Key Takeaways :

- Renewed U.S.–China trade tensions triggered a sharp and rapid drop in Bitcoin (BTC), echoing earlier spring-2025 volatility.

- BTC fell from above $126,000 by more than 13 % in a matter of days, as leveraged positions were liquidated and liquidity fragmented across exchanges.

- The sell-off spread to altcoins and stablecoins, illustrating how crypto is deeply entwined with macroeconomic and geopolitical risk.

- On the flip side, retail investors bought into the dip (over $1.1 billion net), and more than 172 publicly listed companies hold Bitcoin as a hedge asset — pointing to underlying structural strength.

- Analysts suggest that if historical patterns hold, market risk‐off induced by geopolitics could persist until November before sentiment may gradually recover.

- For participants seeking new crypto opportunities or blockchain utility plays, understanding macro-geopolitical triggers is now as important as technicals or fundamentals.

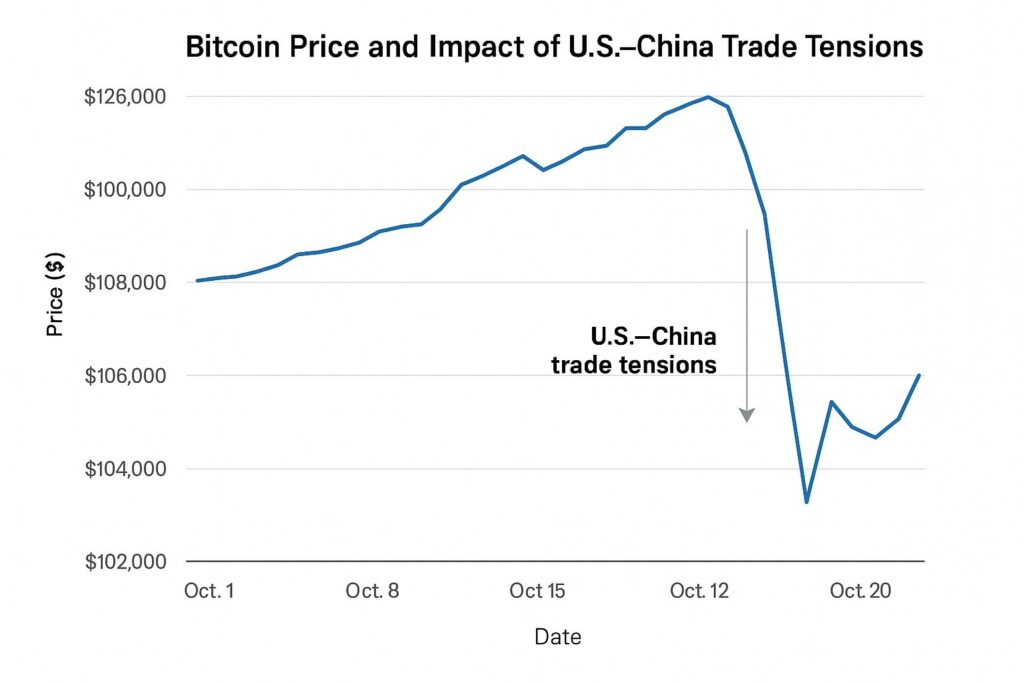

1. Triggering Event: Escalation of U.S.–China Trade War

In early October 2025, the crypto market was jolted by developments in the U.S.–China trade relationship. On October 10 the U.S. announced sweeping new measures: a 100 % tariff on Chinese imports and export controls on key software, in response to China’s restrictions on rare earth exports.

The market reaction was immediate. Bitcoin plunged from above approximately $121,000 to levels below $105,000 in some exchanges. Within the derivatives market, over $19 billion in leverage positions were liquidated. Altcoins fared worse, with some plunging by 40–70 % in a very short span.

This dynamic revived similarities with the March-to-May 2025 period when geopolitical risk had previously weighed on assets including crypto.

2. Mechanisms of the Crash: Leverage, Liquidity and Macro Risk

Why did this escalation hit cryptocurrencies so hard? Several mechanisms converged:

- Forced liquidations: High leverage in crypto derivatives meant that when BTC began to drop, margin calls triggered auto-deleveraging across major platforms.

