Main Points :

- 2025 was not a price-driven bull year, but a structural transformation year for crypto markets

- Regulatory clarity in the US and EU dramatically reduced systemic risk

- Institutional capital reshaped liquidity, stability, and market infrastructure

- ETFs, tokenization of real-world assets (RWA), and stablecoins matured simultaneously

- 2026 is expected to mark a shift from speculation to real demand and utilization

Introduction: Why 2025 Matters More Than It Looked

At first glance, 2025 appeared underwhelming for cryptocurrency investors. Major assets such as Bitcoin and Ethereum failed to deliver the explosive price appreciation many had expected following previous cycles. Market sentiment often oscillated between caution and disappointment.

Yet beneath the surface, something far more important was taking place.

According to an annual report released by Pantera Capital, one of the world’s largest and most influential crypto hedge funds, 2025 should be remembered not as a year of stagnation, but as a “Year of Structural Progress.” In Pantera’s analysis, the crypto industry quietly completed a fundamental transition—one that significantly lowered uncertainty, mitigated long-term risk, and laid the groundwork for sustainable growth.

This article expands on Pantera’s core thesis while incorporating recent developments from regulators, financial institutions, and market infrastructure providers. It is written for readers seeking new crypto assets, emerging revenue models, and practical blockchain use cases, rather than short-term speculation.

1. Pantera Capital’s View: 2025 as a Structural Turning Point

Pantera Capital’s 2025 report emphasizes a crucial distinction: price performance does not equal market maturity.

While token prices remained relatively range-bound, the underlying market architecture evolved rapidly. Regulatory ambiguity—long considered crypto’s greatest systemic risk—began to recede. Institutional-grade products and compliance frameworks became the norm rather than the exception.

Pantera argues that this shift fundamentally changed the crypto risk profile. Volatility driven by existential regulatory fears was gradually replaced by volatility linked to macroeconomic conditions and adoption cycles—similar to traditional asset classes.

Most importantly, Pantera concludes that these developments position the industry for a potential breakout growth phase in 2026, driven not by hype but by genuine economic demand.

2. Regulatory Clarity in the United States and Europe

2.1 The United States: From Enforcement to Frameworks

The United States played a central role in 2025’s transformation. A newly crypto-friendly administration initiated a comprehensive policy review of digital assets, establishing inter-agency working groups to address market structure, stablecoins, taxation, and custody.

The U.S. Securities and Exchange Commission launched a dedicated crypto task force and publicly clarified that many digital assets do not constitute securities. This represented a decisive shift away from regulation-by-enforcement.

Key developments included:

- Withdrawal of several high-profile lawsuits against crypto firms

- Official guidance confirming that certain stablecoins and staking services fall outside securities regulation

- Repeal of restrictive banking custody guidance (commonly known as SAB 121), enabling banks to offer crypto custody services

On the legislative front, Congress passed the GENIUS Act, establishing the first federal framework for payment-focused stablecoins. While broader market structure legislation (the CLARITY Act) remains under debate, the direction is clear: crypto is being integrated into the US financial system rather than excluded from it.

2.2 Europe: MiCA as a Global Benchmark

In parallel, the European Union continued implementing its comprehensive MiCA (Markets in Crypto-Assets) regulation. By 2025, MiCA had already begun serving as a global reference model, offering licensing clarity for exchanges, custodians, and stablecoin issuers across member states.

Pantera highlights that the simultaneous regulatory maturation in both the US and EU significantly reduced global jurisdictional risk—an essential prerequisite for institutional adoption.

3. Institutional Capital Redefines Market Stability

3.1 The ETF Revolution

One of the most visible signs of institutional integration in 2025 was the rapid expansion of crypto ETFs.

In the United States, spot ETFs for Bitcoin and Ethereum were joined by products tracking major altcoins such as Solana and XRP. These instruments provided regulated, liquid exposure to crypto assets without the operational complexity of self-custody.

Pantera reports that net inflows into US Bitcoin spot ETFs alone reached approximately $22 billion in 2025, fundamentally reshaping market liquidity.

[Annual Net Inflows into US Bitcoin ETFs (USD)]

3.2 Traditional Finance Embraces Crypto

Beyond ETFs, crypto-native firms continued integrating with traditional finance.

- Coinbase was included in the S&P 500, symbolizing crypto’s arrival in mainstream equity markets

- Robinhood expanded tokenized trading of equities, bonds, and real estate, accelerating the tokenization of real-world assets (RWA)

- Stablecoin supply expanded steadily, reinforcing crypto’s role in global payments and settlement

Pantera argues that these developments collectively transformed crypto from a speculative niche into a parallel financial infrastructure.

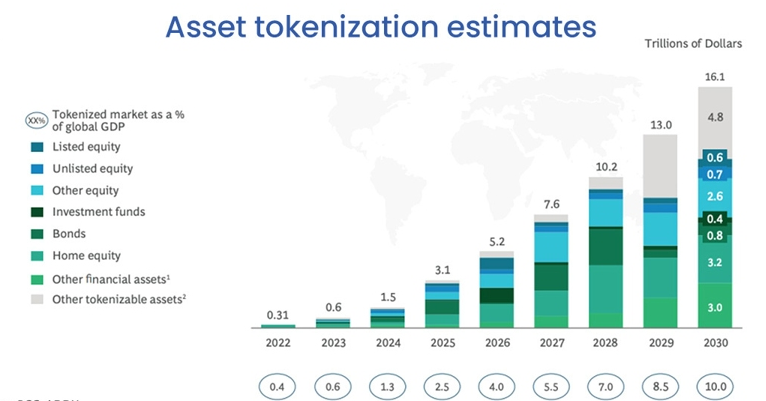

4. Real-World Assets and Practical Blockchain Use Cases

A defining feature of 2025 was the rapid growth of RWA tokenization.

Government bonds, real estate interests, money market funds, and private credit instruments increasingly migrated on-chain. For institutional investors, blockchain-based settlement reduced costs, improved transparency, and enabled near-instant liquidity.

This shift aligns closely with the industry-wide transition from “expectation-driven narratives” to “demand-driven economics.”

[Growth of Tokenized Real-World Assets (USD)]

5. 2026 Outlook: From Infrastructure to Expansion

5.1 Institutional Forecasts

Major financial institutions now view crypto as a permanent asset class rather than a speculative experiment.

JPMorgan has noted that despite temporary market contraction, regulatory easing and infrastructure maturity strengthen crypto’s role as an alternative investment alongside the US dollar and gold.

Meanwhile, BlackRock revealed early 2026 transfers of digital assets—including over 1,100 BTC and 7,200 ETH, valued at more than $123 million—to Coinbase custody, reinforcing expectations of continued institutional exposure.

5.2 ETF Market Expansion

Swiss asset manager 21Shares forecasts that total crypto ETF assets under management could exceed $400 billion by the end of 2026, driven by pension funds, sovereign wealth funds, and insurance companies.

Pantera’s leadership echoes this optimism, predicting that 2026 will mark the transition from regulatory uncertainty to full-scale execution.

Conclusion: 2026 as the First Mature Crypto Growth Cycle

The crypto market did not fail in 2025—it evolved.

By resolving regulatory ambiguity, welcoming institutional capital, and expanding real-world utility, the industry quietly completed a long-overdue structural transformation. As Pantera Capital’s analysis suggests, 2026 may become the first crypto growth cycle driven primarily by real demand rather than speculation.

For investors, builders, and institutions seeking sustainable opportunities, this shift represents not the end of crypto’s story—but its true beginning.