crypto-powered payments without ever thinking about “Web3” or “blockchains.”

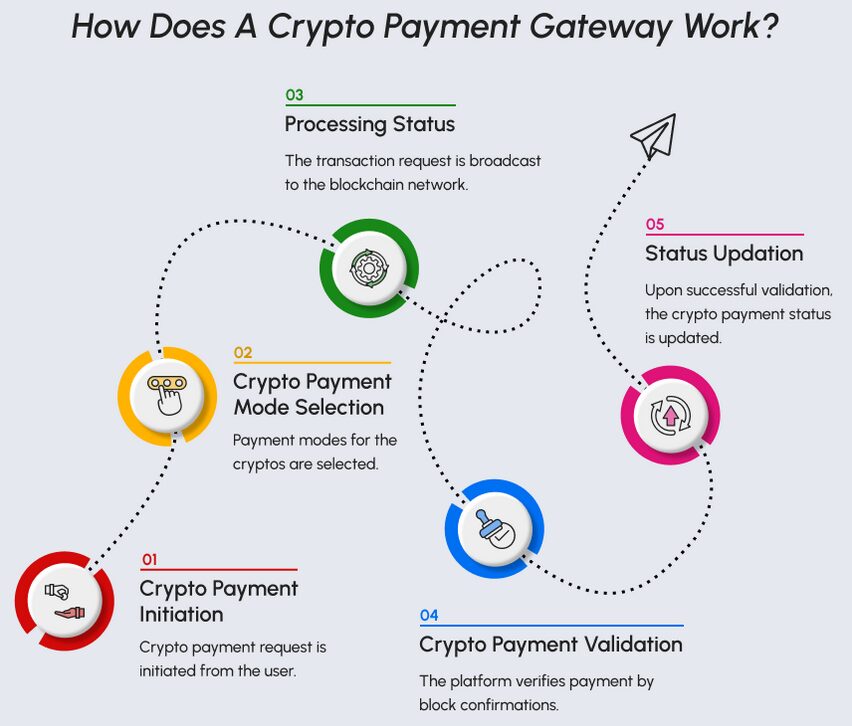

[Conceptual diagram showing integration between crypto wallets, stablecoins, banks, and merchants]

6. Learning from the Internet’s Adoption Curve

CZ drew a historical parallel: the internet took decades to become ubiquitous.

Early internet users needed technical expertise—dial-up connections, command lines, protocol knowledge. Over time, abstraction layers simplified everything. Today, users tap icons without knowing how data moves.

Crypto is on the same path. The industry is currently in its “infrastructure-heavy” phase, where complexity is unavoidable. But abstraction is accelerating.

Wallet UX, account abstraction, and embedded finance are reducing friction, making crypto usable without being visible.