- Liquidity fragmentation: The sharp drop and panic caused some exchanges to experience thinning liquidity, making price moves more extreme.

- Macro interlinkage: While crypto is often seen as uncorrelated, in high-stress macro moments it acts like a risk asset — falling in tandem with equities and other risk-on assets. The trade war undermined confidence across markets.

- Stablecoin/stress feedback: The collapse of a major U.S.-dollar-pegged stablecoin (USDE) and the resulting chain of liquidations highlighted how crypto is interwoven with broader financial plumbing.

3. Resilient Indicators: Why the Market Isn’t Totally Broken

Despite the turbulence, several indicators suggest that underlying structural demand remains in place:

- Retail investors stepped in: During the decline, individual investors were net buyers of over $1.1 billion worth of crypto.

- Institutional/Corporate holdings: More than 172 publicly listed companies hold Bitcoin as part of their treasury or strategic reserve — signalling that Bitcoin is still viewed as a macro hedge.

- Rebound potential: While volatility remains elevated, markets have shown the ability to recover quickly when sentiment shifts. For instance, after the crash, BTC bounced over 12 % back above $114,000.

4. Implications for Crypto Investors Looking for the Next Play

For readers hunting for new crypto assets or blockchain‐based revenue streams, this episode carries several lessons:

4.1 Risk management is paramount

- In times of macro stress, even large cap assets like BTC can drop double-digit percentages rapidly — so having hedges, stop-losses, or position sizing is critical.

- Recognize that systemic triggers (trade war, regulation shock) can nullify asset‐specific bullish narratives temporarily.

4.2 Geopolitics matters for crypto

- This episode underscores that crypto is not immune to macroeconomics or geopolitics. For example, trade war announcements, central-bank decisions, or sanctions can all ripple into crypto valuations.

- Tracking diplomatic calendar (e.g., U.S.–China meetings at APEC), tariff announcements, export control chatter can give early warning of elevated risk.

4.3 Look for utility & decentralised structural advantages

- In high-volatility regimes, projects with real‐world usage, protocol revenue, or tokenomics tied to utility (not pure speculation) may outperform meme coins or purely hype-driven tokens.

- Blockchain applications tied to trade finance, supply chain amid geopolitics, or on‐chain hedging demand may find structural tailwinds.

4.4 Altcoin opportunity amid fragmentation

- When large caps drop hard, altcoins often drop harder — but that also means the potential upside is greater if structural fundamentals hold.

- However the crash showed that low-liquidity altcoins are especially vulnerable to leveraged cascades and liquidity dry-ups.

5. Outlook: When Might Calm Return?

Historical precedent suggests that when macro or geopolitical shock hits crypto, risk sentiment typically takes about three months to begin materially improving. The article referenced indicates that in the 2025 spring episode, similar dynamics played out. Given the October shock, that places a potential stabilisation window around November.

Recent follow-ups support this: while the sharp drop happened, there are signs of diplomatic easing (e.g., announcement of a meeting between the U.S. president and China’s leader) which provided a temporary boost. That said, analysts caution the road ahead is still “choppy.”

Scenario to watch: if the U.S.–China meeting yields concrete movement (tariff de-escalation, export control relaxations), crypto may rally. If instead the conflict escalates (new sanctions, export bans), further downside remains.

Conclusion

The imminent drop in Bitcoin and the wider crypto market triggered by U.S.–China trade spill-over has re-emphasised a key lesson: digital assets do not exist in a vacuum. For those seeking new opportunities in crypto or blockchain utility, the interplay of macro forces, geopolitics and protocol fundamentals is now inseparable from asset selection.

While the sharp fall was painful, the fact that retail and institutional participation remain, and utility still matters, suggests this may be more of a recalibration than a structural breakdown. For smart players, now is a time to reassess risk exposure, watch geopolitical calendars, and lean into projects with strong real‐world usage and liquidity.

Stay mindful: volatility may remain elevated until at least November, but discipline, strategy and active observation can turn this period of turbulence into a foundation for future growth.