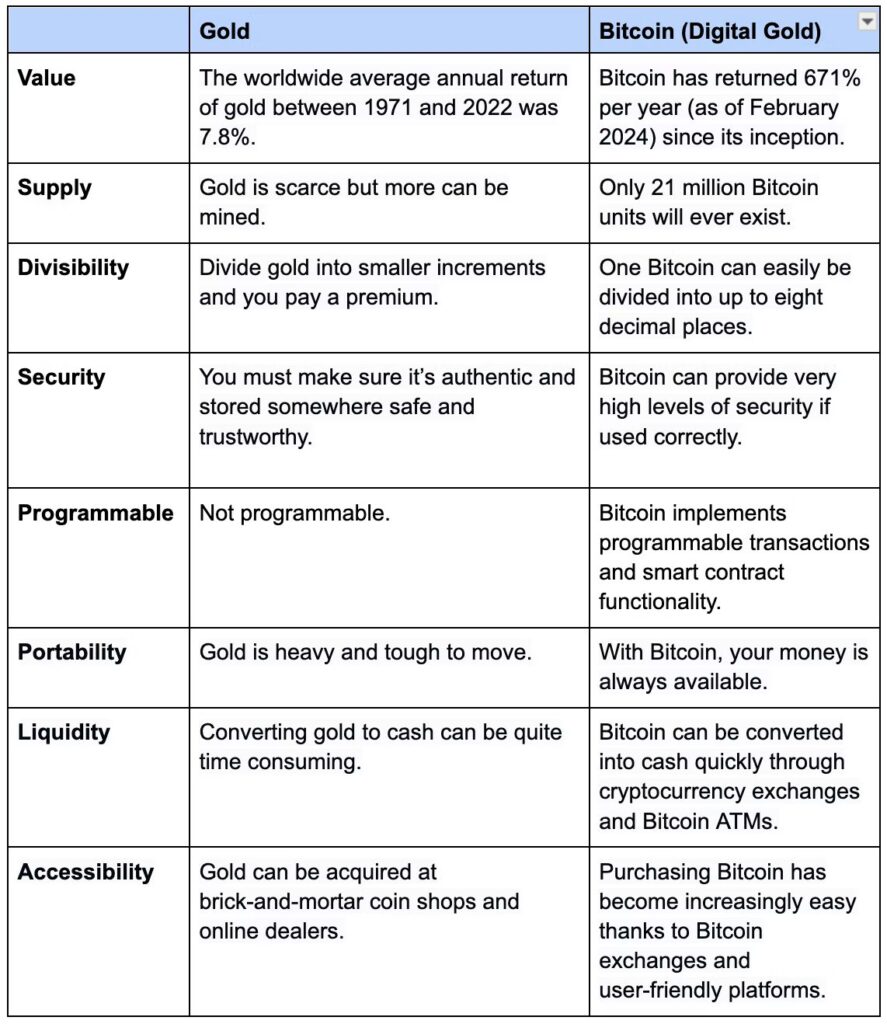

7. Bitcoin’s Role: From Payment Tool to Strategic Asset

While Bitcoin may not dominate day-to-day payments, CZ reaffirmed its importance as a strategic financial asset.

He referenced corporate treasury strategies—such as companies holding Bitcoin as a primary reserve asset—as both viable and sustainable. In an era of monetary expansion and geopolitical uncertainty, Bitcoin offers:

- Predictable supply

- Sovereign-neutral settlement

- Long-term store-of-value characteristics

Rather than competing with payment-focused assets, Bitcoin complements them—acting as digital gold within a broader crypto-financial ecosystem.

[Chart comparing Bitcoin’s role as reserve asset vs. stablecoins as payment instruments]

8. Implications for Investors and Builders

For investors seeking new crypto assets or revenue models, CZ’s outlook suggests several strategic themes:

- Payment Infrastructure Tokens

Projects enabling settlement, compliance, or interoperability may benefit disproportionately from payment adoption. - Stablecoin Ecosystems

Issuers, liquidity providers, and middleware supporting stablecoin flows stand to gain from increased transaction volumes. - Compliance-First Platforms

Regulation-ready solutions are more likely to integrate with banks and governments. - Invisible Crypto UX

Products that hide blockchain complexity will attract mainstream users faster than technically impressive but user-hostile systems.

9. The Road Ahead: From Speculation to Utility

Crypto’s first decade was dominated by speculation and experimentation. The next phase, according to CZ, is about utility, integration, and normalization.

Payments are not just another use case—they are the gateway to daily relevance. Once crypto payments become boring, predictable, and invisible, true mass adoption will have arrived.

Conclusion: A Few Years, Not Decades

CZ’s message is cautiously optimistic. Crypto payments will not replace cash or cards overnight, but the building blocks are now in place.

With regulatory clarity improving, stablecoins scaling, and banks entering the ecosystem, crypto payments may finally escape their experimental phase.

If successful, users in the near future may not ask, “Can I pay with crypto?”

They will simply pay—unaware that crypto is powering the transaction beneath the surface.